My Investments Update – July 2022

Here is my latest monthly update about my investments. You can read my June 2022 Investments Update here if you like

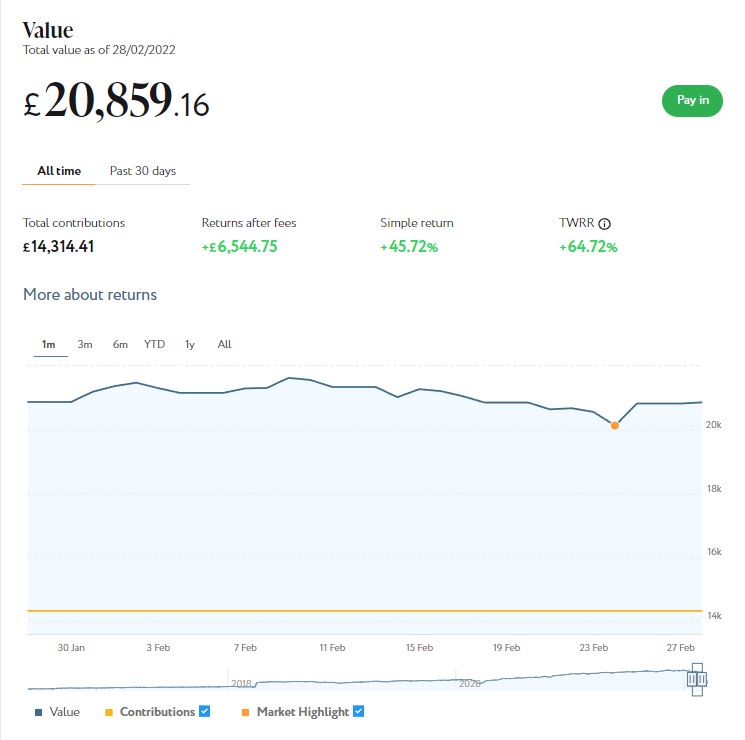

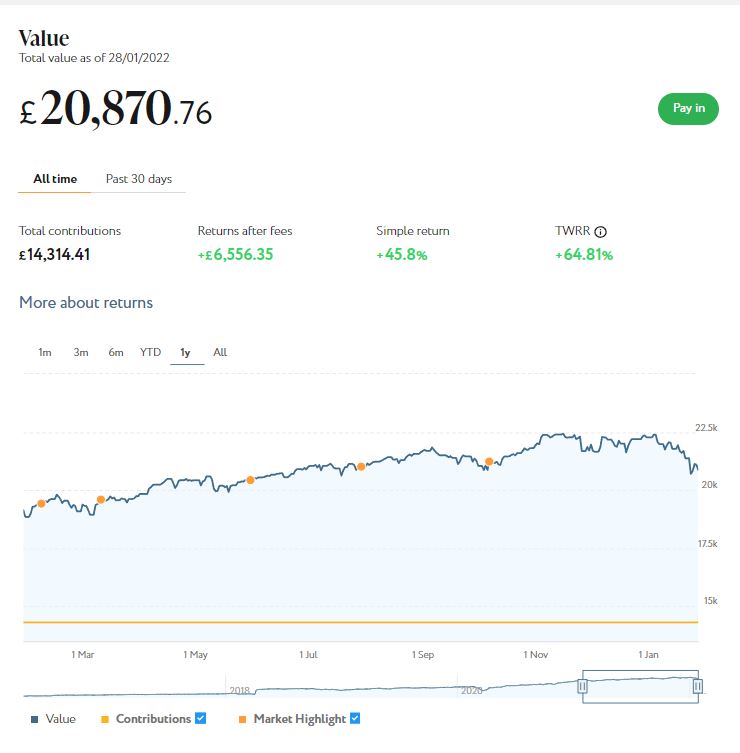

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

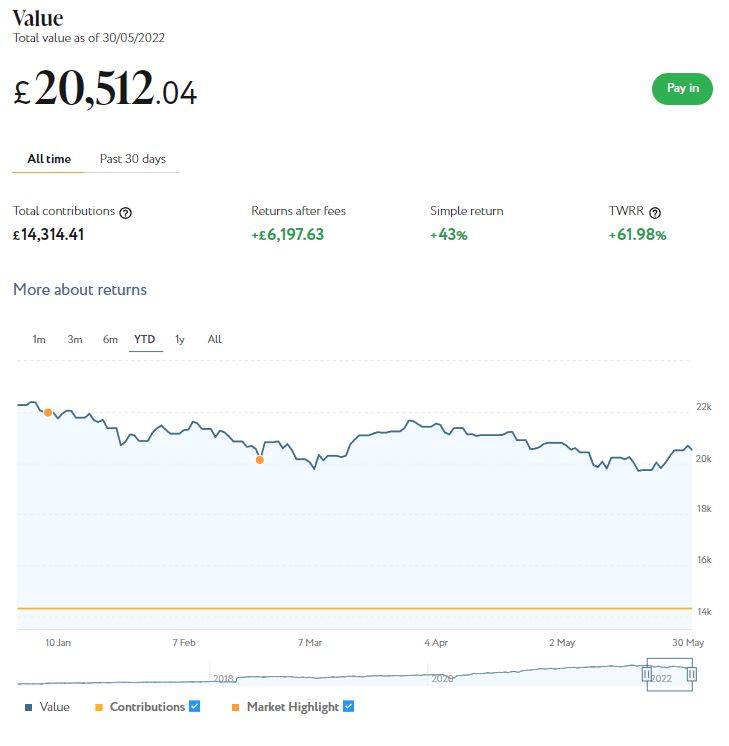

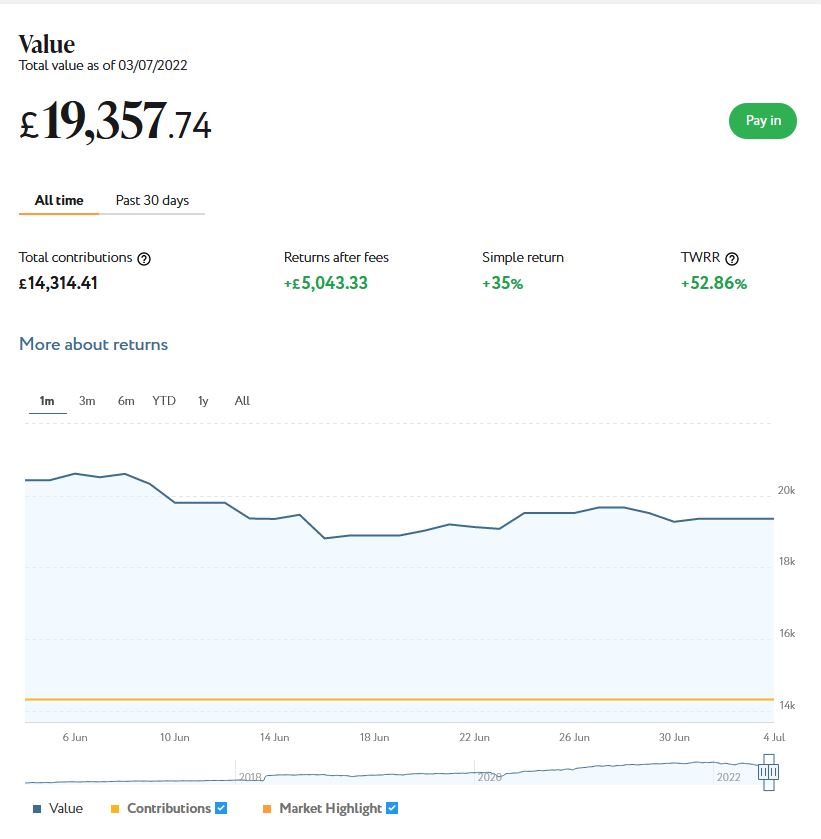

As the screenshot below of performance last month shows, my main portfolio is currently valued at £19,357. Last month it stood at £20,512 so, after another challenging month, that is a fall of £1,155.

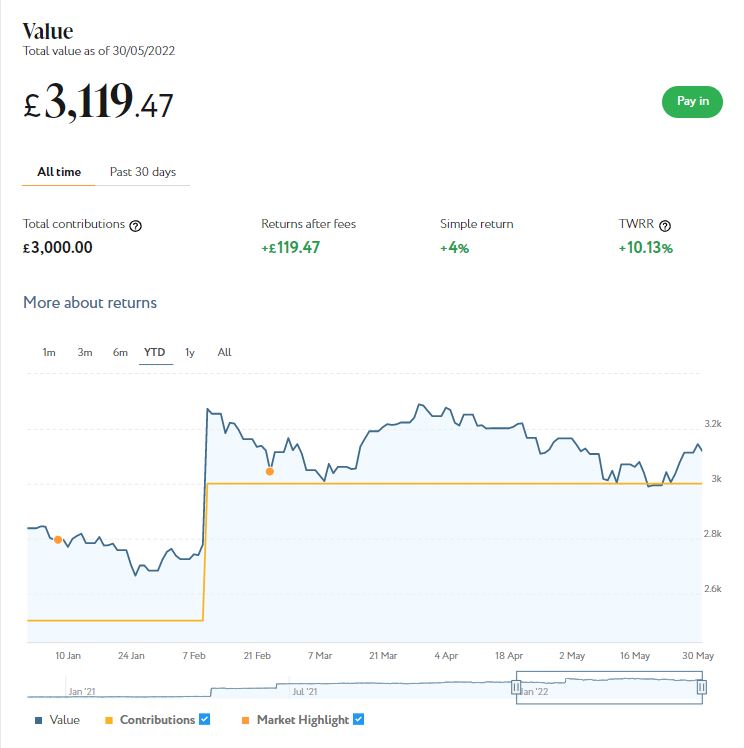

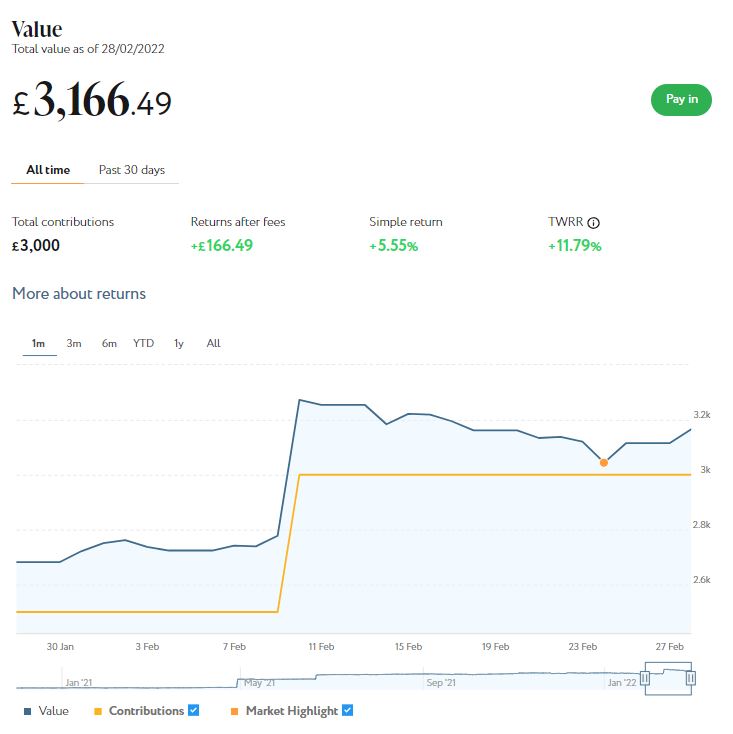

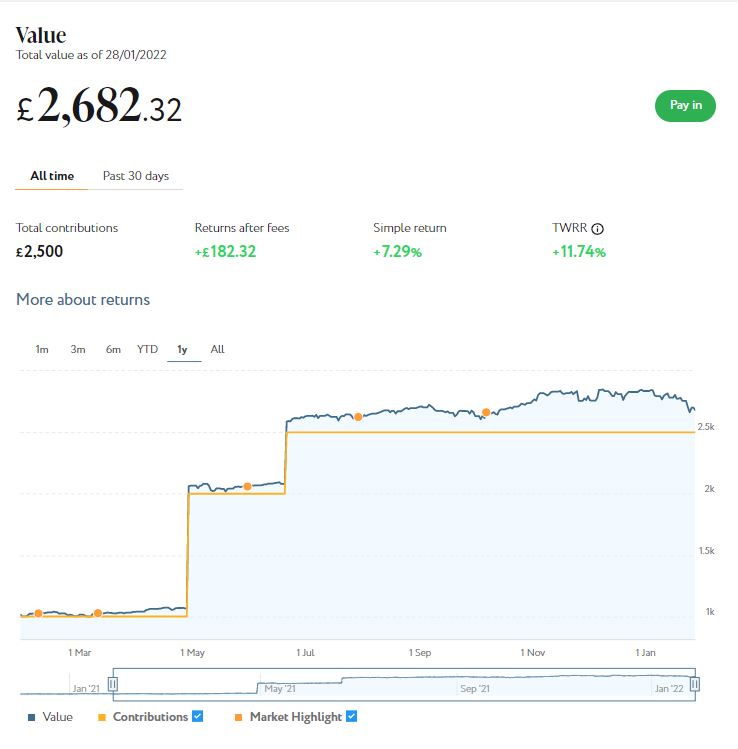

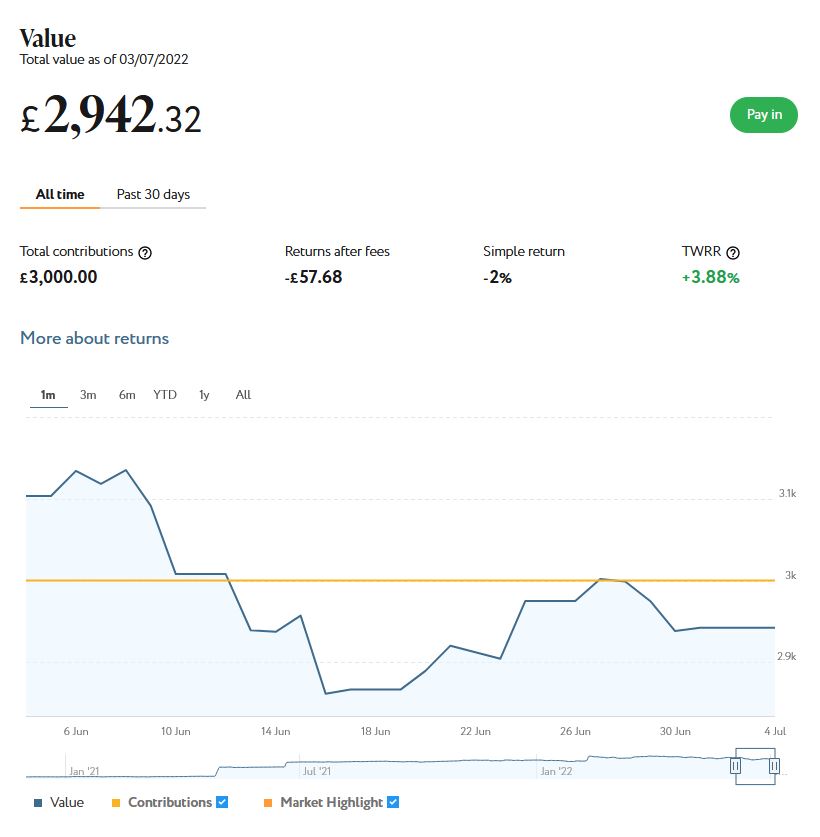

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £2,942 compared with £3,119 last month, a fall of £177

Here is a screen capture showing performance over the last month.

There is no denying these are disappointing results. Though as I’ve noted previously on PAS, you do have to expect ups and downs with equity-based investments. And over the last few months there’s been no lack of volatility in world markets, caused by rising inflation, the war in Ukraine and the aftermath of the pandemic (among other things).

- It is, however, worth noting that since I started investing with Nutmeg in 2016, and despite everything that has happened this year, I have still made a total net return on capital of 28.79% (or 52.94% time-weighted).

While performance this year has clearly been disappointing, I have no doubt there will be an uptick at some stage, and am considering topping up now while asset values are low. I definitely don’t plan to sell up, as that would only crystallize my losses this year and leave me unable to take advantage when – as I fully expect – things turn around again.

I should also mention that I selected quite a high risk level for both my Nutmeg accounts (9/10 for the main one and 5/5 for Smart Alpha). This has served me well generally, but I’m sure investors who selected lower risk levels will have seen smaller falls over the last few months. If you also have a Nutmeg portfolio and plan to withdraw from it soon, there is certainly a good case for switching to a lower risk level now.

You can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your annual ISA allowance, based on my experience over the last six years, they are certainly worth considering.

If you haven’t yet seen it, check out also my blog post in which I looked at the performance of Nutmeg fully managed portfolios at every risk level from 1 to 10 (as mentioned, my main port is level 9). I was actually pretty amazed by the difference the risk level you choose makes. If you are investing for the long term (and you almost certainly should be) opting for a hyper-cautious low-risk strategy may not be the smartest thing to do.

I talked about the performance of my Kuflink and Assetz Exchange investments in my June update and also in this recent blog post. I don’t therefore plan to provide in-depth reports about them on this occasion. I will just say that both are continuing to provide steady returns for me, with a lot less ‘excitement’ than my equity-based investments!

As I said a few weeks ago, in these turbulent times I believe P2P/crowdlending platforms such as the two mentioned are well worth considering. Not only are the rates of return higher than those on offer from banks and building societies, they are relatively unaffected by ups and downs in the stock markets. P2P loans aren’t a way of hedging your equity-based investments directly, but they do help spread the risk.

- To be clear, nobody should put all their spare cash into Kuflink, Assetz Exchange or any other P2P/crowdlending platform, but in my view (and experience) they are certainly worth considering as part of a diversified portfolio.

My investment in European crowdlending platform Nibble (as mentioned last time) continues to perform as advertised. My latest investment was in their Legal Strategy. These are loans that are in default and facing legal action. Nibble buy these loans at a heavily discounted rate and then seek to recover as much as possible of the money owed. The minimum investment is 10 euros and the minimum period is six months. I invested 100 euros for 12 months initially at a target annual interest rate of 12.5%.

The Legal Strategy comes with a deposit-back guarantee. This is a guarantee to return the full investment amount at the end of the investment period and a minimum yield of 9% per year. The actual yield depends on how successful recovery efforts prove, so in practice you may end up with a return of anywhere between 9% and 14.5%. All has gone to plan so far, but I will obviously continue to report on this in the months ahead.

- I recently updated my original review of Nibble, which you can read here if you wish. You can also sign up directly on the Nibble website if you like [affiliate link].

Also as mentioned last time, I also recently set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (about £412) copying an experienced eToro trader called Aukie. As of today my investment has fallen to $473, which I guess in the current circumstances isn’t too bad. In any event I am looking on this as a long-term investment so obviously won’t be judging it yet. I am also considering a further investment with eToro, possibly in one of their themed portfolios.

Moving on, I had another article published on the always-excellent Mouthy Money website. This one is titled Starting Your Own Business With a Franchise. If you harbour an ambition to be your own boss, a franchise can be a great way of achieving this. My article sets out some hints and tips for choosing the right opportunity and making the most of it.

- I also liked this recent article on Mouthy Money by my fellow blogger Shoestring Jane on The Best Places to Make Money From Your Old Clutter.

Finally, I enjoyed a short break in Criccieth, North Wales, at the end of June. I won’t go into detail about this here, as I plan to write a separate blog post about it soon [now published}. But I will say it was a very enjoyable, relaxing holiday, and I definitely hope to return there before too long. I stayed in a lovely sea-front apartment about five minutes’ walk from Criccieth Castle. Here is a photo taken from the castle showing the main beach…

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers 🙂