Accountants are trained and experienced in all aspects of the tax system. They have both theoretical and practical knowledge of how the system works and how the (complex) rules are typically interpreted by HMRC. And they have to keep themselves up to date with the endless legal and procedural changes.

Also, unlike HMRC, an accountant is four-square on your side. They will advise you on the best way to organize your affairs to minimize your tax liability. They will answer any questions you may have, e.g. what records you need to keep. When the time comes, they will (if you want them to) compile your accounts and submit the relevant figures to HMRC in your tax return. And if any queries or problems arise, they will act on your behalf to try to resolve them.

A further benefit of having your accounts prepared by an accountant is that HMRC will know that a finance professional – someone who speaks their language – has compiled them. Other things being equal, this is likely to mean they will be more inclined to accept the figures and not dispute them.

Even if you aren’t self-employed or running a business, there may still be a strong case for getting an accountant to help with your taxes. Many older people, for example, have multiple streams of income, from stocks and shares to ISA accounts, property rentals to pensions. Some of this income may be taxable and some not, and varying tax rates and tax-free allowances may apply. Most accountants are more than happy to provide a service to people in this situation as well.

There is, of course, one drawback to engaging an accountant, and that is the cost. This will probably amount to a few hundred pounds a year (maybe more in some cases). Not to pay this, however, is in my view a false economy. A good accountant is likely to save you at least as much in unnecessary tax as they cost you. And the reassurance (and relief) of having a finance professional on your side when any queries with taxation arise is impossible to put a price on (but extremely valuable).

Of course, finding a good accountant who offers a service suitable for your needs isn’t always straightforward. And the amount they charge varies considerably. If you are looking for a keenly priced and easily accessible service, you might therefore like to check out what my friends at Simply Tax have to offer.

The Simply Tax Option

Simply Tax is a service run by professional accountants that provides a simple and inexpensive method for preparing and submitting tax returns to HMRC. They operate mainly online and are therefore able to keep charges to a bare minimum (starting from as little as £90). They say their service is for:

First time tax filers

Sole traders

CIS subcontractors

High earners (£100K+)

Landlords

Investors

Company directors

People living abroad

Anybody who needs a tax return

As the name indicates, Simply Tax aim to make the process of drawing up and submitting a tax return as simple as possible. In a nutshell, they say their procedure is as follows:

Create your free online account (just need your full name and email address)

Once verified, go into your user area and complete your personal information

Select the button to start your tax return (you’ll be taken to a screen to answer a few questions)

Once you’ve paid and been checked for your identification, simply drag and drop the information requested

We will do all the leg work and prepare the tax return for you

We’ll upload a draft tax return for you to review and approve electronically

Once you’ve approved, leave it to us to submit to HMRC

Although all of this is done online, you will be allocated a personal tax adviser whom you can contact at any time with any questions.

Simply Tax say their service will save you lots of time (they estimate between 70-80%) compared with filing your return yourself. They also estimate that their service is up to 50% cheaper than using a traditional high street accountant or tax advisor.

Finally, Simply Tax are fully regulated by the ICAEW (Institute of Chartered Accountants in England & Wales), providing added reassurance.

If you are looking for a straightforward, cost-effective way of preparing and submitting your annual tax return, in my view Simply Tax is well worth checking out. Okay, if you run a multi-million pound business empire it may not be for you. But if you are like most of us and just need a friendly, professional accountancy service who won’t charge an arm and a leg, they could certainly fit the bill.

As always, if you have any comments or questions about this post, please do leave them below.

Disclosure: This is a sponsored post on behalf of Simply Tax. If you click through any of the links and make a purchase, I will receive a commission for introducing you. This will not affect the fee you pay or the service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

You can read my full review of Nutmeg here. You can also see how my own Nutmeg stocks and shares portfolio has been performing over the last year or so in my monthly Coronavirus Crisis updates (here’s my latest May 2021 update).

Table of Contents

Nutmeg Risk Levels

One of the many things I like about Nutmeg is that you can choose the risk level for your portfolio and any pot within it. In the case of a fully managed Stocks and Shares ISA such as mine, you can choose between risk levels of 1 (ultra low risk) and 10 (highest risk).

With other investment products and styles on Nutmeg, the scale may be different. For example, with a Smart Alpha portfolio, the risk range you can choose is between 1 and 5.

In the case of my main portfolio, I set the risk level near the top of the scale at 9/10 and have kept it there since I opened my account in April 2016. I felt I could afford to be bullish, as I don’t have any living descendants (my partner Jayne passed away a few years ago and we didn’t have children). And I didn’t have any particular purpose in mind for this portfolio, so was willing to take a few more chances with it.

As regular PAS readers will know, my Nutmeg ISA has performed very well for me. At the time of writing it is showing an overall profit of 57.71 percent, even after a tumultuous year due to Covid.

Recently, however, a reader named Kevin asked if I knew whether the high risk level I chose had any impact on my return, or whether I would have had a similar return with a lower risk level. It was a good question and one I hadn’t really looked into before, so I decided to check. I have to admit the results surprised me.

Researching Performance

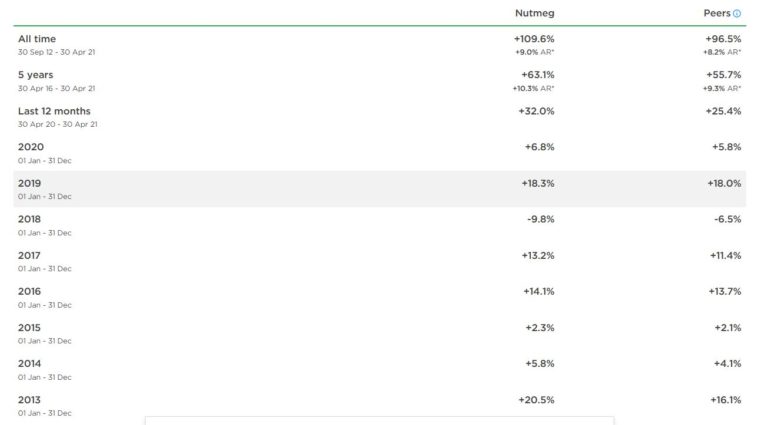

For a fully managed Nutmeg stocks and shares portfolio like mine, the good news is you can can research performance yourself on this page of the Nutmeg website: Use the slider to set the risk level from 1 to 10 and you will be able to see the net returns for the risk level in question over a range of periods. Here are the figures for a 9/10 portfolio such as mine.

As you can see, for the five-year period to 30 April 2021, overall performance is quoted as +63.1%. That is slightly above the +57.71% currently showing for my portfolio over a similar (but not identical) period. There are various reasons why the figures may differ, notably that I added to my investment at various times over the last five years rather than investing one lump sum at the start. But the numbers are close enough to appear reasonable to me.

As you will see, even though this is a level 9 portfolio, in every year bar one (2018) it has produced a positive return. Anyone investing in a level 9 portfolio from Nutmeg’s launch in September 2012 will have seen the value of their portfolio more than double.

So What About Lower Risk Portfolios?

Obviously I am not going to reproduce the table above for every other risk level. Here though is a table showing the five-year performance of every fully managed Nutmeg stocks and shares portfolio from risk level 1 to 10.

Risk Level

5-Year Performance %

1

+1.7

2

+11.1

3

+17.2

4

+23.5

5

+31.2

6

+37.0

7

+47.4

8

+55.9

9

+63.1

10

+67.0

I hope you will agree this makes interesting reading. Over a five-year period, as you can see, risk level has made a huge difference to performance achieved. Anyone choosing risk level 1 will have seen a return of just 1.7% over that period. That looks poor to me – you would almost certainly have done better putting your money in an ordinary bank savings account. And there were actually two years – 2017 and 2018 – when the value of a level 1 portfolio went down. Okay, it was only by small amounts, but even so it is hard to see any good argument for opting for the lowest risk level .

By contrast, the higher up the risk scale you go, the bigger the returns have been. Yes, there has been more volatility, but even so over most time periods – and certainly when investing for at least five years – higher risk portfolios have significantly out-performed lower-risk ones.

Of course – as I always have to say – past performance is no guarantee of what happens in future. Even so, looking at these figures makes me glad I opted for a high risk level initially, and having done this analysis I intend to continue doing so. I may even raise my risk level to the maximum 10!

One other thing I should mention is that if you are thinking of withdrawing money from your Nutmeg account soon (in the next few months, say) there is then a strong case for reducing risk level. This should help protect your capital in the event of a downturn.

Nutmeg’s Flexible Options

As I said to Kevin – who has a level 6 portfolio – if you are happy with the returns you are getting from Nutmeg and increasing the risk might cause you sleepless nights, there is of course a case for not rocking the boat.

But if you want to test the water without risking too much, Nutmeg does offer a few options. For example, you could create a new ‘pot’ with a higher risk level to see how it compares going forward. You could use new money for this and/or transfer some of your existing pot over. You don’t have to switch your entire portfolio to a higher risk level if this would worry you.

You can also have pots with different investment styles. In my case, as well as my fully managed main portfolio, I have a small Smart Alpha portfolio (mentioned earlier). As discussed in this blog post, Smart Alpha portfolios are managed by J.P. Morgan’s Asset Management team. As well as allowing Nutmeg investors to tap into the expertise of this leading investment house, these portfolios are ESG integrated, meaning that environmental, social and corporate governance considerations are factored into every investment decision. These portfolios are therefore suitable for investors for whom ethical considerations are especially important.

You can have multiple pots with different risk levels and/or investment styles. You can also change risk levels or investment styles any time you like. Nutmeg does just caution about chopping and changing too often, as this can incur additional charges. But there is no reason you shouldn’t take advantage of the flexibility Nutmeg offers if your needs or circumstances change or you just want to try something different.

It’s also worth mentioning that you are only allowed to invest in one tax-free ISA of each type per year (stocks and shares ISA, IFISA, cash ISA, etc.). However, if you have a Nutmeg account, you can invest in as many different pots within that ISA as you wish (as long as you don’t exceed your total annual ISA allowance of £20,000). This can provide valuable diversification compared with putting all your money into one single investment product.

Conclusion

As I said above, I was genuinely surprised to see how big a difference risk level made to overall performance with a Nutmeg Fully Managed Stocks and Shares ISA. And obviously I’m glad I opted for a high risk level initially, as doing so has clearly paid off for me.

Of course, nobody knows what will happen in the months and years ahead. It is still possible that opting for a lower-risk portfolio could prove a good decision as we move into a post-pandemic world with all its uncertainties. But personally I hope to see a strong economic recovery and am willing to accept a reasonable degree of risk in order to capitalize on this. You might see this differently, of course. But I hope that at least comparing the historical performance of portfolios at different risk levels will help you decide how best to proceed, whether you’re new to Nutmeg or an existing investor.

Closing Thoughts

I am obviously a fan of Nutmeg and have a significant amount (by my standards!) invested with them. You can read my full review of Nutmeg here if you like..

Of course, I am not a qualified financial adviser and everyone should do their own ‘due diligence’ (and/or take professional advice) before deciding to invest. In addition, you shouldn’t consider investing with Nutmeg (or anyone else) unless you have paid off any interest-charging debts and have at least three months of easily-accessible savings in case of emergencies.

Based on my personal experiences with Nutmeg, though, I am happy to recommend them. They provide a simple, easy-to-understand investment platform, the customer service is excellent, and certainly in my case the results to date have exceeded my expectations.

If you have any comments or questions about this post or Nutmeg in general, please do leave them below.

Disclosure: This post includes referral links. if you click through and open an account with Nutmeg, I will receive a commission for introducing you. This will not affect in any way the product or service you receive. Indeed, as mentioned above, it will entitle you to six months’ portfolio management entirely free of charge. All investments carry a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

Almost everyone loves getting something for free, and in this digital age it is easier than ever to get freebies. So why do so few people take advantage of the great opportunities on offer?

In some cases, people simply aren’t aware that such opportunities exist. However, the main reason for people not actively pursuing freebies is that they are suspicious of getting something for nothing – they believe that there is some sort of catch involved. Alternatively, they might assume that the freebies available are cheap, low quality or not worth the effort. Neither is necessarily true.

Whilst some freebies are undeniably low cost or in sample-size proportions, there are a lot of really great products and services available too. The trick is to identify what product niches you are specifically interested in, then target the offers accordingly. This can yield better results than scanning offer websites with no real intent, and is less labour-intensive if hunting for offers is not something you actively enjoy.

Where you should look for freebies will depend on what type of niche you are targeting. For example, if you are a parent looking for baby- or child-related items, simply signing up to a manufacturer’s website will sometimes result in freebies. Occasionally they may provide the items in exchange for consumer feedback or a product review. But often they will give away items for no other reason than to encourage brand loyalty.

Literature is another good niche to target if you love a free gift. Publishing companies are always looking for people, both adults and children, to review newly published books. You have complete control over which books are sent to you, and are only required to review those which truly interest you.

If your interests are broad and you are more motivated by the thrill of receiving something for nothing, there are many websites and forums where people will list opportunities for obtaining free goods and services. The most impressive freebies are normally offered in limited quantities or for a restricted time period, so you will need to check the listings regularly to get the best deals. Signing up for emails or downloading an app which will generate alerts can make the process easier.

Some of the best free products and experiences are available to those people who are willing to put in a little effort. In particular, mystery shopping can produce great results because the company is required to reimburse you for your time. Your assignment may involve a free experience, such as eating at a restaurant or visiting a local attraction, or visiting a specific store and getting financial recompense for shopping there.

However much free time you have, and whatever your interests, you will be able to find freebies which suit you. Companies frequently send out free samples in order to generate interest in their products, and often all you need to do is fill out your name and address. If you are willing to provide something in return such as a review or completing a short survey, the freebies you receive can be even more enticing.

Disclosure: This is a sponsored post on behalf of Free Stuff websites.

If you enjoyed this post, please link to it on your own blog or social media:

Another month has passed, so it’s time for another of my Coronavirus Crisis Updates. Regular readers will know I’ve been posting these updates since the first lockdown started in March 2020 (you can read my April 2021 update here if you like).

As ever, I will begin by discussing financial matters and then life more generally over the last few weeks.

Financial

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

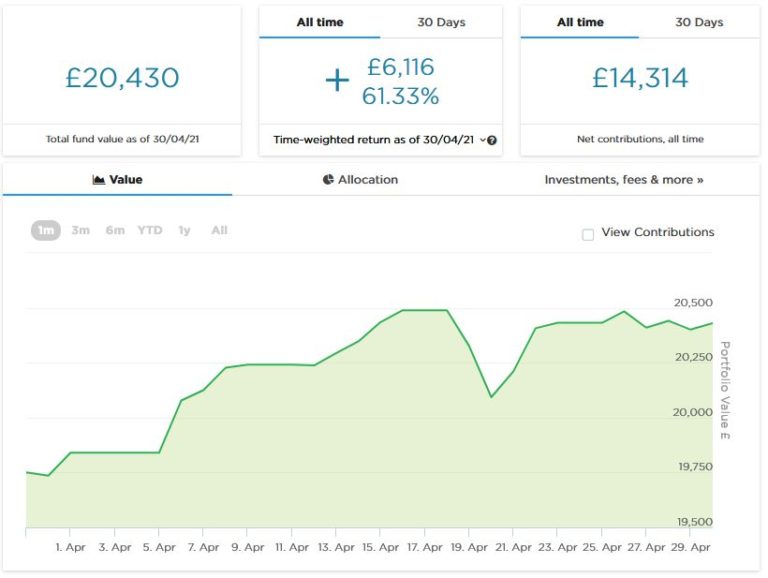

As the screenshot below shows, the value of my main portfolio rose fairly steadily in the first half of April, after which it remained around the same level (apart from a brief dip around the 20th). It is currently valued at £20,430. Last month it stood at £20,078, so overall it has gone up by £352. I am happy enough with that.

Apart from my main portfolio, five months ago I put £1,000 into a second pot to try out Nutmeg’s new Smart Alpha option. This has done pretty well, so in April I added another £1,000 from some money returned to me by RateSetter (as discussed in last month’s update). This pot is now worth £2,067. Here is a screen capture showing performance in April.

I updated my full Nutmeg review in April and you can read the new version here (including a special offer at the end for PAS readers). If you are looking for a home for your new 2021/22 ISA allowance, based on my experience they are certainly worth a look.

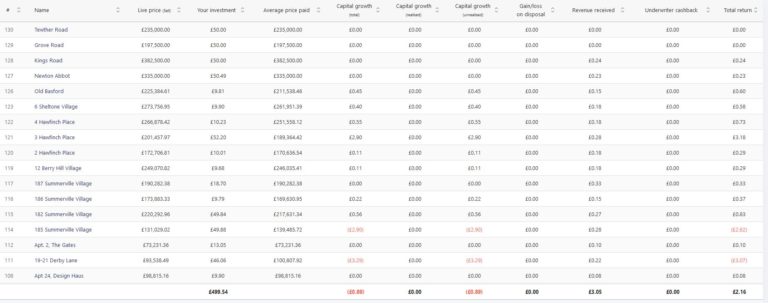

I also added £400 (from RateSetter again) to my initial test investment of £100 with Assetz Exchange. As you may recall, Assetz Exchange is a P2P property investment platform that focuses on lower-risk properties (e.g. sheltered housing on long leases). I put £100 into this in mid-February and (as mentioned) another £400 in April. Since then my portfolio has generated £3.05 in revenue received from rental (equivalent to an annual interest rate of about 10% on my original £100 investment). Here’s my current statement in case you’re interested:

As you can see, even though I have only invested £500, I already have a well-diversified portfolio. This is a particular attraction of Assetz Exchange in my view. You can actually invest from as little as 80p per property if you really want to proceed cautiously!

You may also notice that some of the properties in my portfolio have gone up in value and some have gone down. This makes it a bit harder to judge overall performance compared with an equity-based investment like Nutmeg. The property values quoted by Assetz Exchange represent the best price you can sell at currently on the exchange, which is where all investments on AE are bought and sold. But they are only really relevant if you want to buy or sell that day. By contrast, Property Partner (a somewhat similar P2P property investment platform) quote a value for each property based on an independent surveyor’s valuation every 6-12 months. That means the values displayed on Property Partner are more stable, but of course they are only theoretical as there is no guarantee that this valuation would be achieved if the property was put on the market.

In case you’re not aware, everyone has a generous £20,000 tax-free ISA allowance in the current tax year (2021/22). However, for some reason the government only allows you to invest in one of each type of ISA in any particular.tax year. So you can only put new money into one stocks and shares ISA per year, but you can invest in a cash ISA and/or IFISA as well if you wish – just as long as you don’t exceed the £20,000 total limit. In the 2021/22 tax year I am therefore investing in a Nutmeg stocks and shares ISA and an Assetz Exchange IFISA. This gives me additional diversification compared with investing in just one type of ISA.

Moving on, I heard last month that I will not be eligible for any more SEISS income support payments for the self-employed. Along with many other self-employed people, my income took a hit when the pandemic struck and this money from the government came in very useful (though I do thankfully have a personal pension and other investments as well). However, I have become a victim of the rule that says to receive SEISS your average self-employed income must represent at least half of your total income.

For the first three rounds of SEISS that was indeed the case. However, the latest round of payments incorporates another set of tax returns (2019/20) when calculating average income. Because my income was lower in these accounts (partly due to the pandemic) my four-year average is now less than what I draw from my personal pension. So at a stroke I am no longer eligible for any more support. It’s not the end of the world, but I do find it bizarre that a scheme intended to support self-employed people whose livelihoods have been affected by the pandemic can cut off completely when your average income drops. Commiserations to any PAS readers who may have found themselves in a similar situation 🙁

Personal

In April, as I’m sure you know, some of the government’s lockdown restrictions finally began to be lifted.

I was glad to be able to go for a swim for the first time since Christmas, and have been doing so twice a week since it became possible again. I am a member of the David Lloyd Club in Lichfield which has two pools, one inside and one out. Although I’ve heard that you have to book slots at some swimming pools, that has never been the case at DL Lichfield, and in fact in many ways it feels reassuringly normal. Of course, you have to wear a mask as you enter the building, but thankfully not in the changing rooms or the pool 😀

I have just been told that if the pools get very busy, DL staff ask people to wait in the changing rooms until others have left. I haven’t witnessed this myself and don’t think it happens very often, but am happy to place this info on record.

What I do find bizarre is the rules about buying and consuming refreshments. The club room (aka coffee shop) at DL Lichfield is open for the purchase of drinks and light meals, but you can’t consume them within the building. You are, however, allowed to sit at a table in the club room (no need for a mask) to read and relax or just stare at the four walls. But heaven help you if you try to eat or drink anything.

I was told by a staff member that it was okay to take a drink to the outdoor pool as long as I was going for a swim, but not if I simply wanted to lie on a sunbed. Even though I am fast becoming a connoisseur of strange lockdown rules, this one seems barmy to me and I’d love to know how DL Lichfield plan to enforce it (“Unless you get in that pool in the next five minutes, I’m taking your coffee away.”). I’d like to support the DL club room/coffee shop, but the incomprehensible rules have defeated me. So I’m now taking a flask of tea and a biscuit with me and having that on the poolside or in the changing room after my swim. So far no Covid police have come for me.

I have also been pleased (and relieved) to have my hair cut again, six months after this was last done. Thankfully I didn’t have to queue up, as my hairdresser comes to me and cuts my hair in my conservatory. We have both had Covid jabs and agreed to dispense with masks and just kept the door and window open (thankfully it was quite a warm day). Again, it all felt reassuringly normal.

I haven’t so far taken advantage of the reopening of pub gardens, largely because it has been so cold (and wet) most days. It’s good to see at least some of my local pubs open again, but a shame they still aren’t allowed to open inside as well as out. Last year we had Eat Out to Help Out at a time when there were more Covid cases and deaths then there are now (just one death yesterday, I read). I am looking forward to May 17th when pubs and restaurants can reopen inside as well, but believe this has been delayed too long personally.

I am probably one of the few people who didn’t watch the Line of Duty finale. Indeed, I haven’t watched any of the series, as it didn’t really appeal to me. For one thing it sounded downbeat and depressing, and life has been grim enough recently. But also, it appeared a bit too complicated for my liking. Especially as i grow older, I find following series with large casts and labyrinthine plots increasingly challenging. I can remember laughing (affectionately) at my dad when he expressed confusion at the plot of some TV detective show, but I am obviously going down the same route myself now 😮

I have watched a couple of shows I enjoyed this month, though, so thought I’d share details in case anyone fancies giving them a try.

The first is an Amazon Prime Video series called Upload. This is a dystopian science fiction tale, set in a not-too-distant future when a method has been found for transferring people’s minds at the point of death (or before) to a virtual afterlife. This service is provided by a number of large corporations. They employ minimum-wage ‘angels’ in large warehouse-like offices to monitor these worlds and support the clients who live in them (at least, until their money runs out). It is quite a dark concept, but full of laugh-out-loud moments and some great characters. There is also a mystery in it, and a romance between a female ‘angel’ and one of her (deceased) male clients. It’s well worth a watch if you like something a bit different (and have Amazon Prime Video, of course).

I am also enjoying a US fantasy series called The Librarians (see below). I originally caught a couple of episodes on an obscure Freeview channel and decided I’d like to watch the whole (four) series from the beginning. Doing that proved a bit more challenging than I anticipated, but eventually I managed to track down a DVD box set on eBay.

The Librarians is a tongue-in-cheek fantasy series with a certain retro feel to it. It reminds me a bit of the old Avengers TV show in its heyday (with Diana Rigg as Emma Peel).

The Librarians are a group of misfits who are recruited to work at the mysterious Library, a place where magical artefacts of all kinds are stored. Early in the first series magic is released into the world again, having been suppressed for many centuries. In each episode the Librarians investigate some mysterious incident and try to stop evil individuals deploying magic for nefarious ends, generally using their intelligence rather than violence.

Again, it’s hard to explain in a few words, but you soon get the hang of things. And the characters, while perhaps excessively goofy at times, are all endearing in different ways. The Librarians is really old-fashioned family entertainment (with little if any swearing) and none the worse for that. If you can get hold of it – I’m not sure whether it’s on any streaming services – it offers an enjoyable (and at times hilarious) drop of escapism, something I guess many of us need at the moment.

As always, I hope you are staying safe and sane during these challenging times. If you have any comments or questions, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

According to the Department for Business, Energy and Industrial Strategy (BEIS), there are now roughly a million homes in the UK with solar panels.

Mine is one of them. We had ours fitted in April 2011, just in time to benefit from the highest Feed-In Tariff (FIT) before the rate was slashed by over half.

I hadn’t really given the panels a lot of thought since then. I submitted meter readings every three months, and a few days later a handy, tax-free payment appeared in the bank account.

In March 2019, though, I had a couple of builders doing repairs to the woodwork around the eaves. This was an awkward job that involved having scaffolding put up. Anyway, one of the builders (a guy I have known for several years and trust) asked if I would like the panels cleaned while they were up there. “They’re filthy,” were his exact words.

He quoted me £60, which seemed a good price, and clearly it made sense to have the work done while they were there and the scaffolding was up. They gave the panels a thorough clean, using large sponges and buckets of warm water with washing-up liquid.

I was intrigued to see how much difference this would make to the amount of electricity the panels generated, so I downloaded a free program called Sunny Explorer that works with my solar PV system. It communicates with the inverter (the device that turns the electricity generated by the panels into usable power) via Bluetooth to show how much electricity your panels are producing. And, thankfully, it shows historical data going right back to when the panels were first installed.

Monitoring Solar Panel Performance

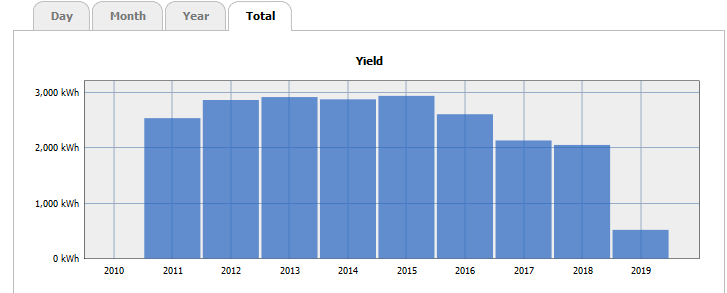

I found the data from Sunny Explorer genuinely eye-opening. First, take a look at this chart showing the total amount of electricity generated by my system year on year since the panels were installed.

As you can see (bearing in mind the panels weren’t installed till April 2011), for the first five years the total power output was pretty consistent. Then in 2016 and 2017 it dropped quite substantially, and again by a smaller amount in 2018, even though that summer was one of the hottest, driest on record. Obviously, if I was being scientific I would compare the total number of sunny days in each of those years, but I think it’s safe to assume that from 2016 onwards the build-up of dirt on the panels began reducing their efficiency.

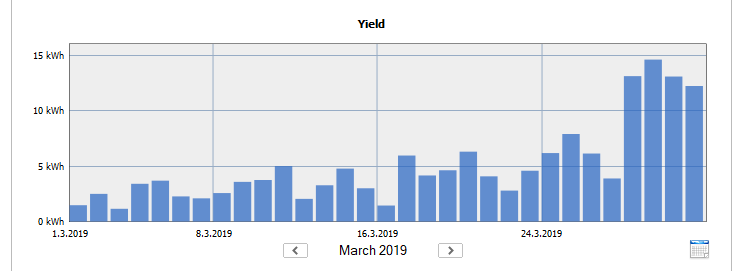

Now take a look at the monthly chart for March 2019. Can you guess what date the panels were cleaned?

Full marks if you said 27th March. The power generation was quite low that day as the panels weren’t cleaned until the afternoon, and obviously they had to be switched off while the cleaning was going on (the builders actually forgot to switch the system back on before they left, but I’ll forgive them that). Notice how much more power the panels generated in the last four days of the month, though.

2021 Update

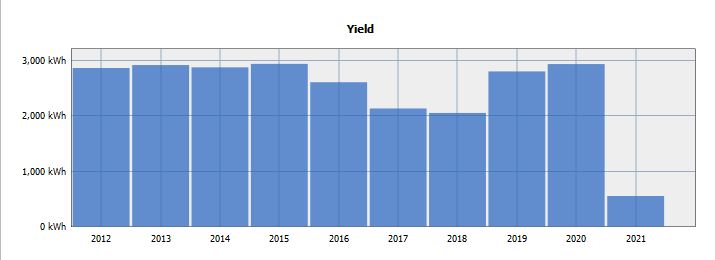

Two years on, here is a chart showing how much electricity my panels have been producing year on year. Remember, they were cleaned in March 2019.

As you can see, in 2019 and 2020 my panels were back generating at the same level they had been prior to 2016. And neither of these years featured exceptional amounts of sunshine. Obviously as it’s only mid-April now the total figure for 2021 is lower, but from comparing the month-by-month figures from previous years it is clear that they are still working well.

If I hadn’t had the panels cleaned it’s likely that their electricity production would have continued at the 2018 level (and probably lower). As it was, in 2019 and 2020 they generated an extra 1,700 kwh compared to the 2018 level, worth about £850 to me in financial terms. So that £60 I paid to have them cleaned was a very good investment!

Overall, I think the lesson from this is that it’s well worth monitoring the performance of your panels, and having them cleaned if you notice it is declining. When our panels were installed we were told that they were ‘self cleaning’ due to the amount of rain we get in the UK, but that clearly wasn’t sufficient in my case anyway!

More Top Tips

I used the free Sunny Explorer software to monitor my system. This works with inverters made by SMA Solar Technology. If you have a different make of inverter it may not work for you, but there should be some other way to check your system’s performance. Ask your installer if in doubt.

If you have trees nearby (as I do) there will probably be more birds around, and over time their droppings are likely to build up on your panels and reduce their efficiency. While dust generally washes off with a good rain shower, bird droppings may not.

Before cleaning or inspecting solar PV panels, it is essential to switch them off via the main isolating switch (in my home it’s a bright red switch next to the solar power meter). Failing to do so could result in a severe electric shock.

If you cannot safely access your panels to clean them, hire a professional to do it. Don’t get up on the roof yourself unless you have the necessary training, expertise and equipment.

A good solution for cleaning solar panels that can avoid the need for going up on the roof is a water-fed pole with a soft brush, combined with a squeegee. Avoid using abrasive tools or products in case you scratch the glass.

Avoid cleaning your panels when the weather is hot, as spraying cold water on very hot panels could cause smearing or even damage them. Instead try to clean the panels in the morning or evening or on cooler days.

Based on my experience, it may not be necessary or cost-effective to clean your panels every year, but every three to five years could be a good strategy. In any event, monitoring the output of your panels will help you decide.

Good luck, and I hope your solar panels are soon working at peak efficiency again!

If you have any comments or questions about this post, as always, please feel free to post them below.

This is an update of my original 2019 post.

If you enjoyed this post, please link to it on your own blog or social media:

I have written about property crowdfunding on various occasions on Pounds and Sense. It’s a way for ordinary individuals to invest in bricks and mortar without requiring huge amounts of capital.

Table of Contents

Why Property Crowdfunding?

Property investors get a double benefit – rent from tenants for as long as they own the property, and – in most cases – a profit if and when they sell.

Of course, property doesn’t come cheap. And even if you can stretch to buying a modest house or flat for investment purposes, you are taking the risk of putting all your eggs in one basket. As a result, many people of more modest means have concluded that property investment is not for them.

Property crowdfunding has changed all that, however. A number of platforms now exist that allow ordinary individuals the chance to buy a share (or fraction) in an investment property. Investors then receive a proportion of the rental income generated and also get a share of any profit when the property is sold (or refinanced).

A further attraction of property crowdfunding is that the platform (and its agents) take care of managing the property and tenants on your behalf. Unlike direct property ownership, property crowdfunding (or crowdlending if you prefer) is a genuine hands-free investment.

Brickowner Review

Brickowner is one of a number of property crowdfunding platforms that also includes Property Partner, Assetz Exchange and CrowdProperty. They allow investors to buy a share of individual property investments.

Brickowner focuses on institutional investments. They buy shares in large, high-return property investment deals that were traditionally only offered to institutions or high-net-worth individuals. They then offer smaller shares in these (a minimum of £500) to members wanting to invest in them.

How It Works

Before you can access the Brickowner platform, you will need to register on the site and confirm that you are allowed by law to invest in this type of product. This is a requirement imposed by the Financial Conduct Authority (FCA), which regulates this type of investment. In practical terms it means you will have to confirm that you meet one of the following descriptions:

High Net Worth Individual – This includes individuals who have an annual income of £100,000 or more or net assets of £250,000 or more and have made a declaration acknowledging the consequences of making investments based on financial promotions that have not been approved by an FCA-authorised firm.

Self-certified Sophisticated Investor – This includes individuals who have prior relevant investment experience and have made a declaration acknowledging the consequences of making investments based on financial promotions that have not been approved by an FCA-authorised firm.

Representative of a High Net Worth Body – This includes companies and partnerships with at least £5 million net assets and trusts with assets of £10 million.

Investment Professional – Including corporate investors and SIPP or SSAS professional service providers.

You will also be required to answer some questions to confirm that you understand the nature of the investments that can be made on the platform.

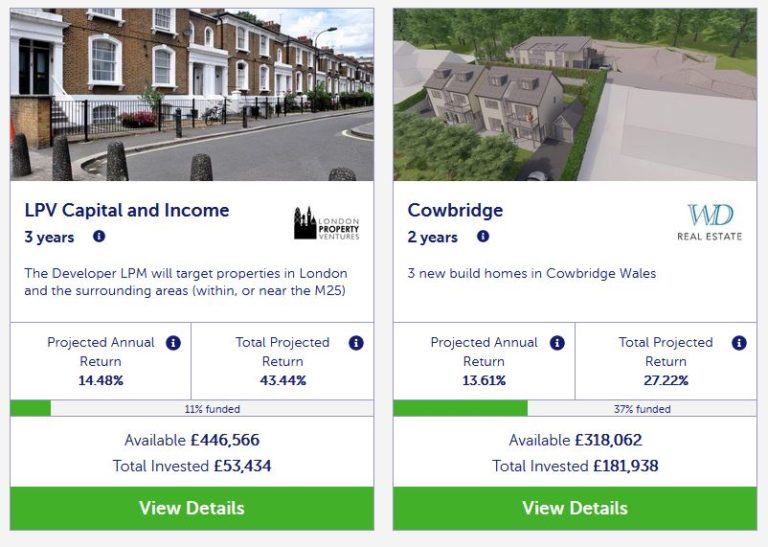

Once you are registered (and not before) you will be able to browse from the range of currently available property investments, such as the example below:

If you see a current project you like, you can invest in it, from £500 up to the maximum available. You can (and probably should) build a diversified portfolio by investing in a number of different properties. You can add funds and increase the size of your portfolio any time you want.

Investments have a fixed term: anything from one to five years. During that time you may receive dividends from any rental income received. These are added to your account and available to withdraw or reinvest. You also receive a share of any profits along with return of your capital at the end of the investment period.

In common with other property crowdfunding platforms, the pandemic has caused delays – in some cases a year or longer – to some projects on Brickowner, As far as I am aware no projects have failed completely, though.

Secondary Market

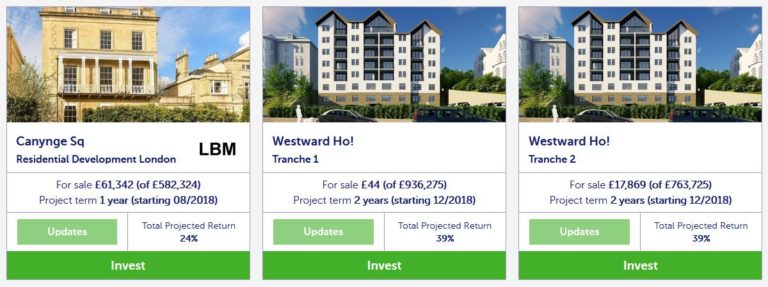

Brickowner recently introduced a secondary market where investors who need to release funds before the end of an investment term can put their share up for sale to other members. Here is a screen capture showing part of the secondary market currently.

As you may notice, some of the projects on the secondary market have less than £500 available. I asked if this meant you could therefore invest less than £500 in these cases, but was told no. Here is the exact reply I received:

£500 is the minimum investment in both the primary and secondary market. The reason there are smaller amounts on the secondary market is that there is a taxi-rank system, whereby available shares are listed and allocated in order of listing to a queue of buyers. So if I wanted to invest, say, £520 in Tamlaght, and there were no other prospective Tamlaght share buyers ahead of me BUT there were only £120 worth of shares available, I would have to wait until £520 worth of shares were available before my transaction went through. Prospective Tamlaght buyers in the queue would have to wait until my order had been filled before they moved forward in the queue.

In effect, then, you would have to place a bid for at least £500 of the project in question, and would have to wait till additional sellers materialized before getting anything. That is probably not ideal, but I can understand that Brickowner want to avoid the situation where some investors end up with tiny holdings in certain projects.

Charges

Brickowner fees are outlined within the property term sheet for each specific investment. There is no charge for depositing money with Brickowner, and no charge at the end of the investment period when your money and (hopefully) profits are returned to you.

My Thoughts

Brickowner offers an interesting option for people who want to add property to their investment portfolio. As mentioned above, there is a good case for doing this both in terms of dividends and capital growth, and to diversify your overall portfolio.

The Brickowner website is attractive and professional looking. One thing I have noticed is that most of their investment opportunities fill up very quickly. That is good insofar as it indicates that Brickowner is succeeding in attracting investors who believe in the proposition being offered. On the other hand, it does mean that at any particular time there may not be many (or any) projects to invest in. You will therefore need to build your portfolio gradually.

As mentioned above, Brickowner has a minimum investment of £500. This is not as low as some platforms (e.g. Assetz Exchange will let you invest as little as 80p) so it may be less suited to investors on a limited budget. But on the positive side, they are transparent about the fees they charge, and it is good that no fees are imposed for depositing or withdrawing money. It’s also good that a secondary market now exists for investors who wish (or need) to exit early.

As you can see from the screen capture above, the projected returns on investments with Brickowner are at the higher end for property crowdfunding platforms. Of course, this generally means the risks are higher as well. In any event it is important to read the financial information on each project carefully, to ensure that the investment aligns with your own needs and goals. Bear in mind also that some projects offer income as well as the potential for capital appreciation, while others aim for capital growth only.

During the coronavirus pandemic and lockdown, property transactions slowed considerably and many commercial property values in particular fell. However, there is clear evidence that a recovery is now under way. My own view is that there are good opportunities at present for property investors, but obviously in this uncertain time there are never any guarantees. Every investor needs to assess the situation carefully in light of their personal circumstances and tolerance for risk and proceed accordingly.

Investor Protection

The returns on offer from Brickowner are significantly better than you would get from a bank savings account at present, but clearly they don’t carry the same level of protection. For example, you are not protected by the Financial Services Compensation Scheme, which will refund up to £85,000 if a bank with which you have an account goes bust.

On the other hand, your money is invested in bricks and mortar, so it’s unlikely you would lose it all. A further level of protection is that – in common with other property crowdfunding platforms – your money is invested via an SPV (Special Purposes Vehicle). This is effectively an independent company with responsibility for the project in question. If Brickowner were to go bust, funds in the SPV would be protected and returned to investors once the property was sold.

Even if Brickowner were to go under before your money was invested, your funds are paid into a separate, ring-fenced client account. If the platform went belly-up the day after you sent the money, your funds would simply be returned to you.

Overall, then, whilst investing in Brickowner is clearly not as safe as leaving your money in the bank, the measures set out above do provide a reasonable level of protection (and reassurance). As with any investment, however, the higher potential returns on offer come with a greater risk of loss. In my view (and I’m not a qualified financial adviser, just an individual who has put thousands of pounds of his own money into property crowdfunding) Brickowner offers a reasonable balance between risk and reward. But clearly, you should invest only as part of a balanced portfolio combined with other, more liquid types of investment. .

If you would like more information about Brickowner and to set up an account, just click through any of the links in this post.

Disclosure: The links in this post are affiliate links. If you click through and set up an account at Brickowner and make an investment with them, I may receive a fee for introducing you. This will not affect the terms or returns you are offered. Please note also that I am not a registered financial adviser and nothing in this post should be construed as personal financial advice. Before making any investment it is important to do your own due diligence, and seek advice from a qualified financial adviser if you are in any doubt how best to proceed. All investment carries a risk of loss.

If you have any comments or questions about Brickowner or property crowdfunding in general, as always, please do post them below.

Note: This is a fully revised and updated repost of my original article about Brickowner.

If you enjoyed this post, please link to it on your own blog or social media:

Spring is here at last, and for once there is plenty of good news in the air.

The vaccine roll-out is going well, cases are way down, and across the UK Covid restrictions are being relaxed. I had my first swim for four months yesterday in the outdoor pool at David Lloyd Lichfield, and tomorrow will be having my first haircut in almost six!

To celebrate all of this, I thought it was high time for another giveaway. I have therefore got together with some of my fellow UK bloggers to offer a bundle of top-quality health and beauty products worth almost £400 for the lucky winner. You can see the full list below ↓↓↓

This giveaway has been arranged and co-ordinated by my blogging colleague Emma at www.MakeMoneyWithoutAJob.com. Do take a look at her site, where (among other things) you can sign up for a free, daily £10 prize draw. There are also articles on money-making topics from How to Make £1,000 Every Month to Online Jobs for Teens, Free Money Offers to How to Make Money Watching Netflix. Literally something for everybody!

Table of Contents

The Bloggers Taking Part

Please show your support for all the bloggers taking part in this giveaway by visiting their blogs. They are:

One lucky winner will receive a health and beauty bundle worth almost £400.

Included in this bundle is:

La Roche-Posay Effaclar Duo+ Blemish treatment 40ml

Marc Jacobs Perfect 50ml

Glo32 Teeth Whitening System

CYO Makeup Bag Top Up Bundle

Olay Regenerist Luminous Anti-Ageing Brightening And Protecting Face Cream SPF20 50ml

Footner exfoliating socks

Liz Earle Cleanse and Polish 50ml

Champney’s Calm Reed Riffuser

Champney’s Slumber Body Butter 300ml

Maybelline Sky High Mascara x 2 (Black; Waterproof)

EcoTools – Daily Essentials Total Face Brush set

L’Oreal Paris Men Expert Get Better With Age Anti-Ageing Duo Giftset for him

Too Faced Hangover Wash Away the Day Cleanser 125ml

La Roche-Posay Anthelios Ultra-Light Invisible Fluid Sun Cream SPF50 50ml

Champney’s Weekend Treat Gift Set

Terms and Conditions

1. There is one top prize of a health and beauty bundle.

2. There are no runner-up prizes.

3. Open to UK residents aged 18 and over, excluding all bloggers involved with running the giveaway.

4. Closing date for entries is midnight on 30 April 2021.

5. The same Rafflecopter widget appears on all the blogs involved, but you only need to enter on one blog.

6. Entrants must log in to the Rafflecopter widget, and complete one or more of the tasks – each completed task earns one entry in the prize draw.

7. Tweeting about the giveaway via the Rafflecopter widget will earn five bonus entries into the prize draw.

8. One winner will be chosen at random.

9. The winner will be informed by email within 7 days of the closing date and will need to respond within 28 days with their delivery address, or a replacement winner will be chosen.

10. The winners’ names will be published in the Rafflecopter widget (unless the winner objects to this).

11. The prizes will be dispatched within 14 days of the winner confirming their address.

12. The promoter is www.MakeMoneyWithoutAJob.com

13. By participating in this prize draw, entrants confirm they have read, understood and agree to be bound by these terms and conditions.

The Giveaway

Complete any or all of the Rafflecopter entry widgets below to enter.

One final small point is that if a winning entry comes from following someone on social media, the organizer (Emma) will check before awarding the prize that the winner is still following the account in question. If they aren’t, they will be disqualified and a new winner drawn. So, please, don’t follow and immediately unfollow, as your entry won’t then count.

Good luck, and here’s hoping we can all look forward to even better times soon 🙂

If you enjoyed this post, please link to it on your own blog or social media:

Today I am pleased to bring you a guest post from Haydn Martin, a UK blogger whose website is called Perpetual Prudence.

Haydn explores ideas relating to retail investing and other personal finance topics on his way to finding the solution to Lifetime Investing…

In his guest post today he discusses the risks of investing in ‘safe’ assets.

Over to Haydn, then…

Risk might be the most important consideration when making investment decisions (like what to invest your ISA allowance in). Get it wrong and you could be retiring on a pittance, running out of money during retirement, or even worse – asking friends/family for handouts. Risk must be taken seriously and properly dealt with, especially when you’re living off your investment portfolio.

It seems strange, then, that risk is so poorly understood by so many.

One aspect of risk that is particularly neglected is the chance of a truly disastrous event crushing the value of the asset in question. The chance of these catastrophic events is ‘unthinkable’ and so not really taken into account by people when making investment decisions.

This is the wrong approach. In this piece, I will be talking about some of the hidden risks of the ‘safest’ asset classes and their implications for the investor.

Table of Contents

Cash

What could go wrong with pilling up cold, hard cash under your mattress? This, surely, I hear you claim, entails no risks at all?

As you might have guessed, not quite. First, there are the practical considerations. If you actually store large amounts of cash somewhere in your house, that cash will promptly disappear if you get burgled, if your house burns down, or if your partner changes their mind about this whole marriage thing and does a runner (with the money). If at some other secure location, it can always be pinched. Cash held at a bank is dependent on the fortunes of said bank. As 2008 showed, this might not be the safest place in the world. The government will cover you up to £85,000, sure, but for those of you lucky enough to have more than this, you’re relying on the prudence of bankers.

Aside from the physical, one must also consider the monetary. Inflation, that cruel mistress, is the biggest threat to holders of pound sterling. It may be practically non-existent these days, but casting your mind back to the 70s will remind you of the real damage inflation can inflict on your purchasing power. If inflation is higher than the rate of interest you earn on your cash (that pile under the mattress is earning 0%) then you’re losing money in real terms. You’re actually getting poorer without realising it.

Government Bonds

Taking this cash and dumping it into government bonds may seem like a sensible thing to do, then. The government is probably less likely to fail than banks. These bonds earn some kind of interest to help combat inflation, too. Happy days.

Unfortunately, most of these rates of interest are dependent on the whims of the Governor of the Bank of England, not directly linked to interest rates. If the govna’ wants to maintain low interest rates to stimulate the economy after, say, a global pandemic has put a halt to business activity, they may maintain low interest rates, even with substantial inflation. This means that your bonds will be earning a negative real return. What’s also nasty about these bonds is the fact that their value fluctuates with inflation and interest rates. This means that you don’t actually receive the yield to maturity unless you hold the bond…to maturity. Otherwise, your yield may be substantially lower.

The government acknowledges this problem with bonds and issues index-linked versions to counteract this inflation risk. These bonds return some percentage above inflation, supposedly ensuring that you maintain your purchasing power (and then some). This, however, relies on the fact that the government calculates the rate of inflation correctly. How confident are you in the competence of the government? There is also the chance that the government defaults on their outstanding debt. This is unlikely under a fiat system (because they can always just print more money), but it remains a risk nonetheless. Reckless monetary policy can lead to veeeery high inflation, which is difficult to stop (just look at Argentina for a contemporary example). In this instance, your bonds would be worth precisely 0.

Shares

It would seem then, that relying entirely on the government may not be the best idea. What about companies?

The apparently safest form of investing in shares is investing in whole markets (or parts of markets) using index funds or ETFs. The highest level of diversification one can get is by investing in every market, using a global ETF/index fund. One of the main risks here is fake diversification. A lot of these global trackers should actually be called ‘US & Friends’. For example, if we look at the Vanguard FTSE Global All Cap Index Fund, we see that the US makes up nearly 60% of the fund. If the US performs badly, these trackers will too. There is also the chance that the company doing the tracking goes bust, meaning you will lose some of your investment. This is a pretty unlikely scenario, but it’s a possibility nonetheless.

An alternative approach is to keep your hard-earned money inside the UK, by investing in a basket of British companies. This leaves you rather exposed to the fortunes of the UK. If we prosper in the next 20-50 years, it will probably be a good move. If not, UK companies might not do so well. You are already likely to be heavily exposed to the UK via your job or some other way (like owning a house here), so it may be a good idea to diversify internationally a bit.

Many assets have this problem, come to think of it. If you plan on moving to the French Riviera in ten years’ time, you are going to want some exposure to French assets before you move. Let’s say France does really well in this time period but the UK does not. France is now more expensive, which is fine for French people because they have been getting richer, too. It’s not so fine for you, for whom France is getting more and more expensive. There is also the exchange rate risk to consider. You don’t want to convert your fortune into Euro only to find that it’s not worth all that much.

Just a closing remark on shares. It’s not clear that they will rise over and above inflation, even over long periods of time. The market is a complex system. The 7% return that everyone seems to be claiming the market naturally drifts towards is not guaranteed in practice.

Asset Management

What about just letting someone do your investing for you? Professionals with years of experience and good track records? That’s safe, right?

When you use these managers, you are putting your fortune into their hands. It’s really hard to judge if these are competent hands or not. These funds can dazzle you with past performance and a good sales pitch, but that is not a good indicator of strong future performance. Take the recent Archegos Capital Management blow-up as a warning (it was the largest trading loss in history). You just never really know what these managers are doing and what risks they’re taking.

Other Assets

Seeing these risks, some prefer to shun the financial world in its entirety and invest in real stuff. Stuff they can see and touch that has a good track record of maintaining value. Things that have historically been valued highly – watches, cars, wine, oil, gold, silver, etc. – could be a good bet. The problem here is that the value of these items is very much dependent on tastes at the time you come to sell. The green initiative could accelerate, crushing the value of cars and oil, for example. Or the demand for watches may just simply die off for no particular reason. I see this as unlikely – things that have historically been highly valued don’t tend to lose their allure overnight without some kind of devaluing mechanism – but it’s possible all the same. The point is, these things are valued pretty much out of thin air.

Some assets are not valued out of thin air. Those that generate cash-flow can have their values reasonably estimated. A small business, for example. Or a property that you rent out. The risks here are specific to each individual case.

Summing Up

Everyone is an investor. You can’t escape it. Everything that can be valued fluctuates in real value. Every day you are making investment decisions, so you might as well know what you’re getting yourself into (or make sure your financial adviser does!).

A big part of this awareness is knowing about the risks of investments, especially the disastrous, not-often-mentioned risks discussed in this post. Nothing is risk-free. Everything can go to 0 and you can lose all your money as a result, making for a pretty grim retirement. It’s just something you have to live with. You have to be a bit paranoid when composing your portfolio or you could get burnt, and burnt badly.

Of course, risk should not be the only factor when making investment decisions. Your specific circumstances (your goals, your age, your income, etc.) must also be taken into account. But risk should be, in my view, the primary consideration. To thrive, first you must survive.

Thank you to Haydn for an interesting and thought-provoking article. Please do check out his excellent blog at Perpetual Prudence as well.

I do very much agree with Haydn that every investment (or savings option) carries some risk. It is therefore essential to be aware of the downside/worst-case-scenario with any investment, while setting this against the potential rewards. Taking excessive risks is clearly to be avoided, but being too risk-averse – and therefore missing out on profitable investment opportunities – can be counter-productive as well. That applies especially to younger people, who may have 30 or 40 years before they retire.

It is also, in my view, crucial to avoid the mistake of putting all your eggs in one investment basket. As regular readers will know, I am a big fan of diversifying your portfolio as widely as possible – across different investment types, asset classes, platforms and risk levels. That way, if one or two investments do go south, hopefully they will be more than compensated by others that succeed.

It is also important to remember that investing is a long-term game. You should generally have at least a five-year time-horizon, to allow for the inevitable ups and downs in markets to even out.

As ever, if you have any comments or questions on this post – for me or for Haydn – please do post them below.

Disclaimer: Everybody’s needs and circumstances are different, and nothing in this post should therefore be construed as personal financial advice. Everyone should perform their own ‘due diligence’ before investing and seek advice from a qualified financial adviser if in any doubt how best to proceed. All investment carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

It’s the start of April, so time for another of my monthly Coronavirus Crisis Updates. Regular readers will know I’ve been posting these updates since the first lockdown started in March 2020 (you can read my March 2021 update here if you like).

As ever, I will begin by discussing financial matters and then life more generally over the last few weeks.

Financial

I’ll begin as usual with my Nutmeg stocks and shares ISA, as I know many of you like to hear what is happening with this.

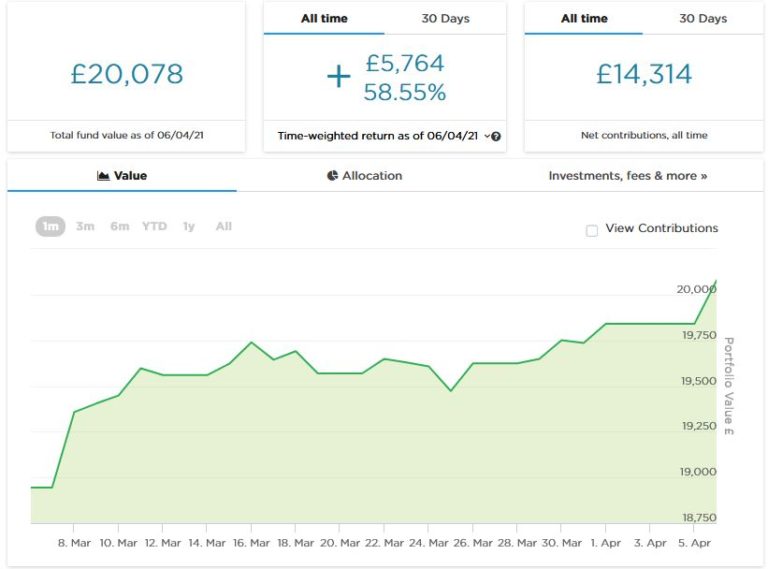

As the screenshot below shows, following a dip in early March my main portfolio has generally been on an upward trajectory. It is currently valued at £20,078. Last month it stood at £19,155, so overall it has gone up by £923. I am very happy with that, obviously.

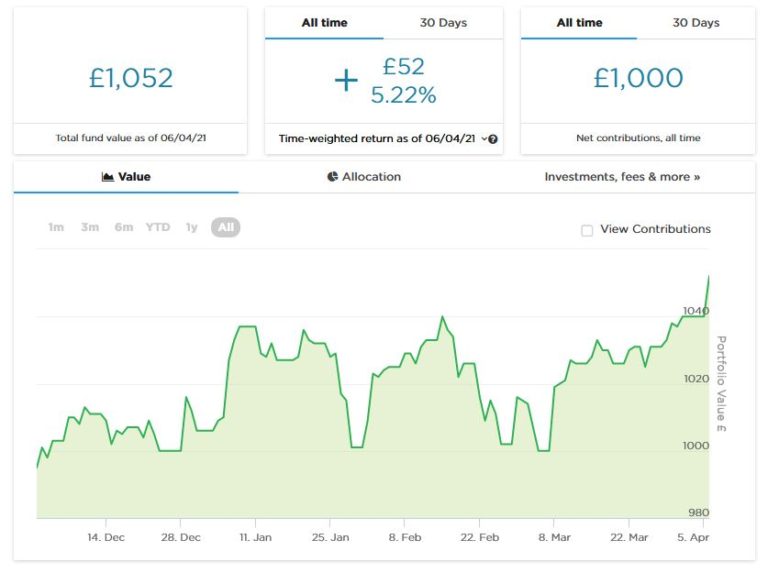

Apart from my main portfolio, four months ago I put £1,000 into a second Nutmeg pot to try out Nutmeg’s new Smart Alpha option. This pot has seen some ups and downs, but right now it is up to £1,052. That’s an increase of 5.22% in four months, equivalent to nearly 16% annually. Here is a screen capture showing performance to date. Obviously, though, it is still too soon to draw any firm conclusions from this.

You can see my in-depth Nutmeg review here (including a special offer at the end for PAS readers). If you are looking for a home for your new 2021/22 ISA allowance, based on my experience they are certainly worth a look.

That aside, last month was a mixture of good and bad news on the investment front. Probably the worst news was discovering that Buy2LetCars had gone into administration. Regular readers will know that I invested in two cars with this car loan platform. For three years everything went like clockwork, but then the FCA stepped in and froze their bank accounts due to concerns over how the company recorded the value of car leases in their accounts. This happened just before monthly payments were due to go out to investors in February. Initially Buy2LetCars said they would engage with the regulator to address their concerns, but then everything went quiet till it was announced that an administrator had been appointed to take over the company.

I don’t know any details of what has been going on with Buy2LetCars. I am still not entirely convinced that the FCA acted in investors’ best interests by freezing the company’s bank accounts just as they were about to make payments to investors. But it does certainly appear that the directors of Buy2Let Cars have questions to answer as well.

Personally I am most sorry for people who invested large sums with Buy2LetCars in recent months, including in some cases (I understand) their entire pensions. To be clear, though in the past I did recommend Buy2LetCars based on my experiences as an investor with them, I have never advocated putting all your money into this (or any other) investment platform. As things stand now, when you deduct the monthly repayments received from the capital I originally invested, I am about £10,000 down. That is clearly a major blow but not a total disaster for me.

As I said above, the company is now in the hands of the administrators and I have sent my claim form to them. It’s important to note that Buy2LetCars does still have assets including the cars themselves and the value of the leases, which their key worker clients are still paying. So in due course I am hopeful that some payments will be made to investors, though obviously it will only be a fraction of what we were promised. The letter from the administrators says they will be writing to the company’s creditors ‘within 8 weeks’ with their proposals, so hopefully I will hear something by mid-May. But any payouts are likely to take a lot longer than that to arrive, of course.

On a brighter note, I had all my money returned as promised by P2P lending platform RateSetter after the company was sold to Metro Bank. I didn’t invest a lot with them, but it was nice to get my capital back plus interest and the £100 bonus on offer when I first invested. I shall be reinvesting this money soon 🙂

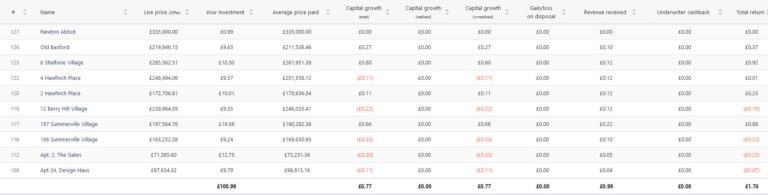

You may also recall that last month I made test investments with two other platforms. One of these, Assetz Exchange, is a P2P platform that focuses on lower-risk property investments (e.g. sheltered housing on long leases). I put £100 into this in mid-February. Since then my portfolio has generated 77p in capital growth and 99p in revenue received, so £1.76 in total. Obviously that doesn’t sound like much, but it works out as an annual interest rate of around 10.50%. Here’s my current statement in case you’re interested:

I also put a small amount into the European loan crowdfunding platform Nibble (the first time I’ve tried investing with a non-UK platform). It’s all going well so far and I get weekly updates from them confirming how much interest has been added to my portfolio. Again, it’s too early to offer any firm opinions about Nibble, but so far everything appears to be on track. My full review of Nibble can be found here.

Finally, a couple of the loans I invested in with the P2P property investment platform Kuflink were repaid (with interest) last month, and I duly reinvested the money in other loans.

I have a diversified portfolio of loans with Kuflink paying annual interest rates of 6 to 7.5 percent. These days I generally invest a few hundred pounds per loan at most (and often £100 or less). My days of putting four-figure sums into any single property investment are definitely behind me now!

You can read my full Kuflink review here. They recently passed the milestone of £100 million loaned, and say that since their launch no investor has lost money with them. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year, with built-in automatic diversification. And I’d particularly draw your attention to their revised and more generous cashback offer for new investors. They are now paying cashback on new investments from as little as £500 (it used to be £1,000). And if you are looking to invest larger amounts, you can earn up to a maximum of £4,000 in cashback. That is one of the best cashback offers I have seen anywhere (though admittedly you will need to invest £100,000 or more to receive that!).

You might also enjoy reading this post titled Home Finance Tips for the Rest of 2021 on the Cibes Lifts website, to which I contributed some suggestions.

Personal

March was another dreary month of lockdown, though it was at least nice to see the schools back (albeit with mandatory masks in classrooms).

The vaccine roll-out continues to go well and the numbers of Covid cases, hospital admissions and deaths are all falling rapidly, giving hope for the weeks and months ahead. And, of course, we are into the spring now, with longer, brighter days and – at some point – the prospect of some warmer ones!

I have gone ahead and booked a short break in North Wales at the start of July. It’s at an Airbnb apartment near Abersoch in North Wales. Here’s a photo from the Airbnb website…

The apartment has a wonderful, near-beachside location with good facilities and great sea views, so I’m really looking forward to going. It will be my first ever visit to Abersoch (and the furthest I have ever ventured along the Lleyn Peninsula). I did try to get there last year but sadly had to cancel due to Covid.

In March I had my annual review with my financial adviser, Mike (if you want to know why a money blogger needs a personal financial adviser, here’s a link to my blog post where I discuss this). Of course we did this as a video call this year. We used Microsoft Teams, a software tool I hadn’t tried before, but it all worked smoothly enough. I am certainly learning a few new IT skills as a result of lockdown!

I talked about my discussion with Mike and some issues it threw up in this recent blog post, so I won’t go over all that again here. Suffice to say, it made me think hard about how my financial situation will change (for the better) when I qualify for the state pension later this year. I didn’t entirely agree with all of Mike’s advice, although I do understand that it was prudent and sensible. But as I should be in quite a healthy financial situation when my pension kicks in, I intend to start spending a bit more rather than simply letting it accumulate year on year till finally it passes on to my sisters (much as I love them). If you haven’t read my post about this, do take a look, and let me know which of us you agree with!

I had hoped by now to have had my first swim since Christmas. But my local David Lloyd Leisure opened their outdoor pool on Monday last week only to close again on the Tuesday (when I went!) due to a problem with the water chemicals (I suspect this could be a euphemism…).

This week it’s too cold for outdoor swims – for me at any rate – so I am counting off the days till Monday 12th April, when they will be able to open their indoor pool as well. The changing rooms will be open too, and I assume I will be able to get a warming mug of hot chocolate in the club room, even if I have to stand up to drink it 🙂

Obviously it is good news that the country is (very) slowly coming out of lockdown. I am also looking forward to meeting friends and family in pubs and restaurants again, though until mid-May this will only be permitted outside in England, so a lot will depend on the weather. But even if I end up waiting till hospitality venues are open inside as well as out, I will look forward to seeing the garden of my local pub full of visitors again!

It does worry me that the government keeps moving the goalposts with regard to easing lockdown measures. In particular, while we were originally told that all restrictions would end by June 21st, it seems increasingly likely this may not be the case. It’s particularly disappointing to hear some of the government’s scientific advisors saying we may be stuck with mandatory face-masks and social distancing well into next year or even longer. I really hope this isn’t the case. The vast majority of vulnerable people have been vaccinated now and this is reflected in the big falls in deaths and hospital admissions. We need to accept that risk can never be entirely eliminated and get back to normal life again now.

As always, I hope you are staying safe and sane during these challenging times. If you have any comments or questions, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I thought I would share something a bit different with you – a sideline opportunity you may not have considered before.

There is a huge demand for people to appear in TV shows. In recent years “reality television” featuring ordinary people in a range of scenarios, from dating to surviving in inhospitable places, has become extremely popular.

Talent shows are also massive. If you can sing, dance, tell jokes, do magic tricks, perform acrobatics, or have some other talent people might like to watch, there is almost certainly a show you can apply for.

Other shows offer the opportunity for successful – and talented – contestants to become celebrities in the field concerned. For example, many of the winners and runners-up in cookery shows such as Masterchef and The Great British Bake Off have gone on to obtain publishing contracts, and in some cases started their own restaurants. One example is the 2005 Masterchef winner Thomasina Miers, who now runs a chain of Mexican restaurants called Wahaca and has also presented several TV cooking series.

Another very popular option is quiz or game shows – from Pointless to Bargain Hunt. A steady stream of contestants is needed for these shows, which is many cases are broadcast daily. And the best news is that these shows are open to people of all ages and backgrounds, and you don’t need any special skill or talent to take part.

Although the coronavirus pandemic (and government response to it) put a temporary brake on some shows, many found ways to get round restrictions, e.g. by redesigning their sets to allow for social distancing. And right now, with restrictions being eased across the UK as virus cases plummet, large numbers of shows are looking for contestants again 🙂

Some shows offer the possibility of winning life-changing sums (Who Wants to be a Millionaire is the classic example). In other cases the rewards are more modest – but even the chance of winning two or three thousand pounds on a show such as The Chase is not to be sniffed at. And under UK law, cash and prizes won on TV shows are entirely tax-free.

Even aside from the chance of fame or fortune, being in a TV show can be an exciting and eye-opening experience. You will see what goes on behind the scenes at your favourite shows, and watch them with fresh appreciation in future. And, of course, you will have an experience to remember and tell friends about for years to come.

Researching and Applying

You can find out what shows are currently recruiting by contacting the production companies directly. See who makes a show that you would like to appear on and look them up online.

There are also websites that publish contestant calls. BeOnScreen is a good place to start. Here is one opportunity that was being advertised there at the time of writing:

Iain Stirling’s CelebAbility is BACK for another series and is looking for fun and outgoing teams of 3 to take part!

This physical, comedy game show sees teams of 3 go up against a squad of celebrities in a series of hilarious games with the chance to win some fab prizes including a cash prize.

Groups can include; friends, family, colleagues or people you share the same hobby with.

If you and your team are aged 18 and over, fun and outgoing who love to play games and get involved in fun challenges, then we want to hear from you!

Depending on when you read this, the opportunity above may have gone, but others will certainly have taken its place. Note that many shows are recorded in or around London, so if you live near the capital you will have a certain advantage. In the interests of diversity, however, many also film in other parts of the UK, so definitely don’t be put off if you live elsewhere.

As well as calls for contestants, BeOnScreen also advertises free tickets for TV shows, and occasionally calls for extras. If all or any of these things interest you, it’s well worth signing up on the website to receive email updates when new opportunities are posted.

There’s much to be said for applying for new shows such as those listed on BeOnScreen, as the competition for places isn’t as intense as established shows. But there are plenty of the latter that need a steady supply of contestants too, of course.

One top tip is to go for daytime shows, which typically have smaller audiences than prime-time shows, again resulting in less competition from other would-be contestants. But do ensure that the prizes are worth your while before sending in an application.

Before applying to be on any show, I recommend finding out as much as you can about it. If a particular physical or problem-solving skill is required, try to practise this as much as possible. And if it requires specialist knowledge, bury your head in some relevant books, and then get a friend or partner to test your knowledge.

It’s also a good idea to practise your public-speaking skills, especially if this is something that doesn’t come naturally to you. If possible, get a friend to assume the role of the show’s host and ask you some likely questions. This will help prepare you for the show itself, and will also assist you with the auditioning process (see below).

Auditioning for a Show

To be accepted as a contestant, you will normally need to go through some sort of audition. Big TV talent shows such as Britain’s Got Talent and X Factor typically hold open auditions in major cities across the country.

To get on a quiz or reality show you will probably have to perform an initial test/audition as well, though it will be lower key. These auditions are generally held by specialist companies who recruit contestants for the shows. They will assess such things as your personality and appearance, your general knowledge, and how well you communicate. They may also check your ability to cope in stressful circumstances.

One time I was auditioning for a quiz show, I was completing a pen-and-paper test in the company of half a dozen other applicants. Suddenly an alarm went off. We all looked at one another, unsure what was going on. The representative then returned to the room and assured us there was nothing to worry about. She revealed later that this was simply a standard test they used to ensure that potential contestants didn’t crumble under pressure!

As mentioned above, if you’re auditioning for a quiz show you may be given a series of questions to answer, either verbally or in writing, to test your general knowledge. If you find them all easy, it may nevertheless be a good strategy to deliberately get one or two wrong. As our American friends say, nobody likes a smartass! And the companies like to recruit contestants with all levels of knowledge and skill, so the watching audience can relate to them as ‘ordinary people’.

One other top tip for aspiring quiz show contestants is to try to stand out from everyone else. The researchers are looking for people who will come across on TV as outgoing and interesting, rather than dull and anonymous.

This needs to be judged carefully, of course. You don’t want to make yourself appear too weird, or the researchers may fear you will be a loose cannon. If (like me) you’re naturally somewhat introverted, though, it will help a lot if you can make an effort to present yourself as a bit more outgoing. If you can manage ‘bubbly’, so much the better!

A distinctive hairstyle or item of clothing may give you an extra edge as well.