Today I have a sponsored guest post for you on behalf of Top Subscription Boxes. On their website they advertise a huge range of subscription box services.

With these services, you receive a new and exciting product (or selection of products) every month. You can subscribe for as long or as short as you want (subject to minimum subscriptions). And as you will see, there is something to suit every taste and budget!

Whether you want to send someone special a gift they will really enjoy or just treat yourself (you deserve it!), the subscription box services listed below could provide the perfect solution. We tried all of these ourselves before bringing the very best together in one place.

So without further ado, let’s get started!

Glossybox

Whenever it comes to beauty and make-up subscription boxes. Glossybox always takes the top spot. Glossybox allows you to treat yourself with a perfect combination of deluxe and full-sized beauty product samples from top brands.

Each month they send you a great-value box loaded with the latest make-up products, tools and beauty creams – and it will only cost you £13.25 per month.

In their previous boxes they have featured well-known brands like La Mer, Nars, pedigree French brands such as La Roche Posay, and impressive budget make-up from the likes of Rimmel.

Beer Bods

Beer Bods is known as the UK’s #1 craft beer subscription service. They send you a box of 8 beers every two months. So basically you receive one beer a week, along with the story behind that beer. All subscribers receive the same beer at one time, and you can join in a live online tasting every Thursday at 9 pm. So you can enjoy a new beer with new friends every week and compare notes with them. The bi-monthly subscription will cost you £24.

Arena Flowers

Nothing can be better than seeing fresh flowers in the morning. They make you feel calm and give your day the perfect start.

Arena Flowers is a leading ethical floristry service. They deliver exciting bouquets through their monthly subscription service.

They’ve been sending out their beautiful bouquets for the last 14 years and have achieved the milestone of 10 million deliveries. Every bouquet you receive is hand-tied and arranged by one of their expert florists to create a unique bouquet just for you. You can subscribe by paying just £17 a week.

Gadget Discovery Club

The Gadget Discovery Club allows you to treat yourself or your loved ones by sending them subscription boxes containing 4 innovative gadgets they didn’t know they needed!

They say that every gadget they’ll deliver to your doorstep will help you to upgrade your home, entertainment or lifestyle. The subscription box contains everything from tech wearables to smart home devices, including Samsung/Philips kits and Google home speakers.

You just need to sign up and select your preferences so they can send you the latest exciting gadgets based on your profile. They offer a monthly subscription or you can also choose a yearly plan. The monthly option will cost you £33 per month.

BakedIn Baking Club

The BakedIn Baking Club is a baking subscription service that delivers a different recipe each month straight to your door. Once you’ve subscribed to this service, you will receive a beautiful baking box with a step-by-step recipe guide, along with all the dry ingredients you need and some extras too.

BakedIn allows you to make your favourite muffins, biscuits, cakes and cookies, to share with your family and friends. If you are one of those people who loves baking, then this is the subscription box service for you. The price is £7.50 a month.

Good luck, and we hope you find the perfect subscription box service for you or your loved ones!

Thank you to my friends at Top Subscription Boxes for some eye-opening suggestions. I would definitely like to try some of these services myself! They would also, of course, make excellent Christmas or birthday presents. Please do click through to their website and check out the other subscription box services as well!

As always, if you have any comments or questions, please do post them below.

If you enjoyed this post, please link to it on your own blog or social media:

This year I have had five vaccines in total. Three of them were for Covid-19, including my booster jab earlier this month. The other two were a flu jab and a pneumonia jab ( the latter is offered by the NHS to everyone reaching the age of 65 in Britain).

You will gather from the above that I am not an anti-vaxxer (though as my Twitter followers will know, I do have reservations about the effectiveness of lockdowns, vaccine passports and mask mandates in combatting the spread of Covid-19).

But while I accept the need for vaccines for older people especially, I know some do get side-effects from them. The most common is an aching arm. This can be very painful and make activities such as driving difficult, though thankfully for most it usually lasts no more than a day or two.

My personal experience with vaccines this year is that I got the worst side-effects from the flu jab, including waking up in the night shivering and feeling sick. With my two Oxford-AstraZeneca jabs I had almost no side-effects, and the same applies to the pneumonia vaccine. With my booster jab, however – which was Pfizer – my arm started aching quite badly and I got a stiff shoulder as well.

In my vaccine journey this year I have found a couple of things that have really helped me minimize side-effects, so I thought I would share them today.

1. Prophylactic Paracetamol

Taking paracetamol is widely recommended if you get an aching arm and/or other side effects from the vaccines. I now take a couple at bedtime on the day I have had the jab, even if at that point I have no side-effects. I continue this the next day, taking them at four-hourly intervals (you shouldn’t take them any more frequently than that) until I am confident that I won’t be getting any side-effects or they have largely subsided.

One thing you shouldn’t do is take paracetamol before having the jab as it is possible this may reduce its efficacy. Not much research appears to have been done about this, but to be on the safe side it’s best avoided.

2. Gentle Arm Exercises

I tried this with my recent Pfizer jab, and was genuinely amazed by how effective it proved in easing stiffness and pain in my arm and shoulder. Friends I have recommended this to have been impressed by how effective it proved for them as well.

The exercises I use can be found on the aptly-named Sheltering Arms website. There are five in all, with short videos to illustrate them. They are simple, easy exercises and you don’t have to do them all if you don’t want to. As I had a stiff shoulder, I also threw in some shoulder rotations (basically rotating the shoulders upwards and backwards, then down and forward again, as was recommended to me a few years ago by a physio). I found this very effective as well.

I kept doing the exercises for a few minutes throughout the day and noticed an improvement within hours. By the end of the day, my arm and shoulder were pretty much back to normal.

Obviously I am no medic, but I understand that gently exercising the vaccinated arm helps disperse the vaccine throughout your body and reduces local muscle soreness. That being the case, it would appear a good idea to start doing these exercises even before any pain or stiffness occurs, again as a prophylactic measure. At my next jab, I intend to start soon after leaving the vaccination centre!

I would also recommend that you don’t do what I have done in the past, which is spend hours hunched over a keyboard after having your jab in case you can’t do this later. That could well reduce the opportunity for the vaccine to disperse and may add to any stiffness you experience later. Get your keyboarding out of the way before you go for your jab!

I hope you find these ideas helpful and they work as well for you as they have for me. Please feel free to leave any comments or questions below as usual. I’d also be interested to hear about your own experiences with ‘vaccine arm’ and any other methods you have found helpful for addressing the problem.

Please bear in mind that I don’t have any medical training and can’t give personalized advice, only share what has worked for me. Obviously if you get more serious side-effects from the vaccine, you should contact a medical professional as soon as possible. This NHS website page has more information.

If you enjoyed this post, please link to it on your own blog or social media:

Christmas is coming, so here’s a chance to make it extra special for one lucky winner!

I’ve joined forces with some of my fellow UK bloggers in this festive giveaway with a prize valued at over£1,000 in total. That’s made up of a unique homeware upgrade package worth over £600 from Norwich-based lifestyle and homeware brand Arca, plus a cool £400 in cash. You can read more details about this amazing prize below.

Entering the giveaway is free of charge and full instructions can be found below. There are multiple ways to enter, and the more you do, the better your chances of winning. But note that where an entry requires following a social media account, you will need to continue following this account until the winner has been drawn on 20 December 2021. Before the winner is announced the organisers will check that they are still following the account in question. If not, they will be disqualified and another winner drawn.

2021 has undoubtedly been another challenging year, though (fingers crossed) we are emerging from the pandemic now and life is slowly getting back to normal. Whether you win this giveaway or not, I wish you and yours a very happy and peaceful Christmas 2021. Here’s hoping that 2022 is a better year for us all, and we can finally put the spectre of Covid in the past where it belongs!

This giveaway has been organised by my fellow blogger Neesha Rees, who blogs at Reinventing Neesha. Please check out her blog and those of the other talented bloggers taking part (listed below). And read on to find out how you could win this mammoth prize!

Your home is your sanctuary, so surround yourself with things you love.

One lucky winner will win a unique homeware upgrade package worth over £600 from Arca plus £400 in cash!

Arca Lifestyle is an eclectic lifestyle and homeware brand based in Norwich. With a range of hand-curated products from across the globe, Arca provides the latest trends to brighten any home as well as original gift ideas for those you love.

Arca has been created with the goal to help individuals find homeware pieces and prints that spark their soul, offering unique products that are not available elsewhere.

Once you have completed the above entry options, via the Rafflecopter widget below you will unlock more ways to enter. The more you complete, the more chances you have of winning.

The competition ends at midnight on Sunday 19th December and a winner will be drawn on Monday 20th December.

For full entry terms and conditions please see the rafflecopter widget below.

Christmas is barely six weeks away, and it’s a safe bet more of us than ever will be shopping online this year.

Pounds and Sense is aimed at the over-50s, so today I thought I’d set out a selection of products you can buy online suitable for people in this age category. Though in my view most would be very well received by younger people too 🙂

Quite a few of these are things I’ve received for free this year as an Amazon Vine reviewer. Others are simply products that I’ve bought for myself – or friends or relatives – and am very happy to recommend to others.

Please note that I am using some affiliate links in this article, so if you click through and make a purchase, I may receive a commission for introducing you. Of course, this will not affect the price you pay or the product you receive.

(1) Music Hat

My first thought when I received this unisex beanie hat to review for Amazon Vine was that it was just a novelty product – but it turned out to be a lot better than I anticipated!

The hat itself is made of stretchable acrylic and is warm and comfortable. It’s available in a range of colours to suit all tastes. And in addition to keeping your head warm in the winter, it boasts an LED light at the front and built-in Bluetooth earphones.

The LED light has three brightness settings, with the brightest illuminating the area in front of you quite impressively. I’ve found this useful for putting the bins out at night and (on a lower setting) to ensure I can be seen when walking at night along poorly lit roads and pavements.

The stereo headphones are surprisingly good quality. Obviously you wouldn’t expect super high fidelity, but for listening to music or podcasts on the go, they are more than adequate. Setting up a Bluetooth connection with my Android smartphone was easy, and I’ve been enjoying listening to my choice of music on my daily walks. In theory you can also use the hat for making and receiving phone calls, though I haven’t tried that myself. Even if you only use it for listening to music, though, it’s still a very nice piece of kit. And for around £20 at the time of writing, this unisex beanie hat won’t break the bank either!

I also got this two-light beanie hat (without built-in earphones) for my sister Annie. At this time of year she has to walk home in the dark from her job at a prison, and she goes running in the evening sometimes as well. Annie sent me the following mini-review: ‘That fluorescent hat is actually really good! Very bright front and back light. Great for being seen by others so makes you feel safe at dusk (I don’t run in the dark nowadays so much). Nice snug fit especially round the ears and easy to put the lights on (front and back) even when it’s on your head! Have had lots of positive comments. Definitely recommended!’

(2) Fruit Wines

I am not much of a drinker these days, but I will always make an exception for these delicious fruit wines, especially at Christmas!

Clive’s Wines is a small, family-run company based barely a mile from where I live. They offer a range of high-quality fruit wines, including damson, cherry, raspberry, strawberry, elderflower, plum and (my personal favourite) gooseberry. For special occasions they also offer a premium sparkling ‘Rhubling’ made with rhubarb.

You can order individual bottles and gift packs online for delivery anywhere in the mainland UK and Europe, with free delivery for orders of over £60 in the UK. If you are looking for an unusual gift that will also support a small local business, I can promise that you (and the lucky recipient) won’t be disappointed 🙂

You do, of course, have to be over 18 to order any product containing alcohol.

(3) Hand Warmer and Power Bank

I have two of these devices now (the first came my way as an Amazon Vine reviewer). As you may gather, they are dual-purpose devices, serving both as a hand-warmer and a power bank for charging your phone or tablet.

The product pictured above is the OCOOPA Rechargeable Handwarmer and Power Bank. This has a powerful 10,000 mAh battery and doesn’t therefore need frequent recharging. You can have three levels of heat (though I find the lowest is more than sufficient for me). It only takes a few hours to charge fully and can charge up my Android phone in under an hour.

Currently I am using this device more as a power bank than as a hand warmer, but that may change if and when sub-zero winter weather conditions arrive. For under £30. it would make a nice, practical gift for any older person (especially if they suffer from cold hands!).

(4) Amazon Echo

Unless you’ve been on Mars for the last few years, I’m sure you’ve heard of these devices. There is a growing family now. The picture above is of an Echo Show, which also has a visual display. I have one of these in my kitchen and use it all the time. I also have an Echo Dot in the bedroom, a standard Echo in the living room, and a tiny Echo Flex in my office. And I’m still thinking of getting more!

I use my Echo devices primarily for listening to music and radio. But I also regularly use them for checking the weather forecast, getting news updates (‘Alexa, read my flash briefing’), asking random questions (‘Alexa, how far is the Earth from the Moon?’), checking the time, setting alarms and timers, finding out what’s on TV, and much more. Alexa has become part of my life now, and I have to admit I actually miss her when I am away. How sad is that? 😀

In my view an Amazon Echo device would make a great gift for any older person, even if they aren’t at all tech-savvy (though they do of course need wifi to work). Once the device has been set up – which is easy enough – you can control it entirely using your voice, just using the ‘wake word’ (Alexa by default, though you can change it if you like) to activate it.

For an older person living alone especially, having an Amazon Echo device can provide companionship as well as reassurance in the event of an emergency (you can ask Alexa to call any of your contacts for you, though currently you can’t get it to phone 999). And an Echo is a present that will go on giving through Christmas and well beyond. Highly recommended.

Amazon often have some great offers on Echo/Alexa devices in their Black Friday sale.

(5) Christmas Hampers

This is quite a traditional Christmas gift, but none the worse for that. I have been sending Christmas hampers to various elderly relatives for many years, and they are always well received. The hampers include a selection of luxury food and drink that people on a limited budget wouldn’t typically buy for themselves. I often get quite in-depth feedback about what they liked or disliked about this year’s hamper and whether it was better or worse than last year’s!

There are various suppliers you can order hampers online from (Marks and Spencer have a good selection, for example). But these days I normally order from Amazon. They have a vast range from a variety of merchants, and you can easily search for the type of hamper you want (including by price, with/without alcohol, vegan/vegetarian, and so on).

Amazon also sell hampers aimed specifically at older people, such as the Traditional Treats Hamper (from Clearwater Hampers) pictured above. This costs £49 at the time of writing and includes luxury chocolates, a tin of afternoon tea, hand-baked lemon biscuits, rhubarb and custard sweets, almond biscuit thins, clotted cream fudge, and more. Guaranteed to put a smile on the face of any grandparent 😀

Of course, there are lots of other options as well, for younger folk as well as older ones. Prices range from around £20 to £200 or more if you really want to push the boat out!

(6) Red Letter Days Vouchers

Red Letter Days sell gift vouchers for a huge range of experience days, for single people or for couples.

Among other things, they include luxury spa days, hotel mini-breaks, afternoon tea (see picture above), driving experiences (e.g. supercar driving, go karting, truck driving), sky diving, hot air ballooning, river cruises, visits to historic houses/gardens, restaurant meals, and many more. Some will obviously appeal more to younger folk, but there are plenty that are equally suitable for all ages (and plenty of older people still enjoy a bit of thrill-seeking as well!).

In the last 18 months many of us have have spent months on end cooped up in our homes. So the chances are your friends or relatives will really appreciate the chance to enjoy an exciting (or relaxing) experience day such as these.

(7) Salter Electronic Scales

Finally, here’s a great, inexpensive gift for anyone who enjoys cooking.

No bowl is provided with these scales, but because of the way they work you don’t need one. You can place any container you like on the scales and press the button to zero the display (so the scales disregard the container’s weight). You can then add your ingredient and the weight (or liquid volume if you prefer) will be shown. If you want to add more ingredients, you can zero the display again before doing so. Once you get the hang of this, it’s amazingly quick and simple. I use it all the time now, and even weighed a parcel on it recently 😀 I also like the way it hardly takes up any space at all in my kitchen when stored on its side.

So there you are – seven great ideas for Christmas gifts you can buy online that any older person would be delighted to receive (and a lot more exciting than slippers or socks!). As always, if you have any comments or questions about this post, please do leave them below.

Note: this is a fully updated version of an annual post.

If you enjoyed this post, please link to it on your own blog or social media:

Many people dream of writing a novel one day, but of course actually doing it can be a daunting prospect.

If that applies to you, maybe next month’s NaNoWriMo could provide the spur you need to get started.

In case you don’t know, NaNoWriMo stands for National Novel Writing Month. It’s a challenge to write a novel of at least 50,000 words in a month, and it comes around every November. From humble beginnings in the USA in 1999, when there were just 21 participants, NaNoWriMo has grown into a huge world-wide event.

There is no entry fee for NaNoWriMo (though donations are always welcome), and no prizes either. Essentially, it’s a challenge to help you write that novel you had always meant to write but keep putting off.

By registering with NaNoWriMo, you are joining a world-wide community of aspiring writers who are all seeking to achieve the same end, and are thus able to encourage and support one another.

Although there are no prizes for completing a novel for NaNoWriMo, if you do (and you have to prove it by uploading your work to the NaNoWriMo site), you will be able to download an official ‘Winner’ web badge and a PDF Winner’s Certificate, which you can print out.

And, of course, you will have the first draft of a novel you will be able to polish and submit for possible publication (or publish yourself). According to the NaNoWriMo website, hundreds of NaNoWriMo novels have been published. They include Sara Gruen’s Wa2ter for Elephants, Erin Morgenstern’s The Night Circus, Hugh Howey’s Wool, Rainbow Rowell’s Fangirl, Jason Hough’s The Darwin Elevator, and Marissa Meyer’s Cinder.

There are lots of useful resources on the NaNoWriMo website and blog, including wordcount widgets, web badges, flyers for downloading, motivational articles, and much more. There is also a busy forum where you can compare notes and get support and encouragement from other participants.

NaNoWriMo 2021 is obviously taking place in the shadow of Covid, with many of us still living under restrictions and life still some way from normal. Nobody knows what this winter will bring, but one thing that’s undeniable is that it could offer an ideal opportunity to write that novel you may have long thought about. My old friend Trevor Belshaw wrote his historical family saga Unspoken (see image below) during the first national lockdown in 2020 and it is now riding high on the Amazon sales charts. There is no reason you couldn’t do likewise!

I wish you the very best of luck if you do decide to register for NaNoWriMo. Please do let me know if you succeed in completing the challenge 🙂

This is an updated version of my original NaNowriMo blog post.

If you enjoyed this post, please link to it on your own blog or social media:

As regular readers will know, I recently started posting monthly updates about my investments. These (partly) replace the ‘Coronavirus Crisis Updates’ I was posting from March 2020. You can read my September 2021 Investments Update here if you like

I’ll begin as usual with my Nutmeg Stocks and Shares ISA, as I know many of you like to hear what is happening with this.

As the screenshot below shows, my main portfolio is currently valued at £21,046. Last month it stood at £21,690, so that is a fall of £644. That is obviously disappointing, but as the value rose by £675 the previous month, I am not going to lose any sleep over it. Most equity-based investments had a rocky ride in September, with my BestInvest SIPP also taking a hit. Stock market investments in general should be regarded as medium- to long-term, and you have to expect some ups and downs in the short term.

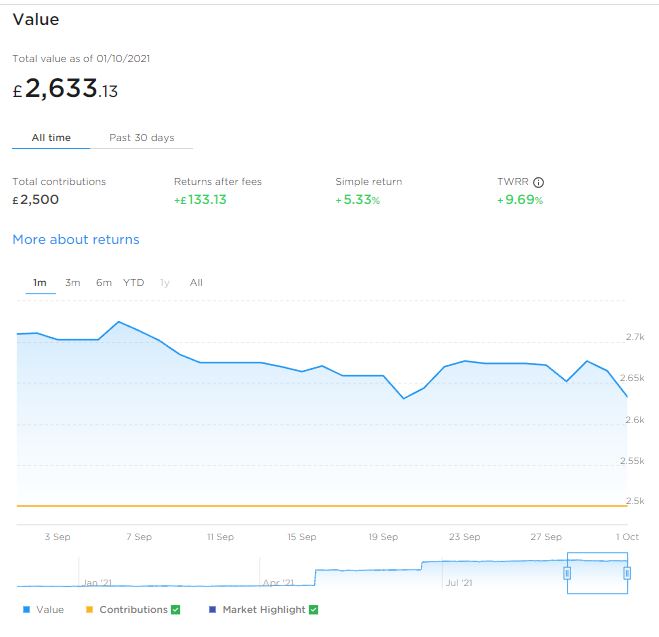

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s new Smart Alpha option. This pot also fell in value in September. It is now worth £2,633 compared with £2,710 last month. That’s a fall of £77, though again the value is still higher than it was two months ago. Here is a screen capture showing performance in September 2021.

As I said above, September was a disappointing month for stock market investors generally, and Nutmeg is far from alone in seeing falls. I make no claim to being an expert on the markets, but from what I read this has resulted from various developments that have worried investors, including the withdrawal of fiscal stimulus packages as we come out of the pandemic and a rise in the inflation rate.

The drop in September is still nothing like what happened in March 2020 – at the start of the pandemic – when the value of my Nutmeg portfolio fell by a third in just a few weeks. On that (admittedly worrying) occasion, the value of my investments swiftly bounced back and turned into a good overall profit for the year. I remain optimistic that something similar will happen again as the UK and world economies get back on a more even keel.

So, especially if you are a new investor, I would strongly advise you not to panic. Remember that if you sell up you are simply crystallizing any losses rather than giving the markets a chance to recover. Personally I am considering investing more in my Nutmeg account now while valuations are down. Obviously I am not offering that as financial advice, just sharing my own thoughts and plans at this time.

Anyway, you can read my full Nutmeg review here (including a special offer at the end for PAS readers). If you are still looking for a home for your 2021/22 ISA allowance, based on my experience they are certainly worth considering. If you haven’t yet seen it, check out also my recent blog post in which I looked at the performance of Nutmeg fully managed portfolios at every risk level from 1 to 10 (my main port is level 9). I was actually pretty amazed by the difference the risk level you choose makes.

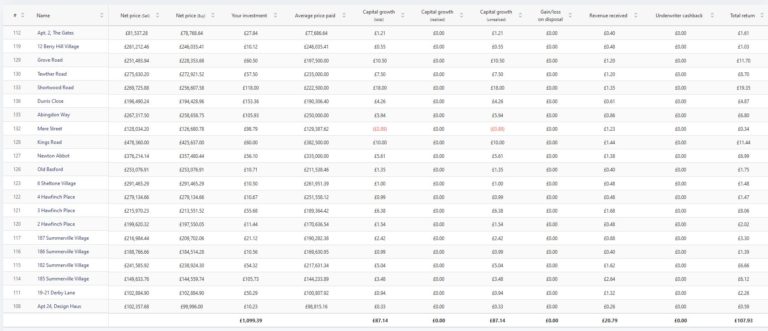

As regular readers will know, this year I am using Assetz Exchange for my IFISA. This is a P2P property investment platform that focuses on lower-risk properties (e.g. sheltered housing on long leases). I put £100 into this in mid-February and another £400 in April. Touch wood, everything has been going well, so in June I added another £500, bringing my total investment on the platform up to £1,000.

Since I opened my account, my portfolio has generated £20.79 in revenue from rental and £87.14 in capital growth, for a total return of £107.93. Here is my current statement:

As I have noted before, Assetz Exchange has had a big influx of new members, meaning all available investments were quickly snapped up. At the same time, some of the new projects that were due to launch were delayed. Only a small number of new projects went live on the platform in the last month, so I haven’t added any more to my portfolio.

To control risk with all my property crowdfunding investments nowadays, I am investing relatively modest amounts in individual projects. I don’t therefore put more than around £100 into any one project. As you can see, I have a well-diversified portfolio with Assetz Exchange comprising 21 different projects. This is a particular attraction of AE in my view. You can actually invest from as little as 80p per property if you really want to proceed cautiously.

Another property platform I have some investments with is Kuflink. They appear to have been doing well recently, with new projects launching almost every day. I currently have just over £2,000 invested with them, quite a large proportion of which comes from reinvested profits. To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, where this happens additional interest is paid for the period in question.

My loans with Kuflink pay annual interest rates of 6 to 7.5 percent. As mentioned above, these days I invest no more than around £100 per loan (and often less). That is not because of any issues with Kuflink but more to do with losses of larger amounts on other P2P property platforms (such as this one). My days of putting four-figure sums into any single property investment are behind me now!

Nowadays I mainly opt to reinvest the monthly repayments I receive from Kuflink, which has the effect of boosting the percentage rate of return on the projects in question

You can read my full Kuflink review here. They offer a variety of investment options, including a tax-free IFISA paying up to 7% interest per year with built-in automatic diversification. Alternatively you can now build your own IFISA, with most loans on the platform being IFISA-eligible.

I’d also particularly draw your attention to their revised and more generous cashback offer for new investors. They are now paying cashback on new investments from as little as £500 (it used to be £1,000). And if you are looking to invest larger amounts, you can earn up to a maximum of £4,000 in cashback. That is one of the best cashback offers I have seen anywhere (though admittedly you will need to invest £100,000 or more to receive that!).

Moving on, I have another article on the always-excellent Mouthy Money website. This was for their Meet the Blogger feature. They asked me a number of thought-provoking questions, including what personal finance tip I would give a younger version of myself and what I would do if I was made Chancellor for the day! You can read my answers here.

Finally, it’s not investment-related, but I did just want to mention an act of kindness that saved me several hundred pounds last month, and a lot of anxiety too 🙂

I drove up to Yorkshire for a family reunion with my sisters Liz and Annie (and Liz’s family, who live there). I went just before the fuel crisis broke, and found myself marooned when all the local petrol stations closed after running out of fuel.

I was staying at Hewenden MIll Cottages near Bingley (the cover image shows the bungalow I booked this time). When I explained my predicament to the owners, they immediately said I could stay as long as I liked free of charge until the situation improved. I don’t mind admitting I was almost reduced to tears by the unexpected kindness. I ended up staying for three extra days – double the length of time I originally booked (and paid for).

So I wanted to take this opportunity to publicly thank Janet and Susan and family for their kindness, and give Hewenden Mill Cottages another plug. As some of you may remember, I last went there two years ago and was bowled over by the quality of the accommodation and the stunning location (see sample photo below).

Today I have a sponsored guest post for you on behalf of Fife Autocentre. The post sets out four advantages to using a mobile tyre-fitting service for tyre replacements and repairs.

Taking good care of your tyres is crucial to maintaining your car’s longevity and performance while keeping you safe. The best way to do this is to engage mobile tyre-fitters to get your tyres repaired, fixed or fitted.

Cost-effective

Why waste time and money trying to get to a garage for tyre replacements and repairs? Mobile tyre-fitting provides an ideal, cost-effective solution. An expert fitter will attend at your preferred location and provide a professional service when conducting repairs and replacements. You will therefore avoid the expense (and risk) involved if you do the job incorrectly yourself. For mobile tyre-fitting, check with the experts at Fife Autocentre.

Increased safety

Why risk damaging your tyres even more when you can be served by a mobile tyre-fitting service at your home or workplace? Attempting to take your car to a garage on damaged tyres is extremely dangerous, as you may end up broken down in the middle of nowhere or even having an accident. A mobile tyre fitting service will immediately respond and act accordingly.

Supremely convenient

Why stress to get tyre problems fixed if you can be reached and attended to at your convenience? Mobile tyre fitters will serve you without disrupting your day’s activities. Just call for help, then carry on with your day as normal.

Instant emergency service

Getting stranded due to tyre problems is a driver’s worst nightmare. So reaching out to a mobile tyre-fitting service is the best solution. Simply contact them and they’ll send someone directly to your location to offer the most effective solution wherever you may be. By this means you can avoid unnecessary delays and be back on the road again in the least time possible.

Final Thoughts

Mobile tyre fitting is the modern way to approach your tyre problems as it is affordable, swift and effective.

I’d just like to add my own endorsement to the advice above. Early on in the first lockdown my car had a puncture and I made the mistake of driving to a tyre and exhaust fitting centre to have it repaired.

Even though I reinflated the tyre before departing, it quickly went flat again. By the time I got to the centre the tyre was flat as a pancake and the wheel had gone out of shape as a result. Instead of paying a small fee for a puncture repair, I therefore had to shell out for a new tyre. So I am very much on board with the advice to use a mobile tyre-fitting service in this situation!

As always, if you have any comments and/or questions about this post, please do leave them below.

Disclosure: This is a sponsored post for which I am receiving a fee.

If you enjoyed this post, please link to it on your own blog or social media:

Nobody would pretend life insurance is an exciting subject, but in these uncertain times it’s something we all need to think about at least. So in this post I thought I’d set out the basics regarding life insurance and why you might need it.

What Is Life Insurance?

Life insurance is a type of insurance policy that protects your loved ones financially if you die. It can help minimize the financial impact that your death could have on your family and provide peace of mind for you and them.

Most life insurance policies are designed to pay a cash sum to your loved ones if you die while covered by the policy. This can help them cope with everyday money worries such as mortgage payments, household bills and childcare costs. It may also cover funeral costs. You can take out life insurance under joint or single names, and you can pay your premiums monthly or annually.

There are two main types of life insurance: term life insurance and whole of life insurance.

Term life insurance policies run for a fixed period such as 10, 20 or 25 years. These types of policy only pay out if you die during the term of the policy. A whole-of-life insurance policy, on the other hand, pays out no matter when you die (as long as you keep up with your premium payments, of course).

There are three different types of term life insurance. With decreasing term insurance, the amount payable on death reduces over time. This type of policy is often taken out in conjunction with a mortgage as the payout reduces over time in line with the amount needed to clear the outstanding debt.

You can also get increasing term insurance, where the payout rises each year (typically to take account of inflation) and level term insurance, where it remains the same throughout. Not surprisingly, level term and (especially) increasing term policies are more expensive than decreasing term.

Over 50s Life Insurance

This type of whole-of-life insurance may be of particular interest to Pounds and Sense readers (PAS is particularly targeted at over 50s).

It allows you to leave a guaranteed fixed lump sum to your loved ones when you’re no longer around. To apply, you need to be aged 50 to 80 (85 in some cases) and a UK resident. No medical is normally required, and your monthly premium (which can be as low as £7) won’t change for as long as you live. In most cases cover for accidental death applies immediately, but for death from other causes there may be a waiting period (typically a year). This type of insurance is not normally index-linked, so over time the value of the lump sum payable may be eroded by inflation.

Who Needs Life Insurance?

Life insurance is intended to protect your dependants from getting into financial difficulties if you die. So if you’re single with no dependants and/or on a very low income, it may not be necessary or appropriate for you.

But if you have a partner, children or other relatives who depend on your income, you probably should have life insurance to help provide for them in the event of your death. Many people take out life insurance when they get married or start a family, or when taking on a major financial commitment such as a mortgage.

Most financial experts recommend you take out life insurance before you reach 35, as the sooner you get cover, the cheaper your premium.

What Doesn’t Life Insurance Cover?

Life insurance normally pays out only on death. If you become unable to work due to an accident or illness, you won’t generally be covered.

Some life insurance policies will pay out if you receive a terminal diagnosis. This is by no means always the case, though, so it’s important to check the wording of your policy carefully.

Most life insurance policies also have some exclusions, e.g. they might not pay out if you die from alcohol or drug abuse. In addition, if you take part in risky sports, you may have to pay a higher premium. If you have a serious health problem when you take out a policy, any cause of death related to that illness may be excluded.

For the above reasons, you may also want to consider taking out critical illness cover. This covers you if you get one of the medical conditions or injuries specified in the policy. Some examples of critical illnesses that might be covered include heart attack, stroke, cancer, and chronic, life-limiting conditions such as multiple sclerosis and MND. Most policies will also consider permanent disabilities as a result of injury or illness. These policies only pay out once and then the policy ends. Some policies will make a smaller payment for less severe conditions, or if one of your children contracts one of the specified conditions. Health conditions you knew you had before you took out the insurance won’t generally be covered.

What Does It Cost?

Life insurance can be surprisingly good value. Premiums start at just a few pounds a month. Prices vary a lot, however, so it’s important to shop around and take advice as appropriate.

A variety of factors may affect the price you are quoted. They include the following:

your age

your health

your weight

your occupation

your lifestyle

whether you smoke

your medical history

your family’s medical history

the length of the policy

the amount of money you want to cover

whether you want decreasing, level or increasing term cover

As mentioned above – and other things being equal – the younger you are, the cheaper your policy is likely to be. But as the list above indicates, many other factors can affect the price you are quoted. In addition, women are typically charged a little less than men, as on average they live a few years longer.

The Get Life Cover Option

As you can see, while life insurance is a simple concept, in practice there are many variations. It’s therefore important to establish what is the most appropriate choice for you and your family, and shop around to get the best price for this.

A company that can help with both these things is Get Life Cover. They will put you in touch with an independent financial adviser in your local area, not some anonymous call centre. The adviser will take the time to establish your exact requirements and recommend a bespoke policy tailored to your (and your family’s) needs. They will be able to arrange all types of life insurance, critical illness cover, cover for long-term illness or disability, and so on. Being independent they will also be able to select from the whole of the market. They are not tied to one insurance company, ensuring you get the best possible value for money.

If you wish, Get Life Cover’s independent advisers can also assist you with other financial matters, including investments, pensions, mortgages, tax, and so on.

To get an initial personalized quote, click through to the Get Life Cover website and provide a few basic details to get a quick quote in 30 seconds, without obligation. You can then discuss this with a local adviser to ensure you get exactly the right type and level of cover for your needs.

As always, if you have any comments or questions on this post, please do leave them below.

Disclosure: This is a sponsored post on behalf of Get Life Cover. If you click through one of the links and end up making a purchase, i will receive a commission for introducing you. This will not affect in any way the product or service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

Summer is here, so it’s high time for another exciting giveaway on Pounds and Sense 🙂

I have joined forces with some of my fellow UK money bloggers to bring you the chance of winning a fantastic Virgin Experience Days Scarlet Collection voucher, worth £100. You can use this voucher on any of a huge range of experiences: from an introductory microlight flight to dinner for two at Coombe Abbey; a pamper day with cream tea for two at a Hallmark Hotel to a three-hour oriental cookery class at School of Wok.

After the last eighteen months we all need and deserve a treat, so here’s your chance to grab one for free!

This giveaway has been organized by my colleague Dan from The Financial Wilderness blog, so I should like to thank him very much for this. More details provided by Dan himself, along with instructions on how to enter, can be found below…

The Prize

The wonderful prize on offer today is a voucher allowing a choice of experience from the Virgin Experience Days Scarlet Collection.

This voucher worth £100 gives you the opportunity to choose a variety of exciting experiences, with something for just about everyone. To give you a flavour of the options on offer in the Scarlet Collection:

For the adventurous – A rally or Porsche driving thrill experience

For the foodies – A range of afternoon teas and dinner options

For the sporty – Have a round of golf at some great courses or learn archery

For the relaxed – A collection of overnight breaks around the country

You can view details of all the available experiences with the Virgin Scarlet Collection on the Virgin Experience Days website here.

The Bloggers Taking Part

This giveaway in run in conjunction with some of my fellow UK Money Bloggers – we run these events to help each other out, so please do visit at least some of the excellent blogs concerned 🙂

Enter to Win a Virgin Experience Days Scarlet Collection Voucher!

Use the Rafflecopter Widget below to make your entry. You’ll need to fill out your basic details and click ‘claim 1 entry’ to be in for the competition.

You also have the opportunity to claim bonus entries by performing an action relevant to the above websites, such as following an account on Twitter or visiting an article. You can do as many or as few of these as you like.

1. There is one top prize of a voucher for Virgin Experience Days “The Scarlet Collection.”

2. There are no runner up prizes

3. Open to UK residents aged 18 and over, excluding all bloggers involved with running the giveaway

4. Closing date for entries is midnight on 18.09.21

5. The same Rafflecopter widget appears on all the blogs involved, but you only need to enter on one blog

6. Entrants must log in to the Rafflecopter widget, and complete one or more of the tasks – each completed task earns one entry in the prize draw

7. Tweeting about the giveaway via the Rafflecopter widget will earn five bonus entries into the prize draw.

8. 1 winner will be chosen at random.

9. The winner will be informed by email within 7 days of the closing date and will need to respond within 28 days with their delivery address, or a replacement winner will be chosen.

10. The winners’ names will be published in the Rafflecopter widget (unless the winner objects to this).

11. The prizes will be dispatched within 14 days of the winner confirming their address.

Just a quickie today to share details of a free-to-enter competition from my friends at All Free Stuff. You can win 1 of 1000 Dior J’adore Absolu samples (see cover image). This is a great women’s floral fragrance by Dior.

To enter, all you have to do is sign up to the Free Stuff email newsletter. This daily email contains all the latest freebies, free samples, competitions, and more (of course, you can unsubscribe any time). Entrants must be over 18 and live in the UK. For the full rules and to enter the competition, please click here.

Good luck, and I hope you win one of the 1000 prizes!

Disclosure: This is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media: