For many of us, our mortgage is our biggest monthly outgoing. So it’s important to keep a close eye on it and check regularly whether you could save money by switching to another provider.

That’s exactly what a new online service called Dashly aims to do. They evaluate your current mortgage deal against the whole market, taking into account your specific personal circumstances as well. If they find a better deal for you they let you know and – if you choose to proceed – assist you with the switching process.

How Does Dashly Work?

Dashly is available as a desktop site, with mobile apps for iOS and Android coming soon.

You start by registering and entering some details about your current mortgage and your personal circumstances. The latter is important, as things such as your income, employment type, credit score and age can all affect the deals you could be eligible for. This process takes 10-15 minutes. Dashly then compares your mortgage against an average of 10,000 products to find the best deal for you.

If they find a better deal than your present one, they send you a notification. You can then evaluate this and decide whether you want to switch. If you do, the team at Dashly will assist you with the switching process.

In addition, Dashly will continue monitoring your mortgage every month. If they find you could save money by switching again, they’ll let you know. It’s worth noting that the equity you have in your property changes on a monthly basis due to ever-changing house values and your decreasing mortgage balance. As your LTV (loan-to-value ratio) decreases, your mortgage may qualify for better, cheaper deals. Again, Dashly checks this on your behalf.

You receive a detailed personal report from Dashly about your mortgage every month. In addition, your dashboard will show you all the key facts at any time, from the changing value of your property to the amount of equity in it, any current deals that would save you money to your next payment date. It’s all there on one easy-to-read web page.

How Much Could You Save?

The savings can be substantial. Dashly say that on average their users save £2,620 (see footnote).

Of course, in practice savings will depend on a number of things, including the balance outstanding on your mortgage, the competitiveness of your current deal, the term left to run, and the effect of any early repayment penalties. Dashly takes all of these things into account in determining whether you could save money by switching to a new lender (and by how much).

Are There Any Costs?

Using Dashly is free. There are no hidden charges and Dashly say they will never hit you with advertisements or email campaigns to try to make money from you. They get paid out of mortgage provider fees, and are authorized and regulated by the Financial Conduct Authority.

Dashly are also founding members of Finance For Good, a charity run by social impact fintechs who put consumers first. They say that their security rivals that of the world’s leading banks.

In Conclusion

If you have a mortgage, in these uncertain times it’s more important than ever to ensure that you aren’t paying over the odds for it.

Dashly offers a free service that not only checks whether you are getting the best deal currently but also continues monitoring your situation month by month and recommends switching again if a new and better deal arises.

By using Dashly you could painlessly save hundreds or even thousands of pounds on the cost of your mortgage. There is never any obligation to switch or any fee to pay for the service. So you really have nothing to lose and everything to gain by registering for an account today.

Footnote: Your individual savings may vary and will depend on personal circumstances. £2,620 per year is the average amount based on research Dashly has conducted on the mortgage market. Find out more at www.dashly.com/reference-index.

Disclosure: This is a sponsored post on behalf of Dashly. If you sign up and make use of the service, I may receive a referral fee for introducing you. This will not affect in any way the service you receive or the deals you are offered.

If you enjoyed this post, please link to it on your own blog or social media:

Regular readers will know that I have been posting about my personal experience of the coronavirus crisis since the original lockdown started (you can read my September update here if you like).

As previously I will discuss what has been happening with my finances and my life generally over the last few weeks, while trying to avoid being too repetitive!

As always, I will start with the money side of things.

Financial

As I’ve done before, I’ll begin with my Nutmeg stocks and shares ISA. This has gone up and down over the last few weeks, but currently stands at £16,578. That is over £500 up on last month, so I’m happy with that! Here is a screen capture covering the last three months…

My Property Partner and Kuflink investments are still both ticking along satisfactorily. Property Partner has resumed paying dividends on some properties, which is appreciated. The five-year sales process has also resumed. There is a backlog, though, so it will probably be longer than five years till the properties I hold shares in can be sold at the current, independently-assessed market price (or retained, of course).

There is nothing really to report about The House Crowd. I assume that the sales of the two properties in which I hold £1,000 shares are progressing, but can understand that it is a slow process at present. At least rental payments are still accruing, which should help to defray some of the selling costs.

There has been no further word either regarding my investments with Crowdlords. As I said last month, I have two remaining investments with them, Kennington Road eco-houses and Trent House. I was told they hope to have exit options for these properties by the end of the year, but I’m not holding my breath. On the plus side, they are paying 6 percent interest on my Trent House investment, which is quite generous in these days of ultra-low interest rates.

Personal

It’s been an eventful few weeks one way and the other.

As mentioned previously, I had booked a short break in Llandudno (see cover image) near the end of September. Thankfully I was able to go. If I had left it just a few days later I would have had to cancel, as the Welsh Assembly has decided to lock down the whole of the Llandudno and Conwy area due to rising infection rates. That means no-one can currently go in or out of the area without a compelling reason (and having a holiday booked there doesn’t count).

Anyway, I enjoyed my visit. I stayed in a self-catering apartment, which turned out to be a good choice in most respects. It was on two floors, with a lounge and well-equipped kitchen on the lower floor and a double bedroom and bathroom on the upper. The location was central but quiet, yet just five months’ walk from the sea. The only drawback was that parking was on the street and finding a spot was a bit of a lottery. I was lucky to get somewhere close when I arrived, but later in the holiday had to park on another road half a mile away, which was a bit of a pain. I paid £255 for my three-night stay via Booking.com, which I thought was reasonable. By comparison, the seafront hotels I checked out were charging over £600 for three nights’ bed and breakfast.

Not surprisingly Llandudno was quieter than usual for the time of year, but there were still plenty of visitors, and many of the small hotels and boarding houses had ‘No Vacancies’ signs in their windows. While some places and amenities were closed, many others were open, and I was pleased to find that the pier was fully operational (see photo below). Professor Codman’s famous Punch and Judy show on the promenade wasn’t running, though – a shame, as there were lots of young children who might have enjoyed it.

On my first day I left my car at the apartment and took a couple of bus tours. The first was the open-top bus that takes a circular route between Llandudno and Conwy and includes a running commentary. I have done this trip before and noticed that the recorded commentary hasn’t changed this year. Mind you, that may be just as well, as a post-Covid commentary would have had to include details about all the hotels and other places that have closed due to the virus, the seafront theatre that became a Covid field hospital, and so forth…

The other trip was on a vintage bus (see photo) around the Great Orme, one of the two promontories at either end of Llandudno’s seafront. This had a knowledgeable driver/guide, who provided an interesting – and up-to date – commentary. I must admit I particularly enjoyed seeing ‘Millionaire’s Row’ at the far side of the Orme. There are some amazing houses here, owned by people who like to preserve their privacy. Obviously the coach passes from a distance, but it was still a good opportunity to gawp at how the super-rich live. I particularly enjoyed hearing about the house that has its own private lift down to the beach!

On the second day of my visit I drove to the medieval walled town of Conwy, which is about three miles away. I booked a ticket online to see Plas Mawr, a restored Elizabethan town house (photo below). It was fascinating, and I was glad I took the option of borrowing one of the free electronic guides. You use these to scan a QR code in each room and it provides a commentary on the room itself and various interesting historical tidbits associated with it.

As with my visit to Dunster Castle near Minehead earlier in September, all the usual anti-virus measures were in place. I had to wear a face covering throughout, and staff ensured that there were no more than two households in a room at any one time. It worked pretty smoothly, although you had to follow a set route and there was no possibility of returning to a room once you had left it.

In case you’re wondering, the photo in my cover image shows the Haulfre Gardens Tearoom on the lower slopes of the Great Orme. It’s one of my favourite places in Llandudno, and I was pleased to find it was still open. I enjoyed afternoon tea in their lovely garden on both days of my visit. As you can see, I was pretty lucky with the weather!

As mentioned above, I was very glad to be able to make my trip before the current lockdown would have made it impossible. I feel very sorry for people who booked after me and were unable to go, especially as I have heard that some are now having problems getting their money back. But I am sorry also for the hotels and other businesses who have been left high and dry by the lockdown. I really hope for their sake it doesn’t go on too long 🙁

Moving on, I had an experience I would rather not have had in the last few weeks too. At a routine eye examination my optician saw something she didn’t like the look of in the retina of my left eye. So she packed me off to the eye clinic at Queens Hospital, Burton. The doctor there told me I had a perforation of the retina, and gave me laser treatment then and there. It wasn’t painful but it was obviously nerve-racking. The doctor did say it was a good thing my optician had spotted the problem, as it could have led to a detached retina if left untreated, which is clearly more serious. I have to go for a follow-up check this weekend, but touch wood the problem has been repaired. I guess if nothing else this does show why it’s so important to have your eyes checked regularly even if you don’t think there is anything wrong with them. That applies doubly to older people and those who (Iike me) are very short-sighted, as we are especially susceptible to this sort of thing.

On the Covid front, clearly most of the news hasn’t been good recently. Mind you, in most parts of the UK hospital admissions and deaths remain a lot lower than at the peak of the pandemic in the spring. I have seen the current situation described as a ‘casedemic’, which seems a pretty apt description. Clearly it’s important to protect the elderly and vulnerable at this time. Young people don’t typically suffer severe reactions to the virus, however, so I do wonder if some of the more extreme measures aimed at them are fair or necessary. Personally I am taking what I consider reasonable precautions but still trying to live my life as normally as possible. I volunteered for the UCL Virus Watch panel a few weeks ago and fill in a weekly questionnaire saying whether I have any possible Covid symptoms (none so far). They have also just asked me to take a blood test to see if I have any antibodies or other natural resistance to the virus. I’ll be interested to see the results of that!

As regards masks and such matters, I have been wearing a half-face shield in supermarkets (as a mask sceptic I’m not going to other shops till masks are voluntary again, though I might make an exception if the shop clearly states that they welcome non-mask-wearers). I find this better than the full face shield I was wearing before, as it doesn’t interfere with my vision. Shields are also much easier to breathe through than cloth masks, and I haven’t yet been challenged by any staff members or self-appointed mask police. In case you are interested, here’s an Amazon ad (affiliate) for some half-face shields similar to the type I am now using.

Well, I guess that’s enough for now. I do hope you and your loved ones are staying safe and well. As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

I recently enjoyed a three-night break in the North Somerset coastal town of Minehead.

It was actually my first visit to Minehead. Early this year, before the pandemic struck, I booked breaks in a few places I hadn’t been to before. Minehead was the only one I didn’t have to cancel 🙁

After some online research, I had booked a room at the Channel House Hotel. This is on Minehead’s North Hill (see cover photo), on the opposite side of the bay from the Butlins holiday camp. Here’s a map by courtesy of Google.

The Channel House Hotel had excellent reviews and a great location near the harbour. It had its own car park as well, which is always a plus with seaside hotels!

Here’s some more information about my stay…

The Hotel

The Channel House Hotel is a small country-house hotel with eight bedrooms. They don’t accommodate dogs or children under the age of 15.

I had Room 7, on the top floor. I had been hoping for a sea view, but due to a line of trees I couldn’t really see it from my room. I could at least hear the waves, though! The hotel is in a quiet, peaceful location, and I slept very well on all three nights.

As you would expect in these strange times, various anti-virus precautions were in place. I had my temperature checked on arrival, and hand sanitizer was available by the front door and on all the tables in the dining room.

I opted for breakfast and an evening meal, although you can book bed and breakfast only. Other dining options near the hotel appear limited, though, especially in these times of Covid.

There was a good choice of breakfast options for a small hotel. As well as the full English (which you can customize as you wish) you could also have Eggs Benedict in three different variations or smoked haddock with poached egg. You could also have a plate of mixed fruit, cereal and/or yogurt, plus the usual toast and hot drinks. I’m not sure what the normal arrangements for breakfast are, but obviously at present they can’t have a self-service buffet, so most meal options are brought to your table.

There is a choice of starters and main meals in the evenings, with guests asked to say what they would like after breakfast. Fair enough in my view, as there is obviously no point in the hotel preparing meals nobody wants! That applies especially at the moment with visitor numbers so low – partly due to the virus and partly (I understand) as a deliberate policy to help preserve social distancing. During my stay, there were never any more than six guests including me.

Evening meals are served at 7.00 pm, with pre-meal drinks in the small bar from 6.30. Although the latter is obviously optional, I did find this an enjoyable way of meeting and getting to know my fellow guests. There was one couple and all the others were solo ladies around my age or older. We all got along well. I enjoyed hearing what they had been doing during the day, as most of them knew the area better than I did.

The evening meals were very good. They comprised five courses: starter, main, dessert, cheese and biscuits, and coffee. That may sound a lot, but the portions were sensibly sized, so I didn’t feel too guilty!

Fish seems to be a speciality and I particularly enjoyed the sole I had on the first night. One thing that surprised me, though, was that the menu never included any vegetarian main courses. They do cater for veggies and those with special diets, so I’m sure if I’d asked I could have had something. For three nights I was perfectly happy with what was on offer. But as I eat vegetarian quite often at home, it might have been nice to have that option on the menu as well, some nights at any rate!

My twin-bedded room was more than adequate for my needs. It had a small (by modern standards) wall-mounted TV, but that was fine for a short visit. The WiFi worked well once I sorted out a bit of confusion over the password, and I was able to use it in my room as well as the communal areas. The bathroom was a good size and had a bath with a modern electric shower over it. My bed was comfortable and there was plenty of storage space. I was well looked after and had an enjoyable and relaxing stay.

Financials

As Pounds and Sense is primarily a money blog, I should say a word about this.

I paid £360 for my three-night stay (including breakfasts and evening meals) at the Channel House Hotel, which I thought very reasonable. If I had chosen bed and breakfast only, the price would have been £285. As you may gather from this, the hotel charge a fixed price of £25 for their five-course evening meals.

You can check current prices and availability on the Hotels.com website. You can book this way (which I did) or directly with the hotel. The latter method may or may not work out cheaper.

Things to See and Do

Inevitably at the time of my visit a lot of places and attractions were either closed or not operating normally.

I was particularly disappointed that the West Somerset Railway – said to be the longest heritage railway in England – was not running. At the time of writing there is still no indication when it will reopen.

I was though able to visit Dunster Castle, which is owned by the National Trust. As a Trust member I was able to get free admission, but had to book a ticket in advance on the website. They are doing this to ensure that visitor numbers are controlled, to help maintain social distancing.

Dunster Castle goes back to at least Norman times, with an impressive medieval gatehouse and ruined tower providing a reminder of its long and sometimes turbulent history. The castle became a lavish country home during the 19th century for the Luttrell family, and the furnishings and decor are largely from that time. The castle is surrounded by a terraced garden displaying varieties of Mediterranean and subtropical plants. Below this is a riverside woodland garden leading to a historic working watermill (unfortunately closed at present).

Due to anti-virus measures, visitors have to follow a long and winding route through the gardens to get to the castle, so my top tip is to allow longer than you would expect to arrive at your allotted time. Bear in mind also that you will be expected to follow a similarly circuitous route afterwards to get back to the car park. This means there is a lot of walking before and after you see the castle itself. I was okay with that, but I suspect some older visitors might struggle.

Anyway I duly arrived at the castle entrance and, after giving a phone number for track-and-trace and using a hand sanitizer, was allowed to enter (wearing a face covering, of course). Only certain parts of the castle were open to visitors, not including the kitchens for some reason. On the plus side, though, with so few visitors there was plenty of room to see everything on view. Although entry is by timed ticket, once in you are allowed to stay for as long as you want (or at least for as long as you can stand wearing a face covering).

I spent around an hour in the castle, after which I was ready for some refreshments. I am not sure if the castle has a coffee shop normally but if so it was closed. They did though have a pop-up cafe in the gardens (you can just see this to the left of my photo above). I had a hot chocolate and a slice of coffee-and-walnut cake here, which I very much enjoyed even though it wasn’t exactly a healthy option!

Dunster Castle was the only formal visitor attraction I visited during my stay, and I do recommend it, so long as walking isn’t a problem for you.

In fact, I did a lot of walking throughout my break. That included along the seafront, from the harbour to the Butlins camp, and also up North Hill, which takes you to the edge of Exmoor. On the walk up North Hill, I stopped to admire the 16th century St Michael’s Church (also sadly closed).

Near the church is an area called Church Steps, where there are some beautiful thatched cottages.

I would like to show you the view across the bay from the top of North Hill, which I am told is quite spectacular. When I got to the viewing area, however, a closed and padlocked gate barred my way, with a forbidding warning notice about Covid-19. Having made the not-inconsiderable effort to walk up the hill (most people drive), this was pretty disappointing. I sat at the roadside for a few minutes collecting my thoughts before heading down again. That was probably the low point of the holiday!

On my last day in Minehead I took a short stroll to Blenheim Gardens, a well-tended and attractive public park. The cafe was closed as well, but I wandered down to the harbour and enjoyed a takeaway cream tea there 🙂

Closing Thoughts

Overall, I enjoyed my visit to Minehead, though obviously the fact that so many places were closed did spoil it a little. I had an enjoyable, relaxing time, with plenty of healthy fresh air and exercise (just as well in view of the cakes and five-course dinners!). I will hope to go back again when things are more normal.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Regular readers will know that I have been posting about my personal experience of the coronavirus crisis since lockdown started (you can read my August update here if you like).

As previously I will discuss what has been happening with my finances and my life generally over the last few weeks. I will try to avoid being too repetitive, as I have obviously published a few of these updates now and not everything changes that much from one update to the next!

As always, I will start with the money side of things.

Financial

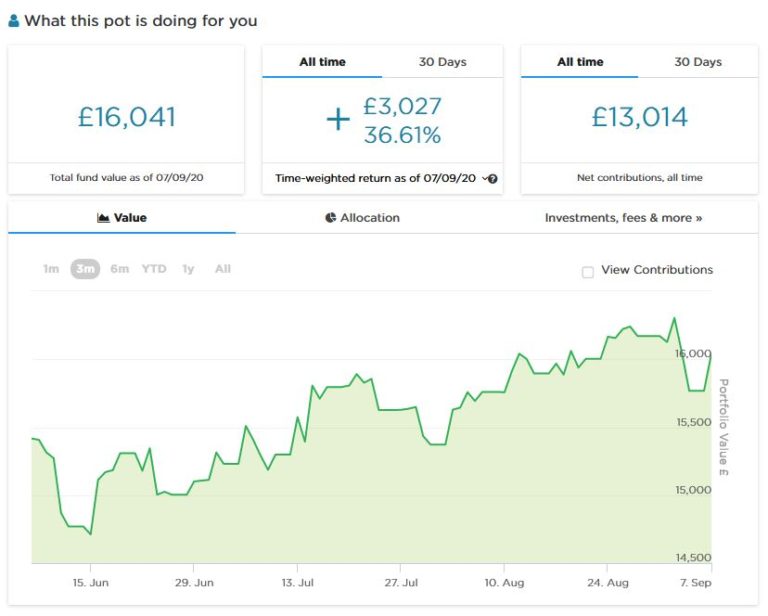

As usual, I’ll start with my Nutmeg stocks and shares ISA. This has gone up and down over the last few weeks, but is currently at £16,041. At one point it was as high as £16,270, but it’s still over £400 up on last month, so I’m not complaining. Here is a screen capture covering the last three months…

My two Buy2LetCars investments are still delivering the promised monthly returns without any hassle. I was pleased that Buy2LetCars also chose to feature me and my blog posts about the company in their email newsletter last month. That brought me a few more readers, so a special welcome if you are one of them! Again, if you’d like to learn more, you can read my review of Buy2LetCars here and my more recent article about the company here.

There is nothing particular to report about my Property Partner or Kuflink investments, both of which are ticking along satisfactorily. As regards The House Crowd, another of their properties in which I hold a share has just been sold, so that is around £2,000 in capital I am expecting back in the next month or two. Unfortunately I am not expecting to make any profit on these two investments, though I have of course received rental payouts – or dividends if you prefer – from these properties over the time I’ve held shares in them.

As regards Crowdlords – which I discussed last month – I wrote asking about two investments I still have with them, Kennington Road eco-houses and Trent House. I had received no information from Crowdlords about either of these projects since before lockdown in March, which I found disappointing.

I received a prompt and courteous reply from Crowdlords co-founder, Richard Bush. He told me that the properties in question were proving difficult to exit from and the situation had been complicated by the change in their FCA status. He added: ‘Prior to the FCA announcement we were about to launch new investments for both of these properties, giving those that wish to leave an exit option and others who like income-based investments to take over, alongside mortgages. This is still our plan, though at the same time we will also try and sell both properties…Once we’re back up and running with Equity and Mezzanine investments we will turn our attention to the BTL’s (including Kennington Road) and still hope to have an exit option available by the end of the year. In the meantime Trent House will continue to earn 6% p.a interest.’

So I guess that is somewhat reassuring, but I’m still not holding my breath about seeing any return from either of these projects any time soon. It’s a shame because I’ve always liked Crowdlords and had good returns from my other investments with them. But obviously these are unprecedented times and property markets generally have been struggling. I will wait to see what new offering the company comes up with, but it will have to be very enticing indeed to persuade me to invest with them again.

As mentioned last time, I applied for the second (and final) round of SEISS (Self Employed Income Support Scheme) payments in mid-August and duly received payment a few days latter. I haven’t seen any complaints or problems about the administration of the SEISS programme and think HMRC deserve a lot of credit for how smoothly it has run. I do know there were issues over eligibility, however, so my commiserations go to any self-employed people who – for no fault of their own – failed to qualify.

In any event, if you are self-employed and eligible for a SEISS payment, applications are open now, so don’t delay!

Personal

In the last few weeks I have done a few things for the first time since lockdown in March. For one, I took advantage of the government’s Eat Out to Help Out scheme to enjoy a couple of pub lunches (okay, one was more of a pub brunch). It was great to be doing something more normal again and catch up with old friends I hadn’t seen since the start of the year. And paying half-price was a nice bonus!

It was obviously a different experience from the usual. When my friend and I arrived for our pub lunch, we were met by a man at the door who checked our booking and showed us to our table (no chance to pick our own as we would normally). One thing I noticed was that no staff were wearing masks and only a few customers. As a mask sceptic this didn’t bother me, but again I was struck by the incongruity of a situation where you can be in a pub surrounded by other diners for a couple of hours with almost nobody masked, then go to a supermarket and be forced to put one on while there (unless you’re exempt, of course).

In any event, I really enjoyed my pub lunch and catching up with my friend. We couldn’t pay cash as we would normally – nobody wants cash nowadays in case it’s contaminated – so my friend paid on his card and I later forwarded my half to him via PayPal. That was a first!

I also went to Birmingham to meet another old friend for brunch at one of the Wetherspoons pubs there. It felt odd to be on the streets in Brum and see so many people wearing masks in the open. Nobody does this in the small town where I live, but I guess it’s a bit different in big cities. Anyway, my friend arrived before me and was directed to a table at the back of the pub. I then had to wander around the tables looking for him behind various protective screens, feeling like a voyeur or a spy. But thankfully I found him eventually!

The instructions on the table told us to order via the Wetherspoons app. That task fell to me, as my friend doesn’t have a smartphone. I managed to do it after signing in to the pub’s free WiFi. I saw several people struggling with this, though. They either ended up hailing a passing waitress or gave up and ordered at the bar.

Anyway, the app worked well for me, and I was impressed by the speed with which cutlery was brought to our table, shortly followed by our meals (two all-day breakfasts). We both also ordered coffee with limitless refills. I was pleased to discover that this was still on offer, though you are now supposed to ask a staff member for a new mug before going to the coffee machine again. I did this, but I don’t think anyone else did.

I have just returned form a short break in Minehead on the Somerset coast (my cover image shows the harbour with the Butlins camp in the background!). I won’t say too much about this here as I plan to do a separate post about it soon. But I will say it was an enjoyable and relaxing break, only slightly marred by the fact that many of the attractions were closed due to Covid. I did manage to visit the nearby Dunster Castle (pictured below), which is owned by the National Trust. Sadly only some areas were open to the public, with various restrictions due to the virus. But on the plus side, because visitor numbers were being limited, I had plenty of space to appreciate what was actually on view!

Going back to masks and such matters, I have been wearing a full face shield in supermarkets (I’m not going to other shops till masks are voluntary again, though I might make an exception if the shop clearly states that they welcome non-mask-wearers). I find this a good compromise as it is much easier to breathe through than a cloth mask, and I haven’t yet been challenged by any staff members or self-appointed mask police. I also recently obtained a half-face shield which covers you from the nose downward. That makes it more portable, and also means your vision isn’t impaired (shields are made of clear plastic, but with my eyesight I struggle a bit reading lists of ingredients through them). In case you are interested, here’s an Amazon ad (affiliate) for some half-face shields similar to the type I bought.

I am looking forward to another late summer break in a couple of weeks’ time. I shall be going to Llandudno in North Wales, one of my favourite UK holiday destinations. I shall be staying in a self-catering apartment and am looking forward to shopping for food without having to put a mask on (Wales so far having sensibly resisted the pressure to make masks mandatory in shops). More about that next time!

And that’s it really. Recent reports are indicating an uptick in the virus among young people especially, and of course the doom-mongers are out in force again. Nonetheless, I think there are still plenty of reasons to stay positive. Hospital admissions and deaths are thankfully still at very low levels. And in my personal opinion we are very unlikely to see a ‘second wave’ anywhere near as bad as the first. Of course, it’s important to continue taking sensible precautions such as hand-washing and using sanitizing gel, along with social distancing (if you can keep up with the ever-changing rules). Personally I think that any marginal benefits from wearing masks are more than offset by the way people misuse them in practice. But I’d better not go on any more about that!

I hope you and your loved ones are staying safe and sane during this crazy time. As ever, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m talking about the important subject of home security.

Obviously it’s not something anyone likes to think about, but the risk of being burgled is very real. It is estimated that a burglary is committed every 40 seconds in the UK (it’s impossible to give exact figures as many such crimes aren’t reported). That means in the time it takes you to read this article, four homes are likely to have been burgled.

Of course, there are certain precautions you can take to reduce the chances of becoming a victim yourself. These include:

Keep all windows and doors locked even when you’re at home.

Keep garages and sheds locked as well, especially if they contain tools or other items that might be useful to a burglar.

Try to vary your daily routine so that burglars (who often live nearby) don’t notice and take advantage.

Avoid mentioning holiday plans too widely (especially not on Facebook or other social media).

Install timers on lights so they go on and off in a seemingly random way while you are out.

Install security lighting that will detect visitors (invited or uninvited) and illuminate them.

These and similar measures can reduce the likelihood of a burglar targeting your property. But of course, they are unlikely to be sufficient alone. You need a burglar alarm, and ideally a complete home security system. Like this one, perhaps…

Boundary Smart Security

If you’re reading this blog, chances are you have a burglar alarm already. But especially if it was fitted a few years ago, it may not be as effective as you hope.

Older alarm systems are easily defeated by determined, professional burglars. And especially if you live in a nice house and have an expensive car or other signs of wealth, you could well be targeted by such individuals. You need a modern smart security system to provide both maximum protection from burglars and the peace of mind that comes from this.

Boundary aims to provide UK residents with state-of-the-art home security at an affordable price. Their new high-tech Boundary Alarm system is based around a central hub (see cover image, above) that wirelessly connects to each Boundary device in your home and allows you to control them from anywhere using a single smartphone app. It’s a sophisticated system that can still be installed by anyone and set up easily (though optionally you can pay for professional installation if you prefer).

You can customize your alarm system as you wish with door and window sensors that detect exactly when any door or window opens in your home and set off an alarm. You can also incorporate infra-red motion detectors (wireless and pet-safe) that will detect any human movement when you’re not at home. Other features include a key tag to easily arm and disarm the system when you’re coming and going, and a 95-decibel siren (pictured below) to alert your neighbours if your home is broken into.

Plans

Boundary offer four different plans, with no long term contracts, cancellation fees or hidden costs. Full details can be viewed on the Boundary website, but briefly they are as follows…

Lite – This is the lowest cost option, with no ongoing fees. It covers two users, two sensors, the Boundary app, smart home integration and Boundary Neighbourhoods (once this service is launched). The latter is a ‘neighbourhood watch’ dashboard to allow people in local areas to connect online to share details of crime and suspicious activity. You will have the option to link your Boundary alarm so that if it goes off, your neighbours will automatically be notified.

Starter – This includes all the features above and others, including push notifications when the alarm goes off, alarm-set reminders when you leave the property, occupied home simulation (requiring smart light bulbs), and so on. This plan costs £4 a month.

Plus – This includes all the features above plus an extended three-year warranty, automated keyholder calling, partial setting (e.g. downstairs only), and more. This costs £8 a month.

Complete – This also includes police response. When the alarm goes off, a security guard at an alarm receiving centre (ARC) will be automatically notified and will immediately verify whether your home is being burgled. If confirmed, the security guard will request a police response and notify the property owner and/or nominated key holders. The complete plan also includes an annual maintenance visit by an engineer. The cost of this plan is £25 a month. Note that with this plan professional installation is mandatory.

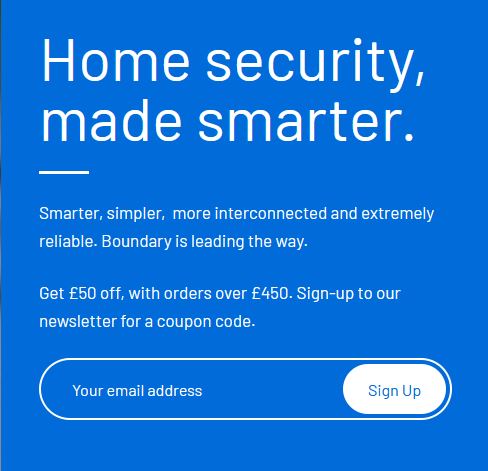

Boundary is still in pre-launch phase and right now you can get a voucher for £50 off the price of any system costing £450 or more just by signing up to their newsletter using the form on their website (screen capture below). There is of course no obligation to use this – but if you’re at all interested, I recommend signing up now to get your hands on the £50 discount code.

Self-install alarm systems are due to be sent out by the end of August, while for those who choose professional installation, the company say that currently they expect delivery and installation to take place in October.

You can ask for a no-obligation quotation via the website to get a price for a system tailored to your exact needs, with no nasty surprises further down the line. At the very least, if you think Boundary Alarm could be the answer to your home security needs, do sign up now for their email newsletter and £50 off voucher.

Note: This is a fully updated repost of my original article from April 2020.

Disclosure: This post includes my referral link, so if you click through and make a purchase, I may receive a commission for introducing you. This will not affect the price you pay or the service you receive.

If you enjoyed this post, please link to it on your own blog or social media:

Hiro is a brand new new mobile phone app currently offering a range of incentives just for downloading it and answering a few quick questions about the smart tech you have in your home.

Hiro say that in future they plan to offer members personalized discounts on home insurance and similar products based on their home technology – from Amazon Alexa devices to smart thermostats, doorbell cameras to smart locks.

Right now, though, there is nothing to buy. They are simply looking to build a community of people who may be interested in saving money on insurance in future. And to do this they are offering gifts for downloading the app and signing up. These range from £5 Amazon gift vouchers to £5/£10 Hiro credits, and lots of other weird and wonderful things as well. Here’s how it works…

Grab Your Free Prize

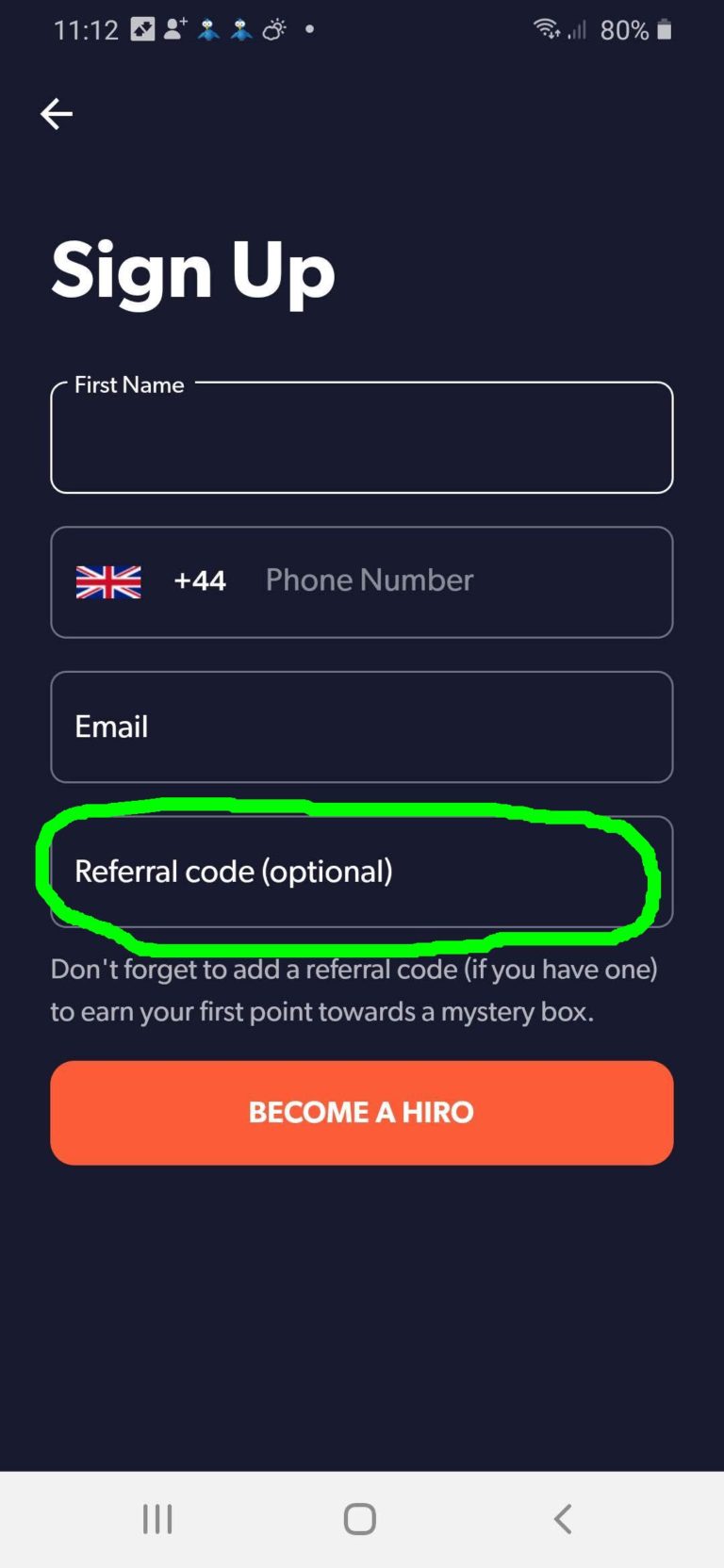

Start by downloading the Hiro app from Google Play or the Apple Store. Open the app and here is what you should see…

Enter your first name, (mobile) phone number and email address in the appropriate boxes. Where it says ‘Referral code’ (highlighted above) please enter nic637, then tap on ‘Become a Hiro’.

You will then be presented with a short questionnaire about your use of smart tech in the home. When I did this, the app told me that with my modest complement I would be eligible for a 17% discount on my home insurance. That’s nice to know, though of course it won’t mean much until Hiro start selling actual insurance.

They say as well that even if you don’t currently have any smart technology, they will be making recommendations and special offers, and explaining the extra discounts the tech in question can bring you.

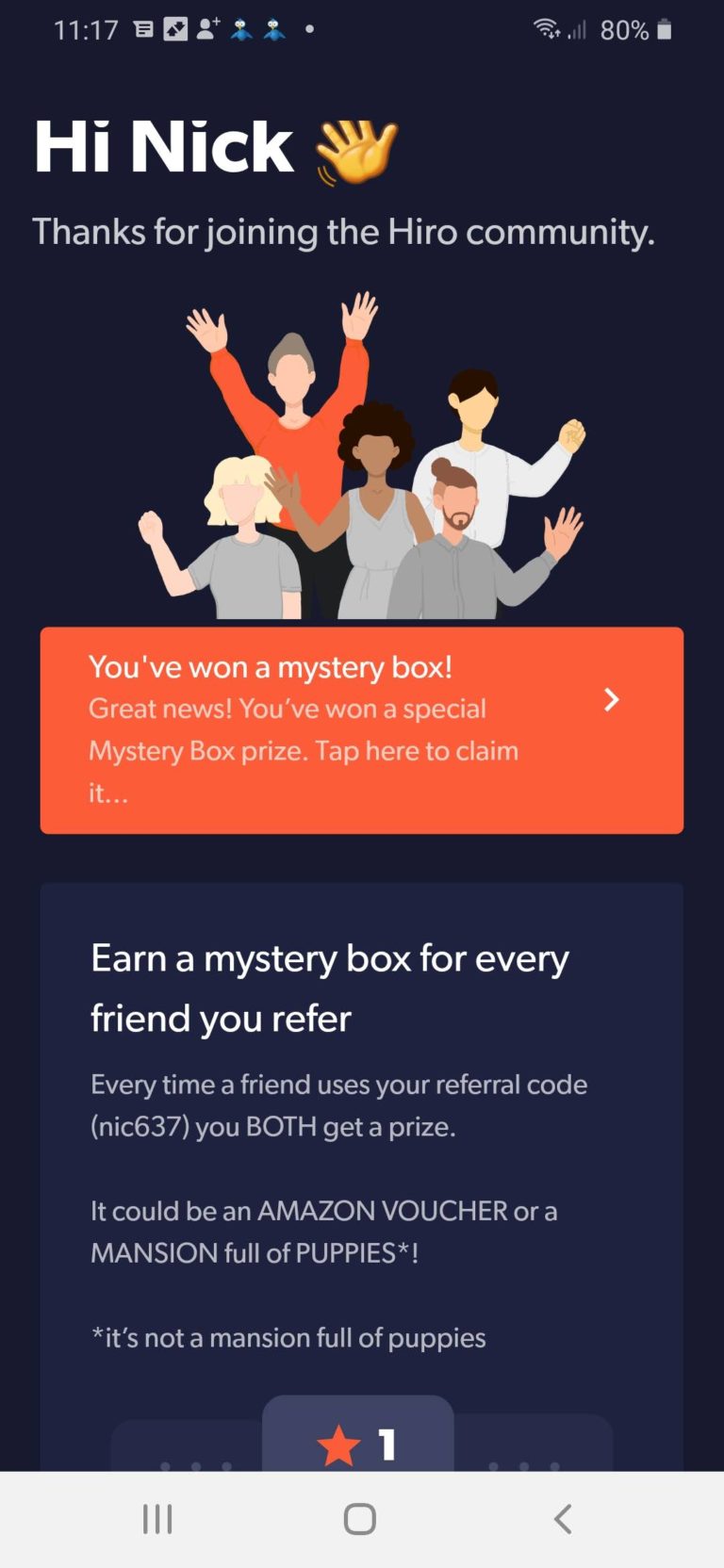

In addition, once you’ve answered the questions, we will BOTH be eligible for a prize (or mystery box, as they call it). Here’s the screen you should see…

Just tap on the the orange box (see screen capture above) to see what you have won.

Of course, once you have signed up you will get a personalized link as well and be able to share this with friends and family. Any time someone signs up using your link, both of you will win a prize. As I said above, there is nothing to buy now and no obligation in future.

Good luck, and I hope you win something almost as exciting as a mansion full of puppies 🤣🤣🤣

As always, if you have any comments or questions about this post, please do leave them below..

Update 19th May 2020 – I have just heard that Hiro aren’t offering Amazon vouchers as prizes at the moment. Other prizes such as Hiro credits are still on offer.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m spotlighting another survey site that offers the opportunity to generate a sideline income.

You may well have heard of YouGov already, as they often run opinion polls on political preferences and other current issues.

YouGov are always on the lookout for new people to join their panel and complete surveys via their website. Naturally, they provide financial incentives for doing this.

How Does It Work?

For each survey you complete on YouGov, you are allotted points. For a typical survey taking 10 to 15 minutes you will get 50 points. Of course, the longer the survey, the more points you will receive.

You can complete surveys on a computer, smartphone or tablet. You will be notified by email of new surveys you are eligible for, though it’s also worth logging on regularly to see the full range of surveys currently available.

Once you have accumulated 5000 points you can redeem them for a £50 fee. YouGov refer to this as a ‘cheque’, but the money is actually paid direct to your bank account.

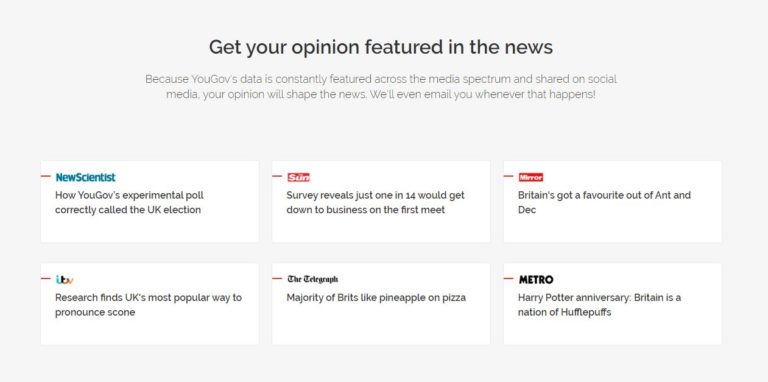

To get 5000 points you would need to complete 100 fifty-point surveys, so this is clearly not a get-rich-quick opportunity. Nonetheless, the surveys are generally interesting and not too demanding to complete. And you will also have the satisfaction of knowing that your responses will ultimately influence decision-makers in government and the private sector. You can see some example media coverage of YouGov surveys in the screen capture from the website below.

How Do You Join?

Joining the YouGov panel is very simple. Just click on this referral link (see below) and complete the short online application form. Acceptance is normally automatic, and you can start earning points immediately.

Disclosure: if you join YouGov via my link I will get 200 points credited to my account (worth £2). If you join YouGov you can also refer other people and earn extra points as well. It all helps get you closer to that next £50 payment!

As always, if you have any comments or questions, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

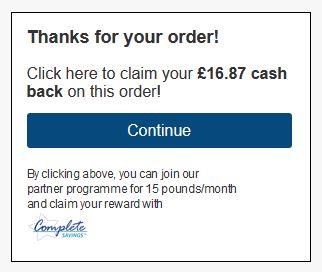

I had a phone call last week from an elderly friend wanting advice. She had just bought some medical supplies on eBay and an ad had come up offering her money back plus a cash bonus. She was keen to know whether this was genuine or not.

Unfortunately I had to tell her that it wasn’t as good an offer as it appeared. This ad – which I have seen many times myself – appears when you have made a purchase at any of a range of online stores, including eBay. Here’s what it looks like…

As you may be able to see from the (tiny) logo at the bottom, this ad comes from a company called Complete Savings. They describe themselves as a cashback site, but as the smaller message below the eye-catching headline reveals, they charge your credit or debit card £15 a month for membership until you cancel.

So Is This a Scam?

I would hesitate to describe Complete Savings as a scam, but the fact remains that – as this Which? article from 2018 confirms – a lot of people are being caught out by it. If you’re in a hurry, it’s easy just to see the eye-catching headline and click straight through to the application form. One lady mentioned in the Which? article didn’t notice she was being charged for five months and ended up £90 out of pocket.

Or you might be like my elderly friend. Her eyesight is poor and she can’t easily read the small print in ads, especially on her mobile phone. She is also relatively new to online shopping (while having to do much more as she is self-isolating). It isn’t hard to see how people such as her could be inadvertently drawn in.

I should make clear that you aren’t automatically signed up just by clicking on the ad. An online application form will appear, and this will hopefully alert you to the fact that you are registering for a subscription-based service. But if you’re in a hurry, or confused, or misunderstand what’s on offer, you could complete the form without realising what exactly you’re signing up for. According to the Which? article mentioned above, they receive a steady stream of complaints from people who have done exactly this.

So Is It Worth Joining?

For your £15 a month, Complete Savings offer discounts from a range of online retailers, including Superdrug, Wickes, B&Q, Hermes, and eBay. Judging from the Complete Savings homepage the standard discount seems to be 10%, although the website says this is the minimum.

To get discounts, you first have to go to the Complete Savings site and click through to the merchant concerned from there. The merchants pay commission to Complete Savings for people buying via their link. All being well, a share of this will be credited to your account as cashback in due course. You can then withdraw this to your bank account once you have earned at least £5.

If you shop online a lot, the cashback could potentially cover the £15 a month fee and be worth your while overall. If you just buy the odd thing online that’s unlikely to be the case, though.

My Thoughts

In my view there are many better ways to get discounts/cashback than Complete Savings (or its sister site Shopper Rewards & Discounts)

As mentioned in this blog post, popular cashback sites such as Quidco and Top Cashback are free to join and offer cashback from a huge range of merchants – in many cases at better rates than Complete Savings. I recommend signing up with all three, and also checking out Cashback Angel, which lets you compare which free cashback platform is offering the best deal for any particular merchant.

Overall, then, my advice is to be very wary of this offer and don’t click on the ads unless you really want to pay £15 a month for a cashback programme when better, free ones are available. And if you know any elderly people or people new to online shopping who may be tempted, warn them it’s not as great a deal as may at first appear. Do them a favour and recommend they sign up with a free cashback site instead!

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media:

Today I’m spotlighting a pension advisory service called AdviceBridge that may be of interest to any Pounds and Sense readers who are planning for their retirement.

There is no doubt that in recent years retirement planning has become more challenging. The pension reforms introduced by George Osborne in 2015 gave people much more freedom over how and when they can access their retirement savings. There are many benefits to those reforms – and I’m a fan of them myself – but it does mean most people now have big decisions to make over how to finance their retirement.

A further factor is the decline of ‘defined benefit’ pensions. These guaranteed a certain pension usually based on how long you had worked for an employer and how much you earned during your career. The great majority of working age people nowadays have ‘defined contribution’ pensions, where you build up a pension pot over the course of your working life. This then provides you with an income (alongside the state pension and any other investments) when you retire. Anyone with a pension of this type will have important choices to make over how, when and where to save for their pension, and what to do with it once they reach retirement age. Many people who are not financial services professionals understandably struggle with this and need some expert help (I did myself).

Getting professional financial advice can be expensive – typically pension advisers in the UK charge £2,000-£3,000 up front and then 0.5% a year. But a new service called AdviceBridge promises a personalized, affordable retirement planning service. Indeed, they say they can do this for as little as a tenth of the average adviser fee, partly by running the service online and over the phone (no face-to-face meetings required).

Although it is a low-cost service, AdviceBridge is staffed by fully trained and regulated financial advisers, and the company is authorized and regulated by the Financial Conduct Authority (FCA). AdviceBridge never holds investors’ money, even when they assist in the implementation of a retirement plan. The advice they give is though covered by the Financial Services Compensation Scheme (FSCS), which means clients can claim compensation of up to £85,000 if they receive bad advice.

Who Is AdviceBridge For?

In order to keep their charges low, AdviceBridge say that at the moment they are only able to help clients who meet the following criteria:

You are resident and domiciled in the UK.

You are generally in good health.

You do not have any unsecured loans.

You are not currently contributing to pensions with safeguarded benefits such as a final salary pension.

You do not own any buy-to-let property or any non-standard investments.

You do not receive any means-tested benefits.

You would like to plan individually, not as a couple.

How Does It Work?

Assuming you meet the criteria above, you start by filling in an online questionnaire and completing some electronically-signed compliance documents.

As well as the usual contact information, the questionnaire covers such matters as:

your age

your employment status

your annual income

any existing private or company pensions

whether you will qualify for a full state pension

other savings and investments

your target retirement age

how much income you hope to have in retirement

any major outgoings in future you need to plan for

and so on

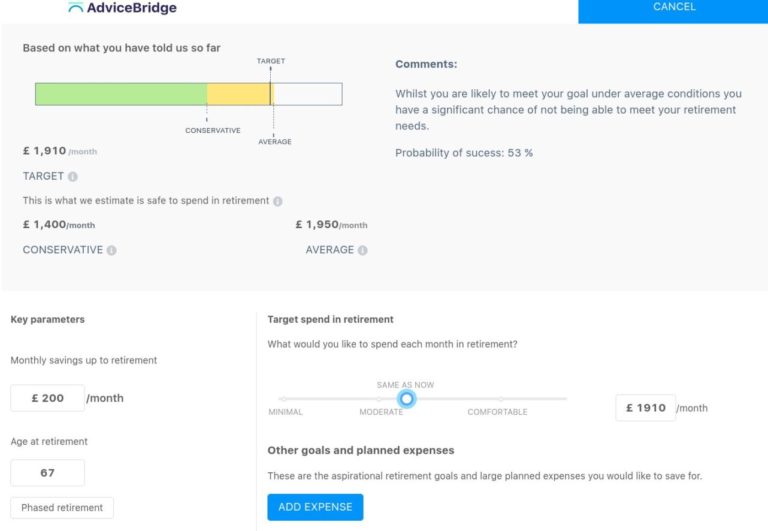

Once you have entered this information, you can create and log in to your account to see an overview of your financial situation. You can adjust the parameters in order to achieve a realistic and sustainable level of retirement income. Here is a screen capture showing part of this (an example account, not mine personally!).

Personalized Plan

Naturally, the above is just the first stage of the process. Once you have provided this information and set up your account, the AdviceBridge advisers will crunch the numbers and (with the aid of their specialist software) produce a personalized plan for you.

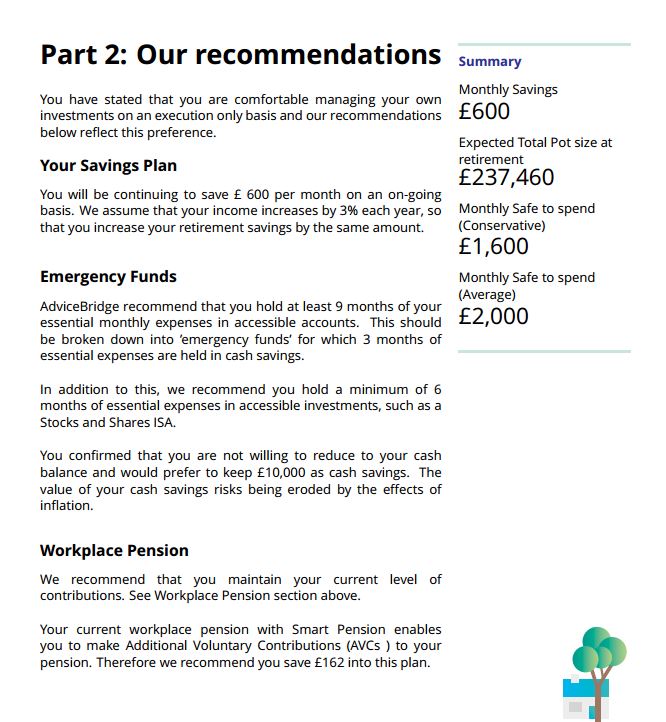

This is obviously a key document. The sample plan I saw came to 39 pages in PDF form. It was divided into three sections: About You, Our Recommendations and Advice, and Appendices.

About You sums up the information you have provided to AdviceBridge via the questionnaire. It covers your personal circumstances, your retirement savings and investments, and your progress so far towards achieving your retirement goals.

Our Recommendations and Advice is the longest section of the plan. It presents recommendations on every aspect of managing your finances for retirement, including restructuring your investment portfolio if required (with specific recommendations for low-cost personal pensions and ISAs). It also examines the likely outcome of following the recommendations, including both average and conservative projections. A sample page from this section of the plan is shown below.

Finally, the Appendices section includes a range of supplementary information, including more detail about the UK state pension, rules about annual pension allowances and taxation, your options for accessing your pension (drawdown, annuities, etc), and more.

It doesn’t end there, though. Once you have had a chance to read and digest your plan, you can arrange a call with a personal financial adviser from AdviceBridge to talk through the advice and recommendations and help you decide how to proceed. The advisers are not paid commission on product sales, so they are able to give unbiased advice about what investments may be best for you based on your specific circumstances.

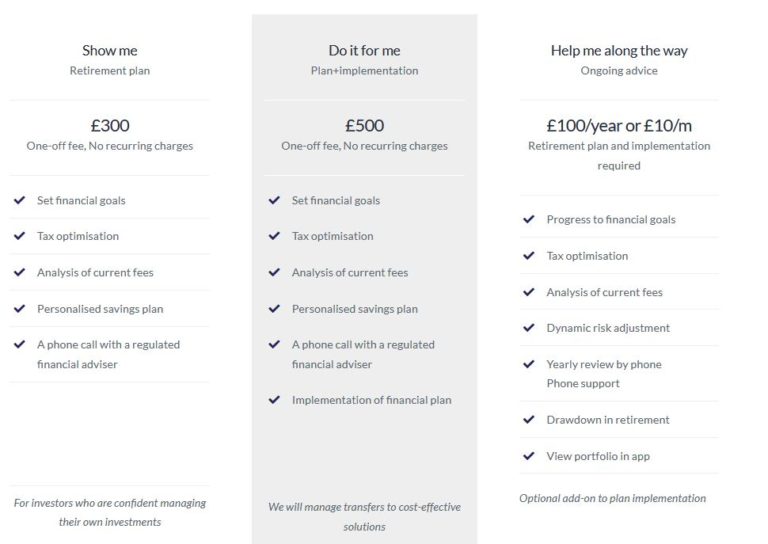

So What Does It Cost?

For the basic AdviceBridge service as described above, there is a one-off fee of £300 with no recurring charges. This service will suit people who are happy to arrange their own investments based on the advice given and the telephone call with an adviser.

If you want AdviceBridge to set up the recommended investments for you – to implement your financial plan, in other words – they will do this as well for an inclusive fee of £500, again with no recurring charges.

Finally, if you opt for the Plan+Implementation service and want ongoing support and assistance too, including dynamic risk adjustment, an annual telephone review, ongoing telephone support, assistance putting your pension into drawdown, and the opportunity to monitor your portfolio online using a dedicated app, AdviceBridge offer all this for an additional £100 a year or £10 a month.

All of the above is summed up in the table below which I have copied from the AdviceBridge website.

My Thoughts

Overall, I have been very impressed by AdviceBridge, both in terms of what they are offering and the prompt and friendly support they provided while I was writing this article. Here are some of the main things I like about their service:

much lower fees than traditional financial advisers

all fees quoted include any taxes due – what you see is what you pay

range of options according to how much (or little) work you want to take on yourself

non-commission-based advisers, so unbiased advice on what investments will suit you best

advisers are free to recommend across the entire range of investment opportunities

all digital process – no need for personal visits or face-to-face meetings

fully FCA authorized company and advisers

advice is covered up to £85,000 under the Financial Services Compensation Scheme (FSCS)

all personal information is securely encrypted

in-depth written advice and recommendations on your retirement finances backed up by telephone support

Any negatives? Well, the only real one I could find is that various groups are currently excluded from the service, e.g. buy-to-let landlords and holders of ‘non-standard investments’. I guess the latter might include me, as I have a proportion of my portfolio in P2P lending and property crowdfunding.

I do of course appreciate that to keep their service so inexpensive AdviceBridge have to streamline their service, but it is a pity if this excludes a significant proportion of people who could benefit from it. I understand that this is something that AdviceBridge keep under review and in future they may remove some of these restrictions. In the mean time, if you aren’t sure whether you are eligible, it is well worth giving them a ring or contacting them via the website to ask (without obligation).

In my opinion, if your circumstances match their criteria, AdviceBridge are well worth checking out. I particularly like their £500 Plan+Implementation service, which covers not only researching and producing a retirement plan for you but implementing it as well. I would also seriously consider paying the extra £100 a year (or £10 a month) for the ongoing service. Obviously that brings the price up a bit further, but it is still far less than you would pay a traditional financial adviser for a similar service.

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: This is a sponsored post for which I am receiving a fixed fee (but no commission). Please note also that I am not a professional financial adviser and nothing in this post should be construed as individual financial advice. Everyone should do their own ‘due diligence’ before investing and take professional advice as appropriate. All investment carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

In February 2017 I wrote this post about premium bonds explaining why I was withdrawing a large amount of the money I had invested in them.

To recap, at that time the interest rate paid on premium bonds (from which the monthly prize fund is calculated) had been cut eight months earlier in June 2016. This led me to sell the majority of my holding, as the amount I was earning in prizes had fallen considerably. The rate was cut again a few months later in May 2017, which led me to sell nearly all my remaining bonds. I now have just £5 left, to avoid closing my account completely.

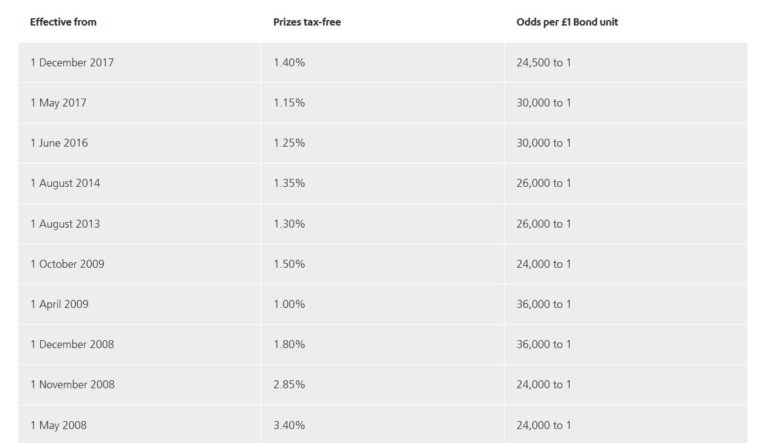

So what has happened since then? The good news for bond owners was that from December 2017 the prize fund was raised by 0.25% to 1.40%. This improved the odds of an individual bond winning a prize in any monthly draw from 30,000 to 1 to 24,500 to 1 (although it still didn’t tempt me to reinvest).

The not-so-good news is that from May 2020 the rate is being cut by 0.1% to 1.3%. As a matter of interest, here is a table copied from the NS&I website showing the changes in prize rates and the odds of winning a prize over the last twelve years. The new rate from May 2020 isn’t shown on the table.

From May 2020 the chances of winning a prize with a single bond will be reduced to 26,000 to 1. Over 170,000 fewer prizes are set to be given out in May 2020 than in February as a result of this change, with less than half the number of £100 and £50 prizes expected to be awarded (source: MoneySavingExpert).

My Thoughts

A first glance you might think that an interest rate of 1.30% percent still isn’t so bad in these days of (very) low interest savings accounts. It’s much the same as the current top paying easy-access savings accounts. Premium bond prizes are tax-free and you can withdraw your capital any time if you need it within a few days. Your money is protected by the UK government and you have an outside chance of winning a life-changing sum. So what’s not to like?

Well, quite a lot in my opinion. Most importantly, although the interest rate is currently 1.40% (reducing to 1.30% in May) in practice most people won’t make this amount. The interest rate is a mean (average) figure and this is skewed by the two one-million pound prizes (which statistically you are highly unlikely to win – see below) and the small number of other other high-value prizes. For these big prizes to be paid out, a lot of people have to win nothing. The more bonds you have, the closer to the average your prize earnings are likely to be. But the reality is that most premium bond owners won’t earn the interest rate quoted (and they may make nothing at all).

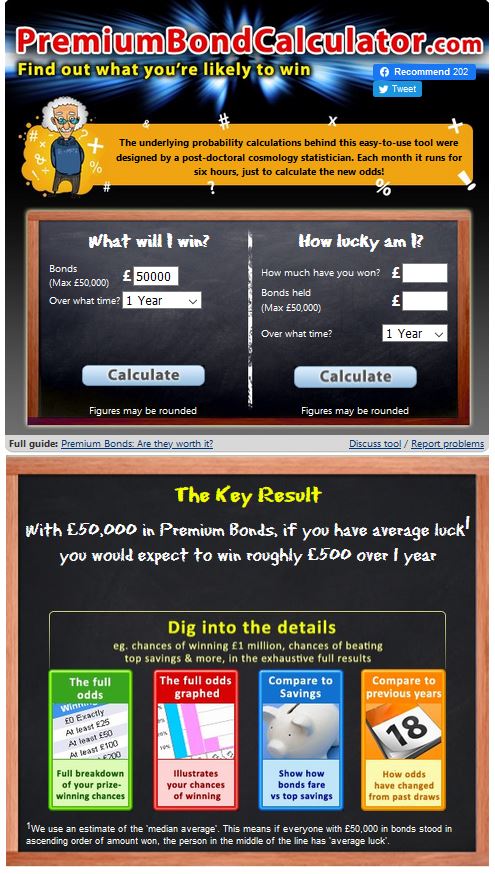

A better measure of what you are likely to make over a year is the median average. The way to think about this is that if you lined up all premium bond-holders with a certain number of bonds (e.g. £50,000) in order from those earning the least in a year (probably nothing) to the most (a million pounds plus), the median is the person right in the middle of the line. Half of all holders will earn more than this person (or the same) and an equal number will earn less. The median in this context is therefore a measure of what you can expect to earn from your premium bonds in a year with ‘average luck’. The clever folks at MoneySavingExpert have built a Premium Bond probability calculator which uses this metric to indicate how much you are likely to win per year, with average luck, with any given holding.

With the £50,000 maximum, the calculator reveals that with average luck you will win just £500 of prizes a year, equivalent to an interest rate of just 1.0 percent (see screen capture below). And that is at the current (February 2020) interest rate. From May 2020 that figure will inevitably go down. Obviously you might have better than average luck, but (as stated above) around half of all bond-holders will have worse. You can read a much more detailed explanation about this on this page of the MSE website.

The calculator also reveals that with £5,000 in premium bonds you could expect to win £50 a year with average luck, and with £1,000 nothing at all. Only about one in three people with £1,000 worth of bonds will win a prize in any one year, so the median (‘average luck’) winnings are zero. Over a two-year period, however, about five out of nine holders of £1,000 will win at least one prize, so the median earnings over two years with £1,000 in bonds are £25 (the lowest and by far the most common prize). This does I guess demonstrate that the ‘average luck’ method used in the MSE calculator has its limitations as a way of estimating likely earnings (although it is still likely to be more accurate than applying the headline interest rate to your investment).

Clearly the longer you hold your bonds, the better are your chances of winning a larger prize, so over a period of years average annual earnings may edge up slightly. Even so, the large majority of bond-holders won’t ever earn the headline rate.

At one time the tax-free status of premium bond prizes would have been a significant attraction, but nowadays that doesn’t apply to nearly the same extent. All basic rate taxpayers now benefit from a Personal Savings Allowance of £1,000 worth of tax-free savings interest every year (higher rate taxpayers get £500 and top rate taxpayers nothing at all). In practice 95% of people now pay no tax on their savings interest. If you are in the 5% who do, premium bonds become a more attractive option. Even so, a typical return of 1% or less, even if it is tax free, isn’t going to set many pulses racing.

Finally, you do of course have a chance of winning a big prize, but it’s important to be realistic about what that chance is. Even with the maximum £50,000 holding, MoneySavingExpert calculate that your chances of winning the million pound top prize in any one year are 1 in 69,876. To put this into perspective, if you had held £50,000 in premium bonds since the year 68000 BC (assuming of course they existed then) with average luck at the current interest rate you could have expected to win the jackpot just once. I looked this up, and 68000 BC is the middle of the Stone Age!

Overall, then, I cannot recommend premium bonds as a home for your savings, especially with the coming rate cut in May 2020.

I can understand why premium bonds are a popular investment, as they offer a bit of excitement every month checking whether you have won and how much. But the fact remains that overall, for most people, the total prize money received is likely to average little more than 1 percent a year at current rates. It may very well be less than this, especially after May 2020 when – as already mentioned – the number of lower value prizes (£25 to £100) will be cut substantially. I look forward to checking on the MSE calculator then to see how much a person with average luck might expect to make in a year.

If you are lucky enough to have £50,000 burning a hole in your pocket, my first advice would be to put enough into an easy-access savings account such as the Post Office Online Saver (currently paying 1.30% including a fixed 0.8% bonus for the first 12 months) to cover your outgoings for up to three months in the event of emergencies. After that, you could invest the balance in a low-cost tracker fund, or a portfolio of investment funds, or a robo-advisory platform like Nutmeg. You could perhaps put a proportion of the money into P2P lending or property crowdfunding as well. Over several years, for the great majority of people, this will outperform an equivalent premium bond portfolio many times over.

As always, if you have any comments or questions about this post, please do leave them below.

If you enjoyed this post, please link to it on your own blog or social media: