Today I’m spotlighting a survey website that wants your opinions and pays cash for them 🙂

The site in question is Y Live. It was previously called Populus Live. You can sign up free of charge, and will then receive email notifications any time they have a survey you may be eligible for.

Each survey is worth a set number of ‘points’. Once you have accrued 50 points you will be sent a cheque for £50 (each point is worth £1, in other words).

The notification emails state how long the survey is expected to take and how many points it is worth. In general, you get 1 point for a five-minute survey, 2 points for a ten-minute one, and so on.

Bear in mind, though, that the timings are Y Live’s estimates, and may not correspond with how long they actually take to complete. For example, I find that ‘five-minute’ surveys can sometimes take ten minutes or longer. Of course, that does reduce the effective hourly rate you receive.

On the other hand, the surveys are generally straightforward and easy to do (though watch out for the attention-checkers). It’s quite possible you will be quicker to complete them than I am.

On occasion you may find yourself screened out of a survey, e.g. if you are not in the target group they are interested in. In that case you won’t be awarded any points, but will get one entry in their monthly prize draw for £250.

Clearly nobody is going to earn a fortune from Y Live, but in my view (and experience) it can make a very worthwhile addition to your sideline-earning portfolio.

As always, if you have any comments or questions about Y Live, please do post them below.

Note: This is an update of an earlier post.

If you enjoyed this post, please link to it on your own blog or social media:

I recently returned from a four-night break on the Isle of Man. It was actually the first time I had ever visited the island, so it’s fair to say I was approaching it with fresh eyes!

For this break I went on a heritage-railway-themed holiday with Newmarket Holidays – here’s a link to the package I booked. I paid a single fee, discussed in more detail below. This included four nights half board in a four-star hotel in the island capital Douglas and my flights to and from the island from Birmingham Airport. The fee I paid also covered transfers from and to Ronaldsay Airport on the IOM and various other things, which I’ll discuss shortly.

For those who don’t know, the Isle of Man is in the Irish Sea, about half way between England and Ireland. It is 32 miles long and – at its widest point – 14 miles across. It covers a total area of around 221 square miles, That makes it nearly five times bigger than Jersey, the largest of the Channel Islands. It is a self-governing British Crown dependency. You can read more about the Isle of Man in this Wikipedia article.

Here is a map of the island from Google Maps…

Flights

As mentioned I flew to the Isle of Man from Birmingham, getting a taxi to and from the airport.

I’d have to say my experience at Birmingham Airport on the outward journey was poor. A lot of building work was going on to install new luggage scanners. As a result the usual queuing areas and escalators were unavailable and passengers had to queue for ages, first to get into lifts to the departures area and then to get through security. I spent almost two hours queuing and by the time I was through it was the final call for my flight. So I then had a mad dash to get to the gate in time. Thankfully I just made it; I’m sure others weren’t as lucky.

The flights were with Scottish airline LoganAir and were actually very good. The isle of Man only attracts relatively small numbers of visitors, so they use small planes and boarding is quick and easy. I was also impressed to be offered free refreshments on both the outward and return flights (something I haven’t experienced on a holiday flight for many years). It took around 50 minutes to get from Birmingham to the IOM, so that was quick and easy too. Of course, if you don’t like flying, you also have the option of going to the island by ferry from Liverpool or Heysham.

I should mention that the return flight back to Birmingham was easy in comparison. Because it’s regarded as a domestic destination, passengers returning to the UK from the IOM don’t have to go through security or passport control. I was out of the airport no more than 15 minutes after landing.

Accommodation

I stayed in a four-star hotel called The Mannin in Douglas. The hotel is just off the main promenade and several other Newmarket Holidays guests were staying there as well.

The hotel room had all the amenities needed for a short stay, including a comfortable double bed, a flat-screen TV, a fridge and electric kettle, and plenty of drawer and wardrobe space. It had an en-suite bathroom with a modern power shower that worked well, with plenty of hot water.

One thing the room didn’t have was a window to the outside world. It had a window leading out to a small balcony, but this was actually within the hotel, overlooking the bar and restaurant area. You may not be surprised to hear that I didn’t use this during my stay 😏

As mentioned, I was staying half-board. Breakfasts were buffet-style and included everything you’d expect, including cooked items such as bacon, sausages, tomatoes, mushrooms and fried or poached eggs (no scrambled, though). I was pleased to discover that the evening meals included my choice of starter, main meal and dessert, with even the most expensive items such as steak at no extra cost. My one slight reservation was that, barring the soup and fish of the day, the menu was the same every night . If I had been staying any longer I might have found this a bit limited. That’s only a very small criticism, though.

Financials

As Pounds and Sense is primarily a money blog, I should say a few words about this.

I paid a total of £1,305 (including VAT) for my four-night visit. That might sound a lot, but as mentioned it included my flights to and from the island, coach transfers, and most meals, along with various other services and amenities. I stayed in a double room with single occupancy, so obviously paid a bit more than a couple would have (pro rata). And finally, I was in a premium four-star hotel. Some other guests were in three-star hotels which I guess would have been a bit cheaper. As a matter of interest, I had to choose the Mannin as it was the only option offered to me when I booked with Newmarket. I guess all the cheaper accommodation had been snapped up already!

The price I paid also included the services of a tour guide, Trevor. He was a local man (from Peel) and extremely knowledgeable about the island. He looked after us very well and even sprang into action when I couldn’t get the top off an ice-cream tub I had bought 🍦😅 Each morning we were picked up by a double-decker bus with Trevor on board. This took us to whatever destination we were visiting first that day (typically a railway station).

Also included in the cost were Isle of Man ‘Go Explore Heritage Cards’. These provided free admission to all the main tourist attractions and also covered travel on the island’s trains and buses. As a result, I actually spent very little extra money during my break – just the odd bit for refreshments during the day and any souvenirs I chose to pick up.

Things To Do

I won’t give you a blow-by-blow account of everything I did on my visit – you can see the full itinerary on the Newmarket Holidays page if you like. I will share some highlights and personal recommendations, though.

1. Douglas: The Capital

This is where I stayed. It is a vibrant, bustling place, with an attractive beach and picturesque promenade you can stroll along. In Douglas you can find the Manx Museum to delve into the island’s history. You can also enjoy a night at the Gaiety Theatre, a beautifully restored Victorian venue offering a variety of performances.

2. Castletown and Castle Rushen

Castletown is the ancient capital of the Isle of Man. Castle Rushen (photo below), one of Europe’s best-preserved medieval castles, is here with its impressive structure and exhibits detailing the island’s past. Also in Castletown you can see the Old House of Keys, the island’s original legislative centre. The trip I was on included admission to the Old House of Keys and an entertaining hour-long interactive presentation there about the island’s history. You would have to book this in advance if not travelling with an organised group.

3. Peel and Peel Castle

The town of Peel is on the island’s west coast and well worth a visit. You can explore the atmospheric ruins of Peel Castle (photo below), and enjoy fresh seafood at one of the local eateries. The House of Manannan museum provides an immersive experience into the island’s Celtic, Viking, and maritime history. You could easily spend a full day here!

4. The TT Mountain Course

For motorsport enthusiasts, the Isle of Man TT (Tourist Trophy) races are legendary. Even outside of race season, you can drive or cycle the 37.73-mile TT Mountain Course, taking in spectacular views and imagining the thrill of the races.

5. Laxey Wheel and Snaefell

The Great Laxey Wheel (see cover image), also known as Lady Isabella, is the largest working waterwheel in the world. If you’re brave (and fit) enough you can go up the spiral steps to a viewing platform at the top. Nearby, the Snaefell Mountain Railway takes you to the island’s highest point. On a clear day it’s said you can see seven kingdoms from here: England, Ireland, Scotland, Wales, the Isle of Man itself, and the kingdoms of Heaven (the sky) and Neptune (the sea). On a more prosaic note, at the top is a nice cafe where you can buy excellent coffee and home-made cake 🍰

6. Isle of Man Steam Railway and Manx Electric Railway

I was on a railway-themed holiday, so naturally this included trips on both of these. The steam railway (photo above) runs through beautiful countryside from Douglas to Port Erin at the southern tip of the island. You get some lovely views of the coast along the way.

The Manx Electric Railway (photo below) also runs from Douglas but in the opposite direction, towards Laxey and then on to Ramsey. The Manx Electric Railway has two carriages, one covered and one open to the elements (referred to colloquially as The Toast Rack!). I went on both during my stay. You get better views from the open carriage but it can be a bit chilly, so remember to wrap up well!

Quick Tips

Here are a few tips for first-time visitors to the Isle of Man based on my own experience and other information gleaned…

1. Plan for the Weather

The Isle of Man has a maritime climate, meaning weather can be unpredictable. It’s advisable to pack layers and waterproofs to stay comfortable regardless of the conditions. That being said, I was extremely lucky on my trip and enjoyed wall-to-wall sunshine.

2. Embrace the Outdoors

With its stunning landscapes, the island is perfect for outdoor activities. Walk a segment of the Raad ny Foillan (Way of the Gull) coastal path, explore glens and waterfalls, or enjoy cycling and bird-watching.

3. Sample Local Delicacies

Don’t miss out on trying Manx kippers, queenies (small scallops), and the island’s renowned ice cream. Local pubs and restaurants often feature these and other regional specialties.

4. Respect Local Traditions

The Isle of Man has a unique culture and traditions, including its own language, Manx Gaelic. You might hear locals using expressions like “Failt Erriu” (Welcome) and it’s appreciated if you can master one or two phrases like this. There are also various superstitions on the island. One of the first I discovered concerned the fairy bridge (quite near the airport). The tour guide told us we must all say “Hello, fairies” as our coach passed over this or bad luck might befall us. Needless to say, everyone complied!

5. Use Contactless Payments

Most places accept contactless payments, but it’s wise to have some cash on hand for smaller vendors and rural areas. Note that if paying by cash you may receive change in Manx notes and coins which are not generally accepted outside the Isle of Man. UK banks will usually exchange Manx banknotes but not coins, so if you get any in your change you will have to keep them as souvenirs, donate them, or hold on to them for your next visit. You can ask retailers if they have UK money available as change, but that is not guaranteed 🙂

Closing Thoughts

As you may gather I enjoyed my holiday on the Isle of Man and am happy to recommend both the island itself and the Newmarket Holidays tour I went on.

The Isle of Man is verdant and charming, with a long and interesting history. Obviously the heritage railways are a particular attraction (for me at any rate!), but so too are the castles at Peel and Castletown and the Great Wheel at Laxey (a beautiful village with a range of other tourist attractions as well). But it’s also a wonderful place to be out walking or cycling, with quiet roads (outside the TT races obviously) and a dramatic and unspoiled coastline. I would definitely like to return there before too long.

As always, if you have any comments or questions about this post, please do leave them below. Also, if you have visited the Isle of Man yourself and have any additional tips or recommendations, I would love to hear them!

If you enjoyed this post, please link to it on your own blog or social media:

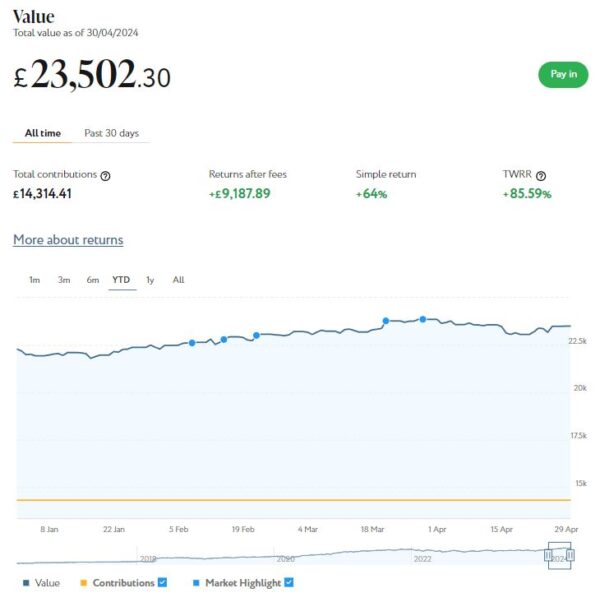

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

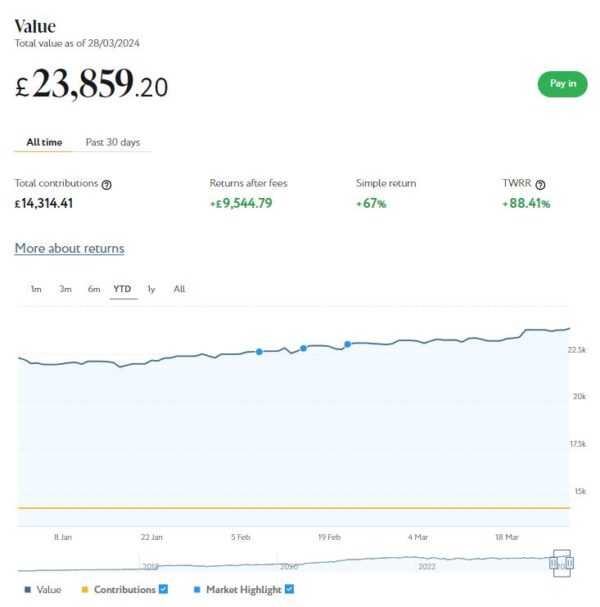

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £23,502. Last month it stood at £23,859, so that is a fall of £357.

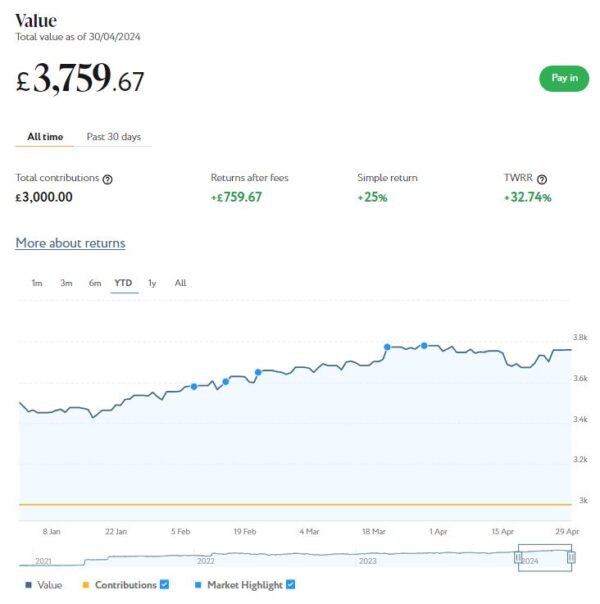

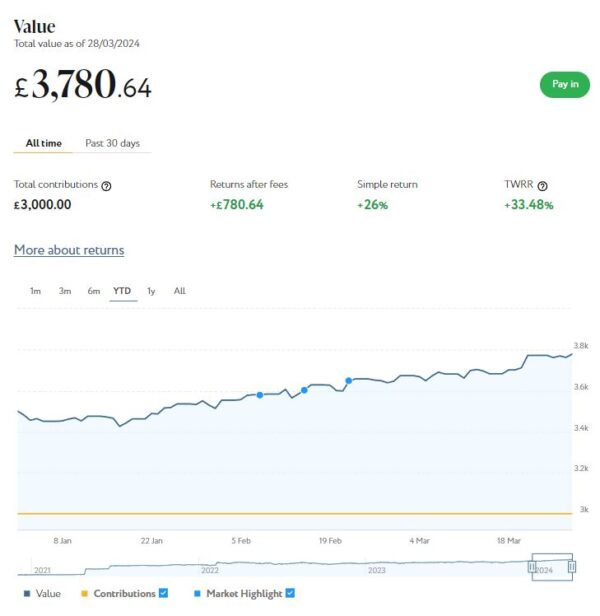

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,760 (rounded up) compared with £3,781 a month ago, a fall of £21. Here is a screen capture showing performance over the year to date.

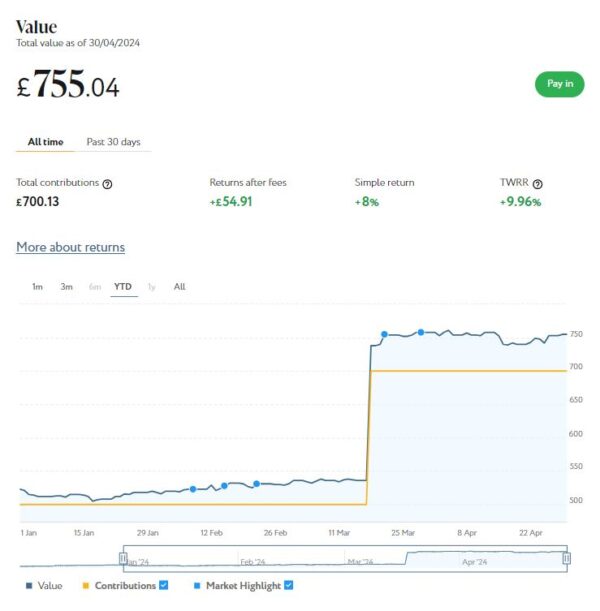

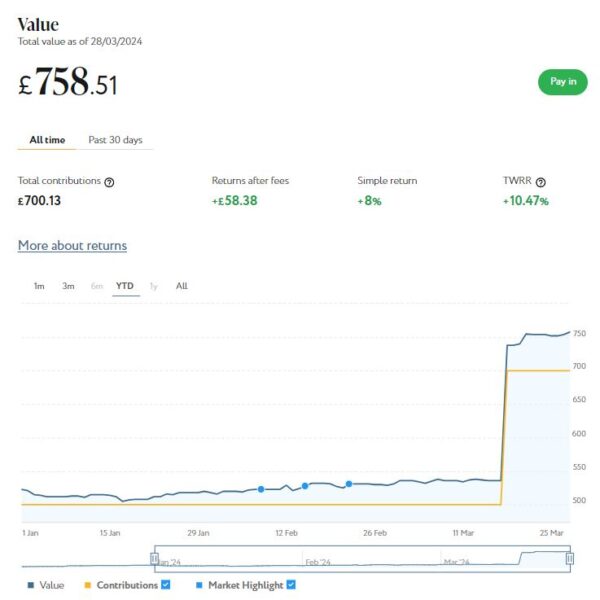

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). In March I also invested a further £200 from ‘Refer a Friend’ bonuses. As you can see from the screen capture below, this portfolio is now worth £755 compared with £759 last month, a small decrease of £4.

It’s obviously a little disappointing that the value of my Nutmeg investments has fallen a bit this month. This is entirely to be expected with investments, however, where ups and downs are the norm. It’s also worth observing that their overall value has risen by £1,392 or 5.29% since the start of the year (not counting the £200 bonus I invested in my thematic portfolio in March).

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Don’t forget, the new tax year began on 6 April 2024 and and you now have a whole new £20,000 tax-free ISA allowance for 2024/25!

I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £1,570 invested with them in 10 different projects paying interest rates averaging around 7%. I also have £14 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual ISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £179.53 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 10 of ‘my’ properties are showing gains, 3 are breaking even, and the remaining 16 are showing losses. My portfolio is currently showing a net decrease in value of £38.96, meaning that overall (rental income minus capital value decrease) I am up by £140.57. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially after Kuflink raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate and becomes more diversified as well.

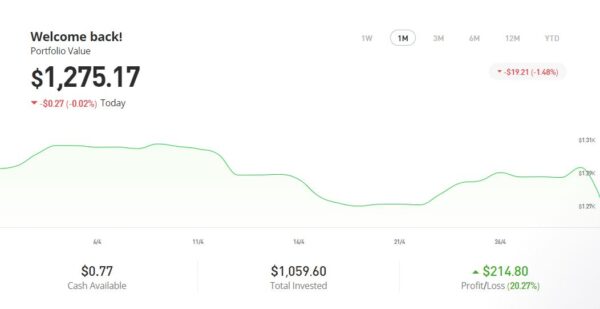

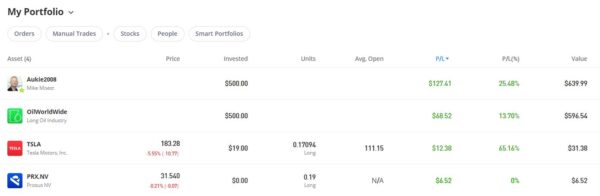

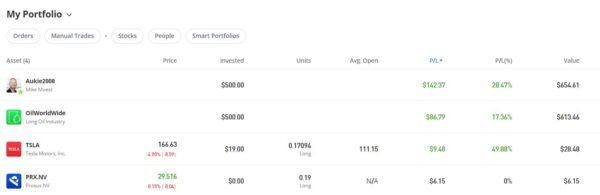

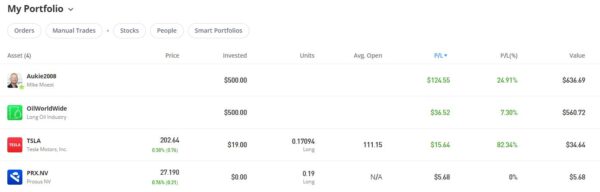

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,275.17, an overall increase of $252.91 or 24.74%.

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had two more articles published in April on the excellent Mouthy Money website. The first is What Is Thematic Investing and Is It For You? In this article I looked at the pros and cons of thematic investing. My editor at Mouthy Money edited the article to remove the specific examples I gave, in case this was construed as personal financial advice. As a consequence the published article is a bit shorter and vaguer than I intended! However, readers of PAS will know that I have thematic investments with Nutmeg and eToro. So far – as mentioned earlier – both have been doing well, but of course there are no guarantees this will continue in future. Thematic investing isn’t for everyone, so take a look at this article, read about the pros and cons, and see if you think it might have a place in your portfolio.

Also in April Mouthy Money published How to Avoid Becoming a Telephone Scam Victim. In this article I set out some tips and advice to avoid falling victim to phone scams. As with online scams, which I discussed in another recent article on Mouthy Money, telephone scams have become an unfortunate reality of daily life in the UK. It’s important to be aware of the risk, and to ensure that any elderly friends and relatives who might be particularly vulnerable don’t fall for them.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. I am a particular fan of my fellow MM contributor and money blogger Shoestring Jane. She writes mainly about money saving and frugal living. Her latest article Eight Ways to be More Mindful With Your Money sets out various ways you may be able to save money relatively painlessly by adopting a more frugal mindset. You can see all of Jane’s articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in April. I won’t bother mentioning those that are no longer relevant now, but the others are listed below.

In Why Now Could Be the Ideal Time to Take Advantage of Your New Tax-Free ISA Allowance I pointed out that (other things being equal) the start of a new tax year is the perfect time to invest in a new ISA. The main reason for this is that the sooner you invest, the more time there is for the power of compounding to start working. There are other good reasons as well for investing now – read the article for more details 🙂

I also published two sponsored guest posts in April. Sponsored posts help pay my bills, but I only accept those that I feel offer genuine value and interest to PAS readers.

Six Tips for Getting Free Stuff Without Dealing With Scams has some good tips for getting valuable freebies online without opening yourself up to a torrent of spam. And Seven Top Money-Saving Websites for Freebies sets out seven websites where you can apply for (genuine) freebies. Understandably my sponsors didn’t want me to link to all the sites as well as the one they were actually promoting, but you should find them easily enough with a little help from Google.

Finally, I posted My Review of the Simba Hybrid Mattress Topper. This is obviously another sponsored post, although in this case I received a free item to review rather than being paid for it. As you will see, this offer came at an opportune time for me. I was genuinely impressed with the Simba Hybrid Mattress Topper, even though it took a bit of effort to get it up the stairs and onto my bed!

Also this year I became a regular contributor to the Over 60s Discounts website. You can read my latest article here: Could You Claim Attendance Allowance? As you will gather, this is all about this invaluable benefit for older people with care needs. It’s estimated that over three million people are eligible for this benefit but not claiming it. Read this article to discover if it’s something you – or an elderly friend/relative – would be qualified to apply for.

I highly recommend registering at Over 60s Discounts, by the way – they list a growing range of discounts and bonuses for older people, including some that are unique to O60D.

Also in April I enjoyed a short break on the beautiful Isle of Man (see cover image). It was the first time I had visited the island, and in fact the first time I had been anywhere by plane since Covid.

I had a great time, with wall-to-wall sunshine until my last day when I was going home anyway. It was a heritage-railway-themed holiday, so I got to ride on the island’s steam and electric trains, and also travelled on buses between towns not served by the railways. The trip was arranged by Newmarket Holidays, and I do recommend this if you are new to the IOM and want a well-organised introductory tour covering all the main places of interest (with a heritage-railway bias, obviously). I will aim to post a fuller review of my Isle of Man holiday on PAS soon.

The one downside to the trip was the chaos on my outward journey from Birmingham Airport. There is loads of building work going on there and, coupled with an apparent shortage of staff, this caused massive queues and delays. Although I arrived before the check-in opened, it took me almost two hours to get through security. By then it was the final call for boarding, so I had to do a mad dash to the gate to avoid missing my flight. There are posters up at the airport saying that all this work will result in a better experience for passengers, but I’ll believe that when I see it. Currently I don’t recommend flying from Birmingham if you can possibly avoid it.

Finally, a quick reminder that you can also follow Pounds and Sense on Facebook or Twitter/X. Twitter/X is my number one social media platform these days and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account, you are definitely missing out!

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

The cover photo, taken by me, shows an Isle of Man Steam Railway train arriving at Port Erin station.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss. Note also that posts on PAS may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

I was recently offered the chance to review the Simba Hybrid Mattress Topper (see cover photo). This is a premium mattress topper from the well-known Simba sleep brand.

I must admit, incidentally, I hadn’t realised the variety of sleep products Simba offer. I knew about their mattresses, of course, but wasn’t aware they also sell quilts, pillows, mattress toppers, and so on.

I currently sleep on a Slumberland king-sized mattress which – despite being barely three years old – is starting to sag. My sleep quality had deteriorated and I was waking up with an aching back and hips. Not good at all 🙁 So when I got the opportunity to test out Simba’s hybrid mattress topper, naturally I leapt at it.

I have tried mattress toppers before, and in fact got a cheap one from Amazon prior to receiving the Simba product. It helped a little but clearly wasn’t going to be the solution for me.

The Simba hybrid mattress topper takes sleep comfort to a whole new level. For starters, it’s deeper and heavier than my previous mattress topper. It came rolled up in a (very) large cardboard box. I wrestled it upstairs and opened it without any help (nobody else being around at the time) but ideally I’d say this is a two-person job.

The mattress topper comes tightly wrapped in a clear plastic bag. Once I removed it from this, it lay flat on the bed without curling. Unlike some sleep products I have ordered in the past, you don’t have to wait for it to expand to its full depth.

From the first night onward I was hugely impressed with the Simba hybrid mattress topper. It is no exaggeration to say that it felt as though I was sleeping on a brand new mattress. It is smooth, cool and comfortable to lie on and (for me anyway) offers just the right medium-to-firm level of support. I am sleeping deeper and longer before waking, and the aches and pains in my back and hips are a thing of the past.

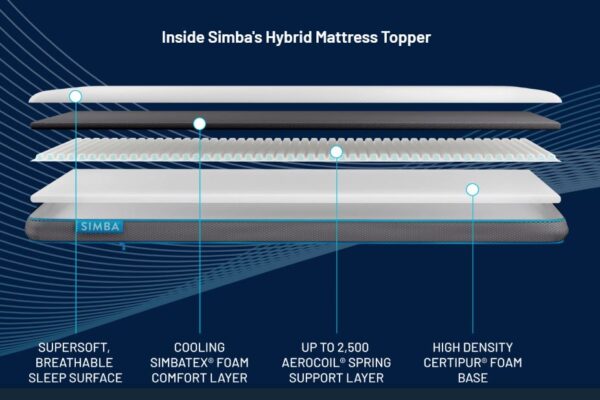

I thought it might be useful to reproduce here the diagram from the Simba web page showing how their hybrid mattress topper is constructed and the different layers it contains…

As you can see, the Simba hybrid mattress topper includes a number of different layers (hence the ‘hybrid’ in the name, I assume). You can read more about this on the Simba web page, but briefly at the top there is a soft, breathable sleep surface, with a foam comfort layer under that. In the middle is a spring support layer (just like in a mattress), with a high-density foam base below that. This is very different from most cheap mattress toppers, which are basically just quilts with a cotton/polyester filling.

Obviously because of its layered structure, you can’t turn the Simba hybrid mattress topper over. You can rotate it from end to end though, and it’s probably a good idea to do so occasionally to even out wear. No instructions are provided about this, however, so that’s purely a suggestion, based on my previous experience with mattresses.

Are there any drawbacks to the Simba hybrid mattress topper? Well, I did notice a slight ‘chemical’ smell which took a few days to disperse. It didn’t bother me, but ideally you might want to let your new mattress topper air for a day or two before starting to use it. I’m afraid I was too impatient to wait, though!

In addition, as this mattress topper contains springs, I wouldn’t recommend trying to wash it (it wouldn’t fit in a standard washing machine anyway!). It does though come with a removable, washable cover. Essentially, you need to treat this product as if it was a mini-mattress in its own right. That isn’t really a drawback to the Simba hybrid mattress topper, just a feature of it.

Overall, I am happy to give the Simba hybrid mattress topper my highest personal recommendation. If – like me – you have an old mattress that is starting to sag, it should prolong its useful life. Also, if you have a mattress that is too hard, it should make it softer and more comfortable for you. It’s not cheap (at the time of writing £219 for the single version or £329 for the king-size I received) – but, as so often in life, you get what you pay for. Easy payment by interest-free instalments (up to 12 months) is also available subject to status.

I should add as well that delivery is free and fast: next working day if you order before 2 pm or two working days if you order after 2 pm. There is also a range of options for buying a Simba double topper.

Many thanks again to my friends at Simba for allowing me to try out their hybrid mattress topper. If you have any comments or questions about this post, as ever, please do post them below as usual.

Disclosure: This is a sponsored post (gifted product).

If you enjoyed this post, please link to it on your own blog or social media:

Today I have another guest post for you on the subject of saving money and getting freebies 🙂

My friends at Hot Free Stuff have put together this list of seven top money-saving websites where you can get freebies, discount codes, downloadable coupons, and more. Check them out, and don’t forget to sign up for free emails from Hot Free Stuff to get all the latest free offers daily!

Are you a stressed-out mum (or dad) trying to make the family budget work?

It takes juggling to make the household budget balance without the need for taking a calculator on every shopping trip. That is because just a click of your mouse or a swipe of your tablet can reel in huge savings on credit card bills, home goods, fashion, electricity, and fun-filled family activities!

We have done the work of trawling the Internet to find you seven of the best money-saving websites around. We’ll help you get freebies, codes, downloadable coupons and more, so that you can do more with your budget every week. Here is our point-and-click guide to savings…

HotFreeStuff.co.uk

This site gets you access to lots of free samples you can really use, from lotions to perfumes. Save money using this site on lots of household goods and get a chance to try new products for free as soon as they are available.

Gumtree

At this so-called ‘classified community’ you can snap up lots of great deals on pets to property. There are many listings for rentals and jobs throughout the UK and Ireland. You will enjoy the deals, but you can also get free items via the freebies section. Just scroll beyond the ads and sponsor links to find many free listings for household items and furniture. At the time of writing there were listings on the London site for free sofas and mattresses, a working Hotpoint fridge-freezer, and free haircuts. Just a word of caution – we suggest for any classified site that you take someone along with you to collect any items, and be careful about giving away too much personal info when responding to ads.

HotUKDeals

This site has been around for well over a decade and is the most reputable place for people to share information on the freebies and discounts they have picked up on their website travels. It is free to register and features include ‘Top 10 Hottest Offers’, requests for offers, and fun, free competitions to enter.

My Voucher Codes

Get over 2000 discount codes at Britain’s biggest voucher website. Tabs include top listings as well as categories, together with the ability to print out vouchers.

Groupon

Never underestimate the power of Groupon! Many times it can seem like a venue for free or cut-price beauty treatments. There are, however, great deals on family attractions, meals and holiday getaways as well.

Moneysaving Expert (MSE)

This massive site set up by financial journalist Martin Lewis has saved the UK millions. It is clearly written, easy to understand, and has lots of information on getting deals on everything from home and car insurance to broadband and mortgages.

Travel Supermarket

This is the best site to find travel deals and compare flights and hotel offers in one easy-to-navigate resource.

Many thanks to Hot Free Stuff for sharing their advice and information. If you have any comments or questions – or other tips and resources for saving money – please do share them below as usual.

Disclosure: this is a sponsored post.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

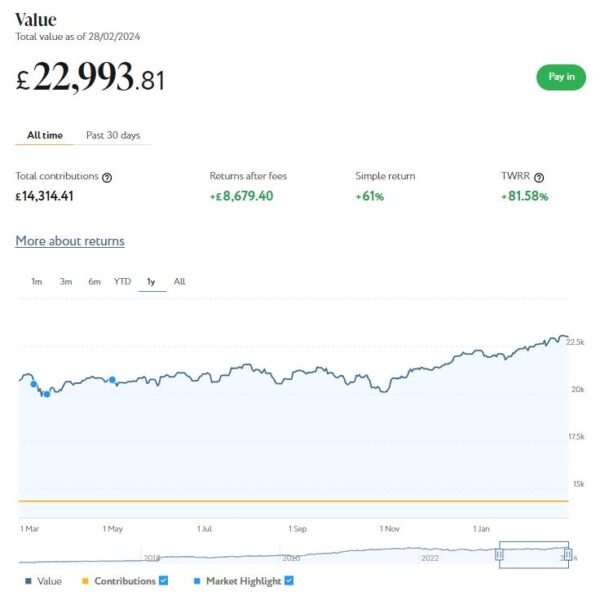

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £23,859. Last month it stood at £22,994 so that is a welcome increase of £865.

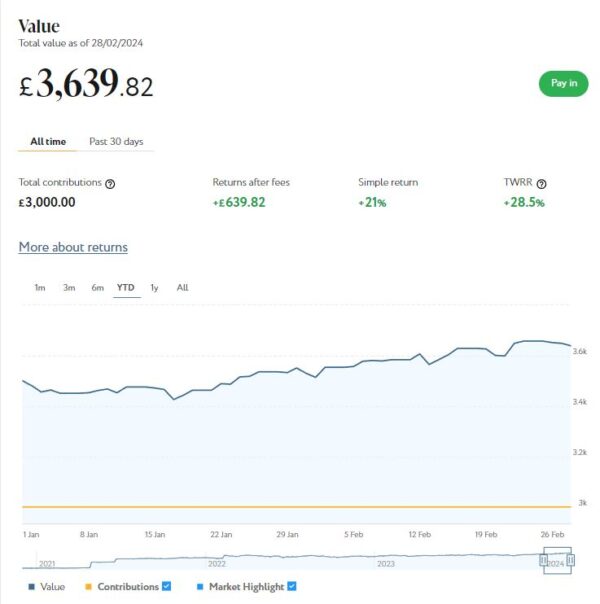

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,781 compared with £3,640 a month ago, a rise of £141. Here is a screen capture showing performance over the year to date.

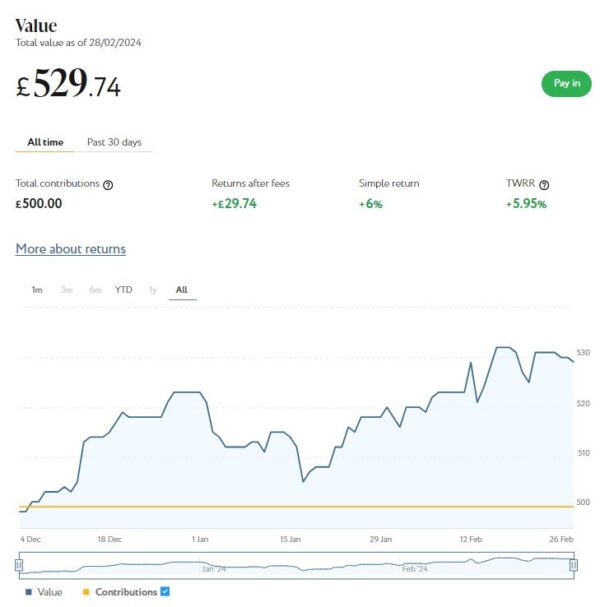

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). As you can see from the screen capture below, this is now worth £759 compared with £530 last month, an increase of £229 since last month.

I should though say that £200 of this is ‘new money’. This came from a ‘Refer a Friend’ bonus, which I decided to pay into this pot rather than withdrawing. So if you disregard that, this portfolio has actually risen in value by £29 since last month.

March was obviously another good month for my Nutmeg investments. Overall – and disregarding the £200 RAF bonus – I was up £1,035 or 3.55%. And since the start of the year (again disregarding the £200 RAF bonus in March) I am up by £1,882 or 7.15%. In these turbulent times I am more than happy with that.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last eight years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Don’t forget, the current tax year ends on 5 April 2024 and after that the 2023/24 tax-free ISA allowance of £20,000 will be gone forever. But the good news is that you will then have a whole new £20,000 ISA allowance for 2024/25!

I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £1,570 invested with them in 10 different projects paying interest rates averaging around 7%. I also have £14 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual iFISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £173.90 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 8 of ‘my’ properties are showing gains, 7 are breaking even, and the remaining 14 are showing losses. My portfolio is currently showing a net decrease in value of £35.05, meaning that overall (rental income minus capital value decrease) I am up by £138.85. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially now that Kuflink have raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate and becomes more diversified as well.

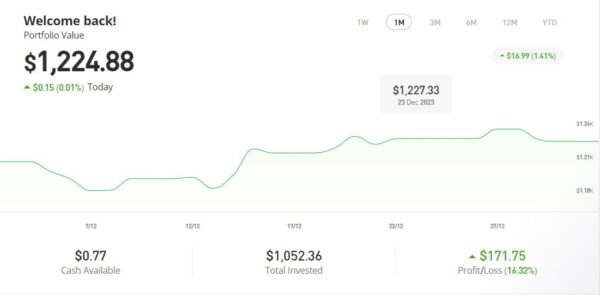

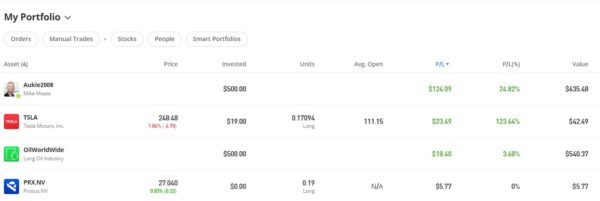

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

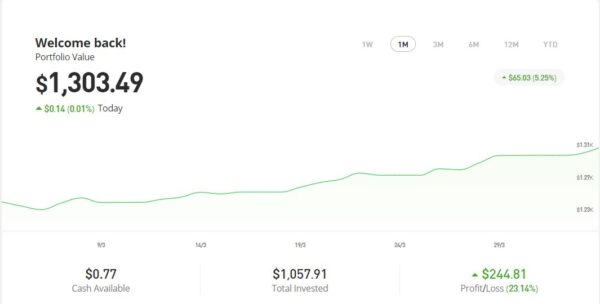

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,303.49, an overall increase of $281.23 or 27.51%.

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had two more articles published in March on the excellent Mouthy Money website. The first is Saving versus Investing – What’s the Difference and Why You Should Do Both. People often get confused between saving and investing, and it doesn’t help that the words are sometimes used loosely and interchangeably. In reality, though, there is a clear difference between them. In this article I explain why saving should always be your first priority, but ideally you should do both.

Also in March Mouthy Money published my article Are Solar Panels Still Worthwhile? As you probably know, solar PV panels generate electricity from sunlight. Growing numbers of homeowners (me included) have them on their roofs. At one time solar panels came with generous payment tariffs known as FiTs (feed-in tariffs), but those days are long gone. So in this article I examine what incentives exist today for installing panels and whether the sums still add up. I also look at the other pros and cons of solar panels.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. I am a particular fan of my fellow MM contributor and money blogger Shoestring Jane. She writes mainly about money saving and frugal living. Her latest article Save Money on Gifts Throughout the Year sets out some top tips for saving money on gifts without (of course!) being a skinflint. You can see all of Jane’s articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in March. I won’t bother mentioning those that are no longer relevant now, but the others are listed below.

One was a reminder that the Trading 212 welcome offer has reopened. If you haven’t done this before, you can get a free share worth up to £100. As I said in the article, my free share in AMD is now worth £151.88! This offer closes on 16 April 2024.

Also in March I published Don’t Miss Out! Use Your £20,000 ISA Allowance Before It’s Too Late. This was a reminder to use your 2023/24 allowance before it vanishes on 6th April 2024. Obviously you will need to move very smartly if you are going to do this now. But (as I said earlier) the good news is that everyone will have a fresh £20,000 allowance from that date.

One other bit of news this month is that I finally got around to buying a home storage battery to connect to my solar panels (see my recent MM article about panels). I used a local (Staffordshire) company called The Energy Box for this, and am very happy to recommend them.

I’ve had my battery for just over a fortnight now and it’s been quite eye-opening. Using the battery app I can see how much electricity my solar panels are generating at any time and how much I am using in my home. I can also check the battery charge level and whether it’s charging or discharging. Even at this time of year, if there’s a bit of sunshine I am generating enough electricity in the day to cover my needs and charge the battery to a level where I’m running the house from it till well into the evening.

In the summer I’d expect to be generating enough to live off solar-generated power entirely, meaning there will only be the dreaded standing charge to pay. So I will actually be saving more money than I originally anticipated, though admittedly it will still be a number of years before the cost is covered.

It wasn’t just a financial decision, though. My other aim was to be able to continue as normal in the event of power cuts (which I expect to become more frequent in coming years as the UK transitions away from fossil fuels), and that should be the case too. The only issue might be a power cut in the depths of winter when the battery hasn’t charged up from the panels. Even so, if I know (or suspect) a cut is coming I can charge the battery in advance from the mains.

I’ve written an article going into more detail about home storage batteries (including my own) for my regular clients at Mouthy Money. This will be published in April, so keep an eye out for it!

Finally, a quick reminder that you can also follow Pounds and Sense on Facebook or Twitter/X. Twitter/X is my number one social media platform these days and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account, you are definitely missing out!

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

As the screenshot below for the last 12 months shows, my main Nutmeg portfolio is currently valued at £ £22,994. Last month it stood at £22,386 so that is a welcome increase of £608.

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,640 compared with £3,530 a month ago, a rise of £110. Here is a screen capture showing performance over the last 12 months.

Finally, at the start of December 2023 I invested £500 in one of Nutmeg’s new thematic portfolios (Resource Transformation). As you can see from the screen capture below, this is now worth £530, an increase of £11 since last month and £30 or 6% over the three-month period since I first invested.

February was obviously a good month for my Nutmeg investments. Overall I was up £737 or 2.79%. In these turbulent times I am more than happy with that.

You can read my full Nutmeg review here. If you are looking for a home for your annual ISA allowance, based on my overall experience over the last seven years, they are certainly worth considering. They offer self-invested personal pensions (SIPPs), Lifetime ISAs and Junior ISAs as well.

Don’t forget, the current tax year ends on 5 April 2024 and after that the 2023/24 tax-free ISA allowance of £20,000 will be gone forever!

I also have investments with the property crowdlending platform Kuflink. They continue to do well, with new projects launching every week. I currently have around £1,570 invested with them in 10 different projects paying interest rates averaging around 7%. I also have £14 in my Kuflink cash account.

To date I have never lost any money with Kuflink, though some loan terms have been extended once or twice. On the plus side, when this happens additional interest is paid for the period in question.

There is now an initial minimum investment of £1,000 and a minimum investment per project of £500. Kuflink say they are doing this to streamline their operation and minimize costs. I can understand that, though it does mean that the option to test the water with a small first investment has been removed. It also makes it harder for small investors (like myself) to build a well-diversified portfolio on a limited budget.

One possible way around this is to invest using Kuflink’s Auto/IFISA facility. Your money here is automatically invested across a basket of loans over a period from one to five years. Interest rates range from 7% to around 10%, depending on the length of term you choose. Full up-to-date details can be found on the Kuflink website.

You can invest tax-free in a Kuflink Auto IFISA. Or if you have already used your annual iFISA allowance elsewhere, you can invest via a taxable Auto account. You can read my full Kuflink review here if you wish.

Moving on, my Assetz Exchange investments continue to generate steady returns. Regular readers will know that this is a P2P property investment platform focusing on lower-risk properties (e.g. sheltered housing). I put an initial £100 into this in mid-February 2021 and another £400 in April. In June 2021 I added another £500, bringing my total investment up to £1,000.

Since I opened my account, my AE portfolio has generated a respectable £168.53 in revenue from rental income. As I said in last month’s update, capital growth has slowed, though, in line with UK property values generally.

At the time of writing, 10 of ‘my’ properties are showing gains, 4 are breaking even, and the remaining 15 are showing losses. My portfolio is currently showing a net decrease in value of £40.01, meaning that overall (rental income minus capital value decrease) I am up by £128.52. That’s still a decent return on my £1,000 and does illustrate the value of P2P property investments for diversifying your portfolio. And it doesn’t hurt that with Assetz Exchange most projects are socially beneficial as well.

The overall fall in capital value of my AE investments is obviously a little disappointing. But it’s important to remember that until/unless I choose to sell the investments in question, it is largely theoretical, based on the most recent price at which shares in the property concerned have changed hands. The rental income, on the other hand, is real money (which in my case I’ve reinvested in other AE projects to further diversify my portfolio).

To control risk with all my property crowdfunding investments nowadays, I invest relatively modest amounts in individual projects. This is a particular attraction of AE as far as i am concerned (especially now that Kuflink have raised their minimum investment per project to £500). You can actually invest from as little as 80p per property if you really want to proceed cautiously.

As I noted in this recent post, Assetz Exchange is particularly good if you want to compound your returns by reinvesting rental income. This effectively boosts the interest rate you are receiving. Personally, once I have accrued a minimum of £10 in rental payments, I reinvest this money in either a new AE project or one I have already invested in (thus increasing my holding). Over time, even if I don’t invest any more capital, this will ensure my investment with AE grows at an accelerating rate.

In 2022 I set up an account with investment and trading platform eToro, using their popular ‘copy trader’ facility. I chose to invest $500 (then about £412) copying an experienced eToro trader called Aukie2008 (real name Mike Moest).

In January 2023 I added to this with another $500 investment in one of their thematic portfolios, Oil Worldwide. I also invested a small amount I had left over in Tesla shares.

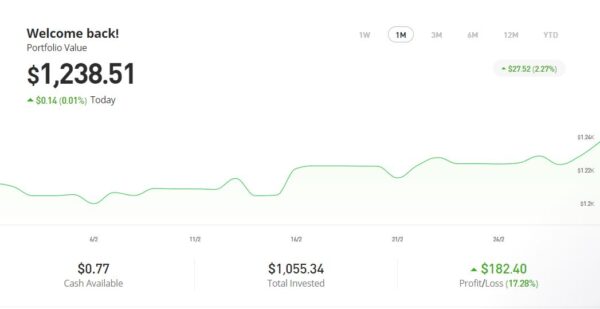

As you can see from the screen captures below, my original investment totalling $1,022.26 is today worth $1,238.51, an overall increase of $216.25 or 21.15%.

eToro also offer the free eToro Money app. This allows you to deposit money to your eToro account without paying any currency conversion fees, saving you up to £5 for every £1,000 you deposit. You can also use the app to withdraw funds from your eToro account instantly to your bank account. I tried this myself and was impressed with how quickly and seamlessly it worked. You can read my blog post about eToro Money here. Note that it can also serve as a cryptocurrency wallet, allowing you to send and receive crypto from any other wallet address in the world.

I had three more articles published in January on the excellent Mouthy Money website. The first is How to Save Money on Motoring. Like everything else in life the cost of motoring is going up and up, so in this article I set out a variety of ways – from ride-sharing to driving for fuel economy – you may be able to reduce it.

Also in February Mouthy Money published Are You Making the Most of Your Annual ISA Allowance?. As mentioned earlier, the 2023/24 tax year ends in just a few weeks’ time. And after that the £20,000 tax-free ISA allowance for that year will be gone forever. In this article I describe the different types of ISA – Cash ISA, Stocks and Shares ISA, Innovative Finance ISA (IFISA) and Lifetime ISA (LISA) – and explain how they work and the differences between them. I also provide some tips and advice for making the most of your annual ISA allowance.

My final article published on Mouthy Money last month was Can You Save Money on Your Shopping with JamDoughnut? Regular PAS readers will know that I am a fan of the JamDoughnut app, which enables you to save up to 20% on purchases with a growing range of retailers. The article also reveals how you can get a £2 head-start by using my referral code.

As I’ve said before, Mouthy Money is a great resource for anyone interested in money-making and money-saving. I am a particular fan of my fellow MM contributor and money blogger Shoestring Jane. She writes mainly about money saving and frugal living. Her latest article Frugal Skills to Save You Money sets out a selection of life skills that can save you money (and aren’t hard to learn). You can see all of Jane’s articles for Mouthy Money via this web page.

I also published several posts on Pounds and Sense in February. I won’t bother mentioning those that are no longer relevant now, but the others are listed below.

In Get Your Will Written Free of Charge in March I revealed how you can get your will written (or updated) free of charge during Free Wills Month. This regular event supports a range of leading charities. Obviously the hope is that you will include a bequest to charity in your will, but there is absolutely no obligation to do this. Free Wills Month is now up and running. If you want to take advantage and get your will written free, I recommend acting now as there are only limited spots available.

Also in March I published a guest post titled Building Your Own Home – It’s Not Just for the Super Rich! This post was written on behalf of Suffolk Building Society, who are trying to raise awareness of the self-build option in the UK. As they say in the article, they can provide mortgages to purchase land suitable for self-build projects. SBS emphasize that this option is suitable and available for ‘ordinary people’, not just the super-rich folk you see on TV shows like Grand Designs!

I also published Saving for a Rainy Day or a Stormy Breakup? The Surprising Facts About Secret Savings Accounts. This post is based on some eye-opening research from my friends at Smart Money People, which revealed (among other things) that one in ten people in a serious relationship, including marriage, civil partnerships, or cohabitation, maintain a secret savings account. Find out more in this post.

Also, from January this year I became a regular contributor to the new Over 60s Discounts website. You can read my latest article here: Who Cares for the Carers? This is about help available for unpaid carers in the UK, both financial and practical. I highly recommend registering at Over 60s Discounts, by the way – they list a growing range of discounts and bonuses for older people, including some that are unique to O60D.

One other thing is that this month I switched my Santander 123 Lite current account to a Santander Edge current account. I will try to find time to write a separate post about this soon. But briefly, my main reason was because having an Edge current account allows you to open an Edge savings account, which offers a market-leading 7% interest rate (AER) for amounts of up to £4,000 for one year (it then falls to 4.5% AER).

The Santander Edge account has slightly higher fees (£3 a month as opposed to £2) and the cashback on offer is slightly less. However, when I crunched the numbers, the value of having an Edge savings account easily outweighed this. Though I am fortunate in that I had £4,000 I could put into it immediately from another, lower-paying savings account. If I hadn’t had that, it wouldn’t have been worth switching to the Edge account.

Finally, a quick reminder that you can also follow Pounds and Sense on Facebook or Twitter/X. Twitter/X is my number one social media platform these days and I post regularly there. I share the latest news and information on financial (and other) matters, and other things that interest, amuse or concern me. So if you aren’t following my PAS account, you are definitely missing out!

That’s all for today. As always, if you have any comments or queries, feel free to leave them below. I am always delighted to hear from PAS readers

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that posts may include affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered, but it does help support me in publishing PAS and paying my bills. Thank you!

If you enjoyed this post, please link to it on your own blog or social media:

In the world of investing, there’s a powerful force that has the potential to turn small contributions into substantial wealth over time.

This force is known as compounding, and when combined with the magic of compound interest, it becomes a powerful tool for building wealth and long-term financial success.

For savers and investors, harnessing the power of compounding can be the key to achieving your financial goals.

The Basics of Compounding

Compounding is a simple yet highly effective concept that involves earning interest on both your initial investment and the accumulated interest from previous periods. In other words, it’s the process of generating earnings on an asset’s reinvested earnings. The longer your money remains invested, the more significant the compounding effect becomes.

Let’s consider a hypothetical scenario to illustrate the point. If you invest £1,000 with an annual interest rate of 5%, you would earn £50 in the first year. In the second year, however, you wouldn’t just earn interest on your initial £1,000, you would also earn interest on the £50 you earned in the first year (at 5% that would be another £2.50). Over time, this compounding effect can result in exponential growth.

The Magic of Compound Interest

Compound interest takes compounding to the next level. Unlike simple interest, where you only earn interest on the principal amount, compound interest allows you to earn interest on both the principal and the previously earned interest. This compounding occurs at regular intervals, such as annually, quarterly, or monthly, depending on the investment vehicle. In general, the more frequently compounding occurs, the faster your money will grow.

Compound interest can make a significant difference to the growth of your wealth. Whether you’re investing in stocks, bonds, or other financial instruments, the power of compound interest allows your money to work harder for you, potentially accelerating your journey towards financial freedom.

The Importance of Time in Wealth Building

A critical factor in maximizing the benefits of compounding and compound interest is time. The earlier you start investing, the longer your money has to grow, and the more substantial the compounding effect becomes. This is sometimes referred to as the ‘time value of money’.

For example, let’s compare two imaginary investors, Jane and Bob. Jane starts investing £1,000 per year at the age of 25 and continues until she’s 35, contributing a total of £11,000. Bob, on the other hand, starts investing the same amount at 35 and continues till he’s 65, contributing a total of £31,000.

Assuming an annual return of 7%, Jane’s investments will grow significantly more than Bob’s due to the extra years of compounding, despite the fact she invested £20,000 less than Bob in total. In this scenario, Jane’s investment would grow to over £193,000 by the time she is 65, while Bob’s would reach around £148,000. The difference is striking and emphasizes the importance of an early start in wealth building.

Key Steps for Investors

Start Early: The earlier you begin investing, the more time your money has to compound and grow. Even small amounts invested regularly can lead to substantial wealth over the long term.

Reinvest Earnings: Instead of cashing out your investment earnings, reinvest them to take full advantage of compounding. Reinvesting dividends and interest compounds your returns, accelerating wealth accumulation.

Diversify Your Portfolio: A diversified investment portfolio helps spread risk and enhances long-term returns. Consider a mix of stocks, bonds and other assets to optimize your investment strategy.

Stay Disciplined: Consistency is key when it comes to compounding. Stick to your investment plan, contribute regularly, and avoid unnecessary withdrawals to maximize the long-term benefits.

Practical Examples

Although compounding is often discussed in regard to cash savings, as indicated above the principle applies very much with stock-market-type investments as well.

To take one example from my own experience, regular readers will be aware that I have some money in the P2P property investment platform Assetz Exchange [referral link]. This platform specializes in relatively low-risk social housing projects where rents are typically paid by charities and housing associations or the government (e.g. asylum seeker hostels). Here is a link to my original review of Assetz Exchange.

With all my AE investments, I receive pro rata rental distributions every month. My investment is quite modest so these aren’t huge amounts in themselves. But once they have added up to a reasonable sum (say £10 or more) I reinvest them in another AE project or increase my holding in an existing one. From the following month I then start receiving distributions from these investments as well. That means my investment and monthly returns are building steadily, month by month, through the power of compounding.

Obviously that’s just one example. But Assetz Exchange works particularly well for this, as the minimum investment per project is so low (as little as 80p in some cases). So even if you are only investing relatively small amounts like me, you can still harness the power of compounding to grow your money.

FYI, in January 2025 Assetz Exchange rebranded as Housemartin. It still works the same way, with just one or two minor changes. See my blog post for further info.

That’s just one possible approach, of course. Another would be to invest in dividend-paying shares and reinvest the dividends when they arrive in more such shares. This approach to investment was discussed a while ago on PAS in a guest post by Lewys Lew.

Whatever your chosen investment vehicle, reinvesting your interest, income or dividends will help you grow it faster using the power of compounding.

Final Thoughts

As I hope I’ve shown in this post, the power of compounding and compound interest is a wealth-building secret every investor should embrace.

By understanding these concepts and implementing a disciplined and long-term investment strategy, you can harness the power of compounding to achieve your financial goals.

Start early, stay committed, and let compounding work its magic on your road to financial success 🙂

As always, if you have any comments or questions about this post, please do leave them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

If you enjoyed this post, please link to it on your own blog or social media:

In my post today I’m focusing on the trading and investment platform eToro. I originally reviewed eToro in this post.

eToro is a global fintech company with its HQ in Israel. The company has registered offices in Cyprus, the UK, the US and Australia. It is a hugely popular platform with 25 million customers from over 140 countries across the world. They offer a range of share trading and investment services.

eToro is regulated and authorised in the UK by the Financial Conduct Authority (FCA) and is covered by the Financial Services Compensation Scheme (FSCS). That means if eToro were to go bust any cash deposits with them up to £85,000 would be protected. Of course, the FSCS doesn’t protect you if you lose money simply due to your investments performing poorly.

What is Copy Trading?

Copy trading is a very popular feature of eToro. As mentioned, it allows you to automatically copy the trades of established eToro investors and benefit from the profits they (hopefully) make.

eToro has hundreds, probably thousands, of approved ‘popular investors’ whose trades you can copy automatically on the platform. They each have a profile page where you can find out more about them and their investment strategy.

On a trader’s profile page you can see various stats about them, including how many copiers they have and how many people are following them. You can also check their profits over various timeframes (though of course this is no guarantee of how successful they will be in the future).

eToro operates in US Dollars, though that isn’t an issue for UK investors (see tips, below). There’s a minimum investment of $200 (around £165) for copy trading. However, many approved traders recommend a higher minimum than this. That’s because, when you sign up to copy a trader, eToro automatically duplicates all of that person’s trades in proportion to the size of your investment.

eToro has a minimum investment size of $1 and if a trade would work out less than that pro rata it won’t be executed. It follows that traders whose strategies typically involve placing large numbers of relatively small trades generally recommend a higher minimum starting investment.

One of the biggest attractions of copy trading is that no charges are payable. The traders in question receive commission from eToro for the business they bring in for the company. So in effect you are getting privileged access to the skills and expertise of these people at no cost to yourself.

You are allowed to copy up to 100 different popular investors, though you can of course start with just one.

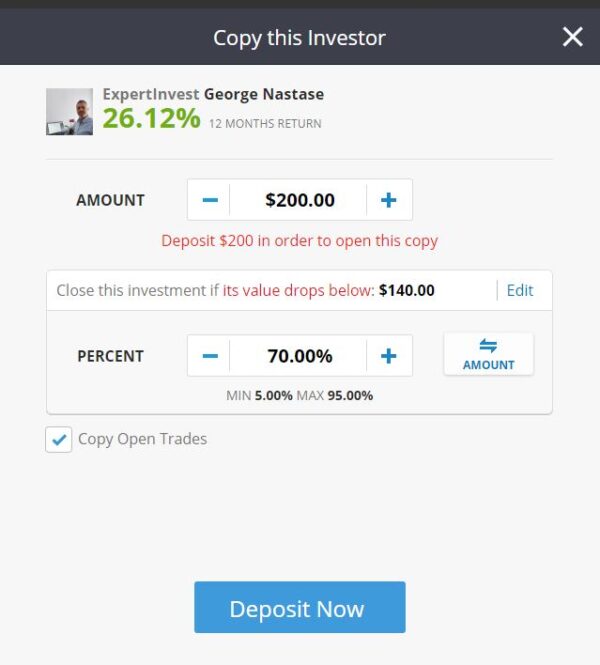

How to Copy a Trader

Before you can start copy trading, you will need to register for an account with eToro and deposit some funds with them. I talked about this in my original eToro review.

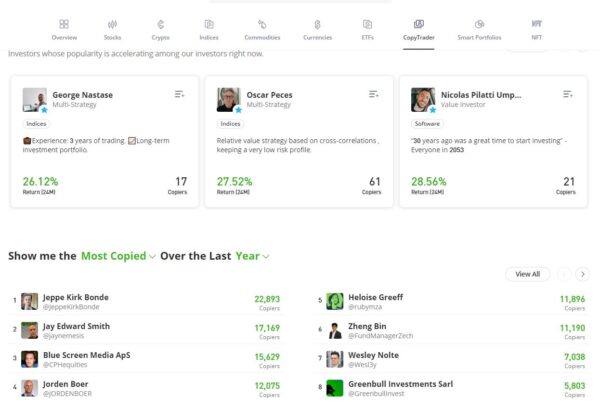

Once you have done this, you can check out popular investors on the platform by clicking on Discover in the left-hand menu of your dashboard when logged on, then clicking on CopyTrader near the top.

A new page will open showing the most popular copy traders and also those whose copier numbers are currently growing the fastest (probably due to good recent performance). Here’s a screen capture showing part of this page at the time of writing:

.

You can also use the search facility to search for popular investors according to where they are based, what they invest in, and how much profit they have made within a certain period.

Once you’ve found an investor you want to copy, click on the green ‘Copy’ button on their profile page. A pop-up box such as the one below will then appear. Enter the total amount you want to invest at the top.

You also have to choose whether you want to copy all existing open positions as well as new ones. ‘Copy Open Trades’ is the default, and if you want to do this you should leave the box in question ticked. If you uncheck the box, only new trades opened after you start investing will be copied.

One drawback with copying all open positions is that you’ll be investing in these trades at the current price, whatever it is, instead of the price when the trader concerned opened their position. If the price has gone up since then, the profit potential may be less. On the other hand, if you opt only to copy new trades, it may be some time before your money is fully invested. There are pros and cons either way, but ultimately the longer you stay invested, the less difference this decision is likely to make.

Another choice to make here concerns the CopyTrader Stop Loss (CSL). If your copy value falls by that amount, the CSL will automatically terminate the copy relationship and return the remaining money to your eToro balance. You can set this figure anywhere between 5% and 95%. My advice is not to set it too high, as even a brief ‘wobble’ will then trigger the stop loss and crystallize your losses (see tips, below).

If any of the above sounds at all daunting, note that everyone on eToro also gets a $100,000 virtual portfolio to practise with. You can copy trade using this virtual money to see how the process works and what returns you make.

My Experience of Copy Trading

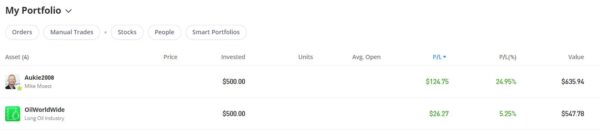

In June 2022 I invested $500 (then about £412) copying a Netherlands-based eToro trader called Aukie2008 (real name Mike Moest). I chose him for various reasons, including his eToro profit record and the number of followers he had already.

On his profile page he came across as a likeable, straight-talking individual, as well as being an experienced and knowledgeable trader. He posted regular updates on his strategies and on investing generally. I also liked the fact that he always took the trouble to answer questions posted by his followers. His recommended minimum starting investment was $500.

Unsurprisingly in these volatile times, my investment has been up and down, but it is currently (after 18 months) about $125 (25%) in profit. All things considered I am very happy with that.

In due course I may top up my copy trading investment with Aukie2008. I may also diversify my investments, either by following another approved trader or perhaps via another themed smart portfolio. As regular PAS readers will know, a few months ago I invested $500 in the Oil Worldwide smart portfolio. As the screen capture below shows, this has done okay, though not as well as my copy trading investment. It’s still early days, though.

Top Tips for Copy Traders

Here are some top tips to help you make the most of the copy trading facility on eToro. These are based partly on my own experiences, but also on other comments and advice I have seen.

As mentioned above, check the minimum recommended investment for any trader you are thinking of following and be sure to invest this amount of money or more.

Note also the risk score assigned by eToro. Each approved trader is allocated a score between 1 and 10, with 1 representing very low risk and 10 the highest. Scores are based on the number, size and type of trading activities they engage in. If you are just starting out you might prefer to begin with someone relatively low risk (say 5 or lower) and work up from there as you gain experience on the platform.

Other things being equal, when following a trader I recommend choosing ‘Copy Open Trades’. This will ensure all your money is put to work immediately. As mentioned above, it does mean some positions may not have the same profit potential as when they were opened, but the longer you remain invested, the less this will matter overall.

Also, as mentioned earlier, don’t set your CSL too high. Doing so will mean even a slight wobble may trigger your stop loss and crystallize your losses. Personally I wouldn’t set this figure any higher than 70%, but it’s your decision, of course, based on your tolerance for risk.

To keep currency conversion costs to a minimum, I strongly recommend opening a separate eToro Money account. This will allow you to deposit instantly to your eToro account without paying currency conversion fees or charges.

Remember one key principle of successful investing is diversification. You should therefore consider copying a number of traders with different investment strategies rather than just one. In addition, eToro offers a range of other investment opportunities as well, including individual company shares and themed portfolios.

Even though you’re following an approved trader, you should still monitor his/her results carefully and be prepared to switch if it seems they are losing their touch.

I recommend reading all the updates on the trader’s profile page too. Not only do these provide valuable background about their strategies, you can also learn a lot about the thought processes of professional traders.

Finally, don’t forget that everyone on eToro also gets a $100,000 virtual portfolio to practise with. You can use this to try out copy trading or any other type of investment without risking any real money.

Closing Thoughts

If you’re looking for an interesting (and somewhat unusual) investment opportunity, copy trading on eToro is certainly worth considering.

In effect, your portfolio is managed on your behalf by an experienced professional trader, whose expertise you get access to at no direct cost to yourself. There are plenty of approved traders to choose from, and you can study their past performance and personal updates via their profile pages before picking one (or more) to follow.

As always, if you have any questions or comments about this article, please do post them below.

Disclaimer: I am not a qualified financial adviser and nothing in this blog post should be construed as personal financial advice. Everyone should do their own ‘due diligence’ before investing and seek professional advice if in any doubt how best to proceed. All investing carries a risk of loss.

Note also that this post includes affiliate links. If you click through and perform a qualifying transaction, I may receive a commission for introducing you. This will not affect the product or service you receive or the terms you are offered.

This is a fully updated version of my original (2022) blog post about copy trading on eToro.

If you enjoyed this post, please link to it on your own blog or social media:

I’ll begin as usual with my Nutmeg Stocks and Shares ISA. This is the largest investment I hold other than my Bestinvest SIPP (personal pension).

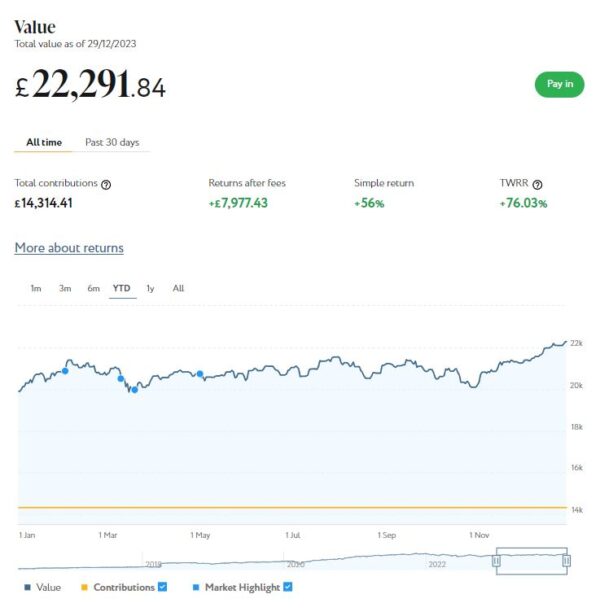

As the screenshot below for the year to date shows, my main Nutmeg portfolio is currently valued at £22,292. Last month it stood at £21,282 so that is an increase of £1,010.

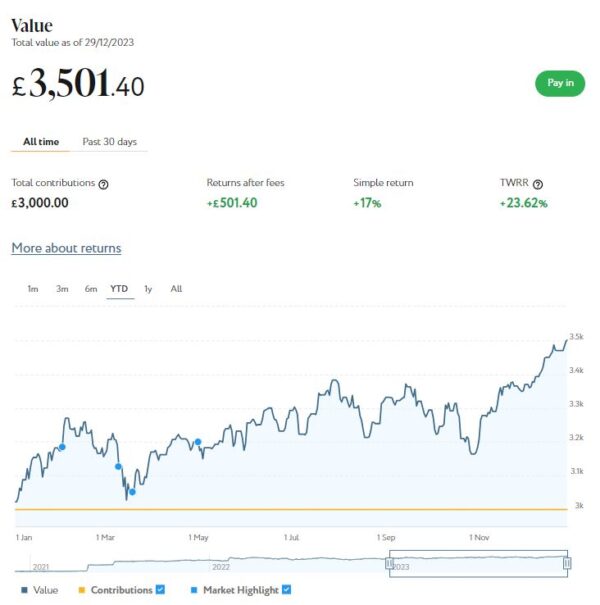

Apart from my main portfolio, I also have a second, smaller pot using Nutmeg’s Smart Alpha option. This is now worth £3,501 compared with £3,351 a month ago, a rise of £150. Here is a screen capture showing performance since the start of this year.

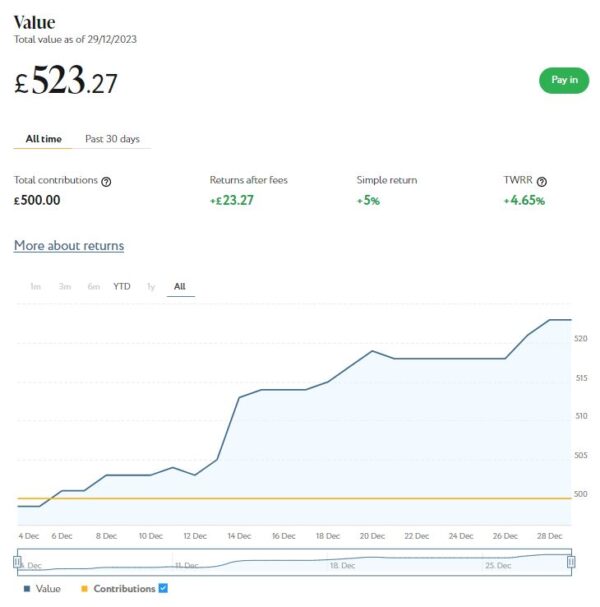

Finally, at the start of December I invested £500 in one of Nutmeg’s new thematic portfolios (discussed further below). This has now grown to £523, an increase of £23 or 4.6%. That would equate to an annual interest rate of just over 55%. Naturally I don’t expect that to happen in reality!

December was obviously another very good month for my Nutmeg investments. Excluding my new thematic portfolio, their total net value rose by £1,160 or 4.71% month on month. That represents an increase of £2,872 (12.53%) since 1st January 2023. If you add in the increase in value of my thematic portfolio as well (£23), that gives a total increase of £2,895 since the start of the year.

This is obviously a much more positive outcome than appeared likely just a few months ago. It clearly demonstrates the importance of taking a long-time view where investing is concerned and not panicking when the inevitable downturns occur.

As regards thematic portfolios, I discuss these in more detail in my full Nutmeg review. Personally I opted for Resource Transformation. Nutmeg’s description of this portfolio is copied below: