My Coronavirus Crisis Experience: September Update

Regular readers will know that I have been posting about my personal experience of the coronavirus crisis since lockdown started (you can read my August update here if you like).

As previously I will discuss what has been happening with my finances and my life generally over the last few weeks. I will try to avoid being too repetitive, as I have obviously published a few of these updates now and not everything changes that much from one update to the next!

As always, I will start with the money side of things.

Financial

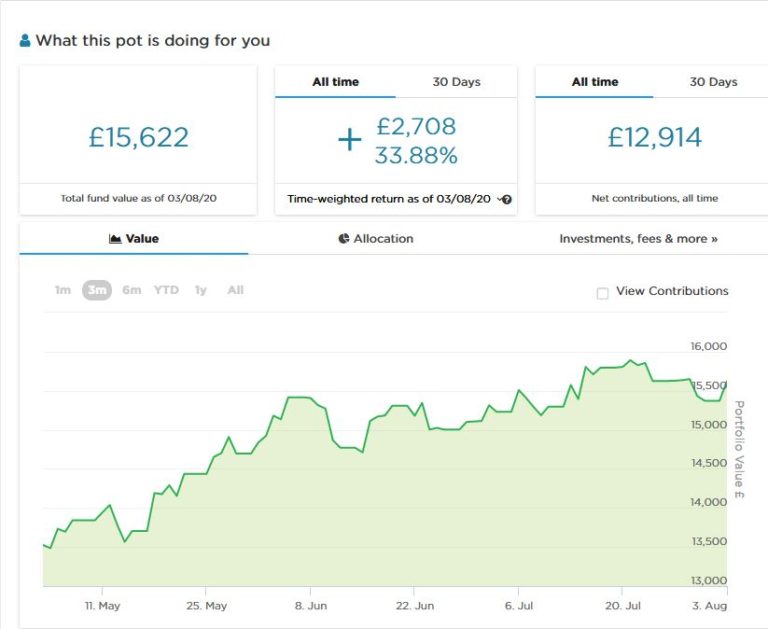

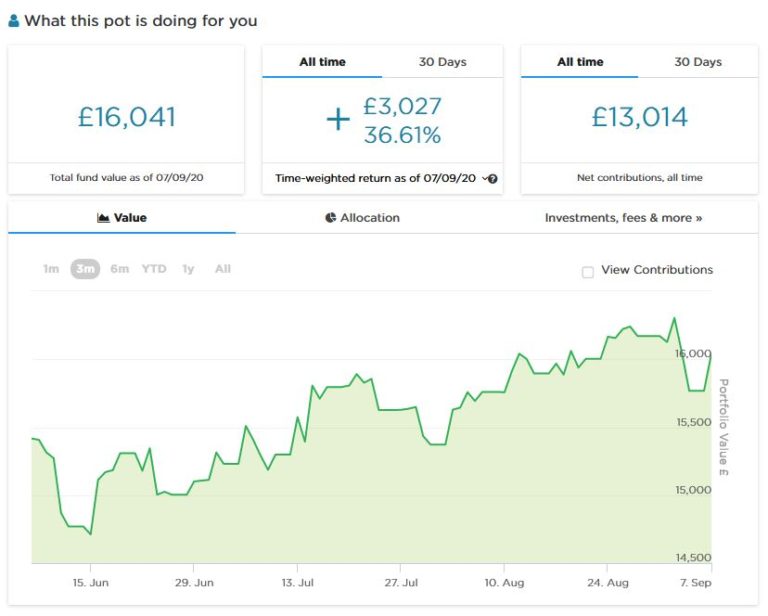

As usual, I’ll start with my Nutmeg stocks and shares ISA. This has gone up and down over the last few weeks, but is currently at £16,041. At one point it was as high as £16,270, but it’s still over £400 up on last month, so I’m not complaining. Here is a screen capture covering the last three months…

You can read my in-depth Nutmeg review here if you like.

My two Buy2LetCars investments are still delivering the promised monthly returns without any hassle. I was pleased that Buy2LetCars also chose to feature me and my blog posts about the company in their email newsletter last month. That brought me a few more readers, so a special welcome if you are one of them! Again, if you’d like to learn more, you can read my review of Buy2LetCars here and my more recent article about the company here.

There is nothing particular to report about my Property Partner or Kuflink investments, both of which are ticking along satisfactorily. As regards The House Crowd, another of their properties in which I hold a share has just been sold, so that is around £2,000 in capital I am expecting back in the next month or two. Unfortunately I am not expecting to make any profit on these two investments, though I have of course received rental payouts – or dividends if you prefer – from these properties over the time I’ve held shares in them.

As regards Crowdlords – which I discussed last month – I wrote asking about two investments I still have with them, Kennington Road eco-houses and Trent House. I had received no information from Crowdlords about either of these projects since before lockdown in March, which I found disappointing.

I received a prompt and courteous reply from Crowdlords co-founder, Richard Bush. He told me that the properties in question were proving difficult to exit from and the situation had been complicated by the change in their FCA status. He added: ‘Prior to the FCA announcement we were about to launch new investments for both of these properties, giving those that wish to leave an exit option and others who like income-based investments to take over, alongside mortgages. This is still our plan, though at the same time we will also try and sell both properties…Once we’re back up and running with Equity and Mezzanine investments we will turn our attention to the BTL’s (including Kennington Road) and still hope to have an exit option available by the end of the year. In the meantime Trent House will continue to earn 6% p.a interest.’

So I guess that is somewhat reassuring, but I’m still not holding my breath about seeing any return from either of these projects any time soon. It’s a shame because I’ve always liked Crowdlords and had good returns from my other investments with them. But obviously these are unprecedented times and property markets generally have been struggling. I will wait to see what new offering the company comes up with, but it will have to be very enticing indeed to persuade me to invest with them again.

As mentioned last time, I applied for the second (and final) round of SEISS (Self Employed Income Support Scheme) payments in mid-August and duly received payment a few days latter. I haven’t seen any complaints or problems about the administration of the SEISS programme and think HMRC deserve a lot of credit for how smoothly it has run. I do know there were issues over eligibility, however, so my commiserations go to any self-employed people who – for no fault of their own – failed to qualify.

In any event, if you are self-employed and eligible for a SEISS payment, applications are open now, so don’t delay!

Personal

In the last few weeks I have done a few things for the first time since lockdown in March. For one, I took advantage of the government’s Eat Out to Help Out scheme to enjoy a couple of pub lunches (okay, one was more of a pub brunch). It was great to be doing something more normal again and catch up with old friends I hadn’t seen since the start of the year. And paying half-price was a nice bonus!

It was obviously a different experience from the usual. When my friend and I arrived for our pub lunch, we were met by a man at the door who checked our booking and showed us to our table (no chance to pick our own as we would normally). One thing I noticed was that no staff were wearing masks and only a few customers. As a mask sceptic this didn’t bother me, but again I was struck by the incongruity of a situation where you can be in a pub surrounded by other diners for a couple of hours with almost nobody masked, then go to a supermarket and be forced to put one on while there (unless you’re exempt, of course).

In any event, I really enjoyed my pub lunch and catching up with my friend. We couldn’t pay cash as we would normally – nobody wants cash nowadays in case it’s contaminated – so my friend paid on his card and I later forwarded my half to him via PayPal. That was a first!

I also went to Birmingham to meet another old friend for brunch at one of the Wetherspoons pubs there. It felt odd to be on the streets in Brum and see so many people wearing masks in the open. Nobody does this in the small town where I live, but I guess it’s a bit different in big cities. Anyway, my friend arrived before me and was directed to a table at the back of the pub. I then had to wander around the tables looking for him behind various protective screens, feeling like a voyeur or a spy. But thankfully I found him eventually!

The instructions on the table told us to order via the Wetherspoons app. That task fell to me, as my friend doesn’t have a smartphone. I managed to do it after signing in to the pub’s free WiFi. I saw several people struggling with this, though. They either ended up hailing a passing waitress or gave up and ordered at the bar.

Anyway, the app worked well for me, and I was impressed by the speed with which cutlery was brought to our table, shortly followed by our meals (two all-day breakfasts). We both also ordered coffee with limitless refills. I was pleased to discover that this was still on offer, though you are now supposed to ask a staff member for a new mug before going to the coffee machine again. I did this, but I don’t think anyone else did.

I have just returned form a short break in Minehead on the Somerset coast (my cover image shows the harbour with the Butlins camp in the background!). I won’t say too much about this here as I plan to do a separate post about it soon. But I will say it was an enjoyable and relaxing break, only slightly marred by the fact that many of the attractions were closed due to Covid. I did manage to visit the nearby Dunster Castle (pictured below), which is owned by the National Trust. Sadly only some areas were open to the public, with various restrictions due to the virus. But on the plus side, because visitor numbers were being limited, I had plenty of space to appreciate what was actually on view!

Going back to masks and such matters, I have been wearing a full face shield in supermarkets (I’m not going to other shops till masks are voluntary again, though I might make an exception if the shop clearly states that they welcome non-mask-wearers). I find this a good compromise as it is much easier to breathe through than a cloth mask, and I haven’t yet been challenged by any staff members or self-appointed mask police. I also recently obtained a half-face shield which covers you from the nose downward. That makes it more portable, and also means your vision isn’t impaired (shields are made of clear plastic, but with my eyesight I struggle a bit reading lists of ingredients through them). In case you are interested, here’s an Amazon ad (affiliate) for some half-face shields similar to the type I bought.

And that’s it really. Recent reports are indicating an uptick in the virus among young people especially, and of course the doom-mongers are out in force again. Nonetheless, I think there are still plenty of reasons to stay positive. Hospital admissions and deaths are thankfully still at very low levels. And in my personal opinion we are very unlikely to see a ‘second wave’ anywhere near as bad as the first. Of course, it’s important to continue taking sensible precautions such as hand-washing and using sanitizing gel, along with social distancing (if you can keep up with the ever-changing rules). Personally I think that any marginal benefits from wearing masks are more than offset by the way people misuse them in practice. But I’d better not go on any more about that!

I hope you and your loved ones are staying safe and sane during this crazy time. As ever, if you have any comments or questions about this post, please do leave them below.